jetcityimage

introduction

Building a business is hard. Building a publicly traded company with consistent earnings growth and double-digit annual returns is much more difficult. Doing this in a cyclical industry takes things to a whole new level.

Basically, there are three main ones The machinery companies on my radar have done this:

- Deere & Company (DE).

- Caterpillar (cat).

- cumin (New York Stock Exchange: CMI)the star of this article.

Since January 2004, CMI stock has returned 17.6% annually!

This includes the Great Financial Crisis, the 2015/16 industrial recession, and the pandemic.

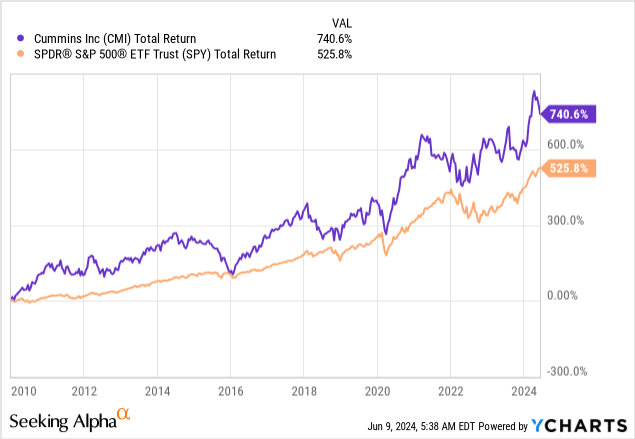

Since January 2010, CMI has generated a total return of 741%, beating the astonishing 526% return of the S&P 500 by a significant margin!

Interestingly, CMI was also one of the first industrial stocks to begin covering on Seeking Alpha.

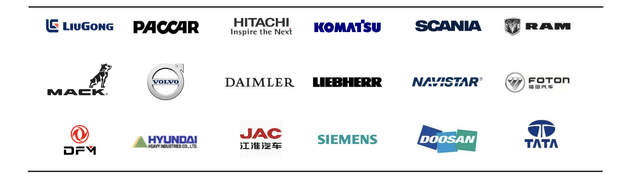

Several years ago, I was really fascinated by this diversified business model, which We have enjoyed great relationships with some of the world’s largest truck/machinery producers.

As we live in a highly complex, globalized world where power/influence increasingly shifts to suppliers, Cummins has put itself in a great position to benefit from secular and cyclical growth.

My last article about this company was written on February 8, when I went with the title “The Power Play: Cummins’ Path to More Than 10% Annual Revenue.”

Since then, shares have risen 11%, outperforming the S&P 500 by about 400 basis points.

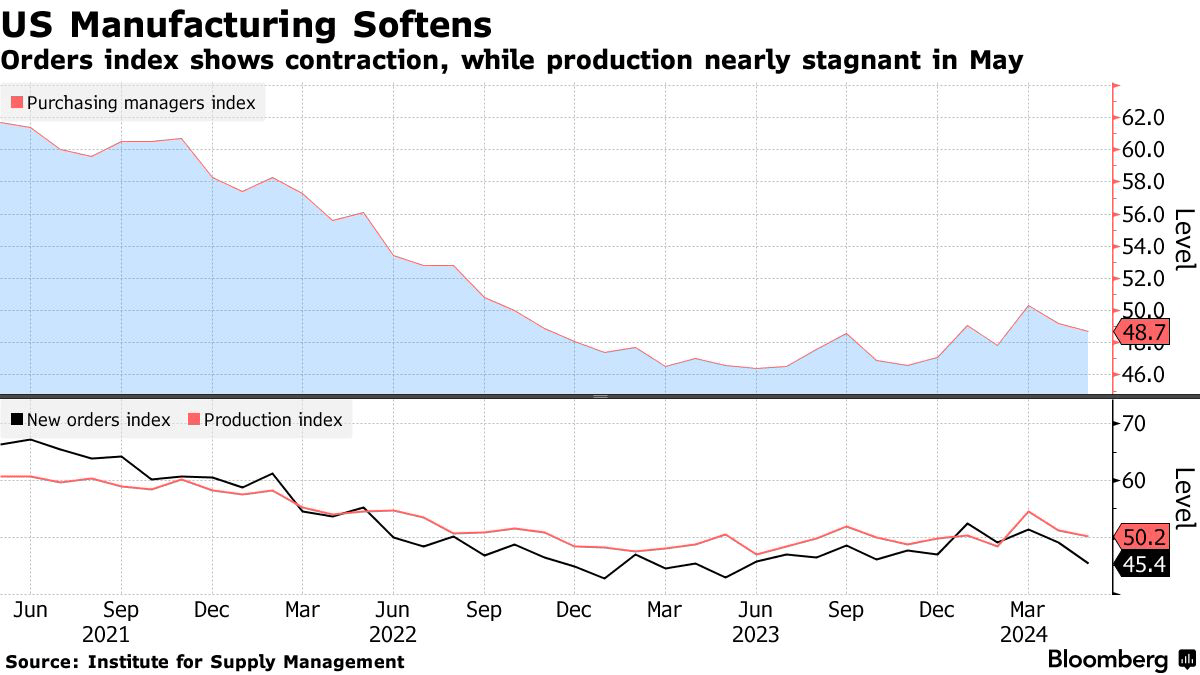

This is an impressive performance, as cyclical indicators indicate the failure of demand for manufacturing industries in the United States to recover.

As Bloomberg reported on June 3, the ISM manufacturing index is back below 50 (the neutral line), with a sharp decline in new orders.

Bloomberg

This is what one respondent from the machinery industry had to say:

Backlogs are dwindling as we get overwhelmed with orders; New orders are not coming in as strongly as the backlog decreases. Inflation remains an issue in raw material pricing and interest rates. We expect a steady hold in calendar year 2024, especially since it is a presidential election year. – Via Bloomberg

In this article, I will update my bullish case using the company’s latest earnings, investor day, and other relevant developments impacting demand for heavy machinery.

So lets get to it!

Between periodic headwinds and long-term tailwinds

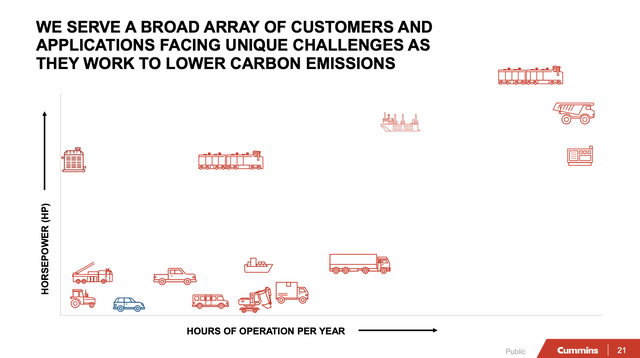

As I wrote in my previous article, Cummins is a highly diversified producer of engines and related products, serving a wide range of customers, including road transportation, mining, agriculture and construction.

Cummins Company

This includes some of the world’s largest producers, covering every continent.

Cummins Company

As the Bloomberg chart showed earlier in this article, manufacturing sentiment has been struggling since 2022. Since then, it has been below the neutral 50 line, almost without interruption.

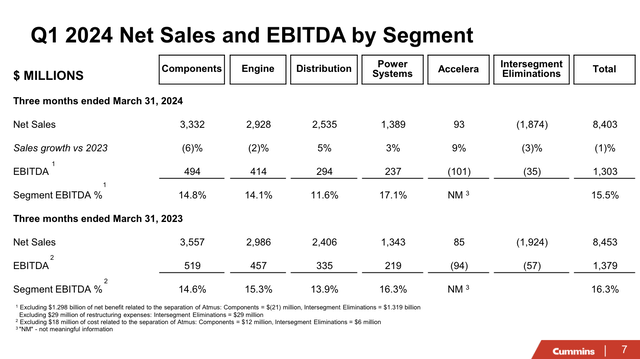

And in the first quarter of this year, we saw some of that in the company’s earnings, although the company continues to perform well.

Although heavy-duty truck production declined 5%, Cummins unit sales remained strong, with significant gains in the medium-duty truck market, where sales increased 22%.

Furthermore, the company’s power generation revenue in North America increased 21%, driven by strong demand from data centers and mission-critical applications.

Furthermore, international revenues benefited from strong sales of construction and power generation equipment.

Cummins Company

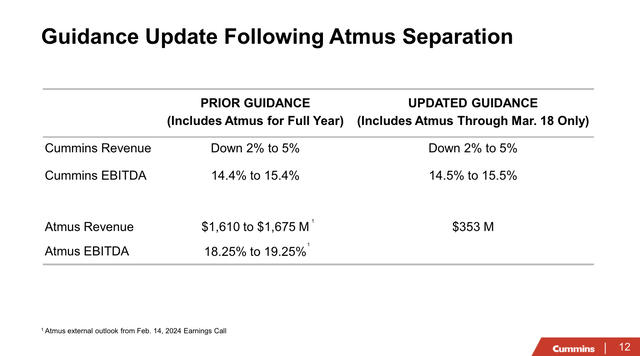

Looking ahead to the remainder of this year, the company has given a good forecast, expecting revenue to decline by 2% to 5%. In light of the economic challenges, this is a good forecast.

Additionally, the company increased its guidance for heavy-duty truck sales in North America and expects continued growth in the powertrain market, with growth of at least 10%.

Cummins Company

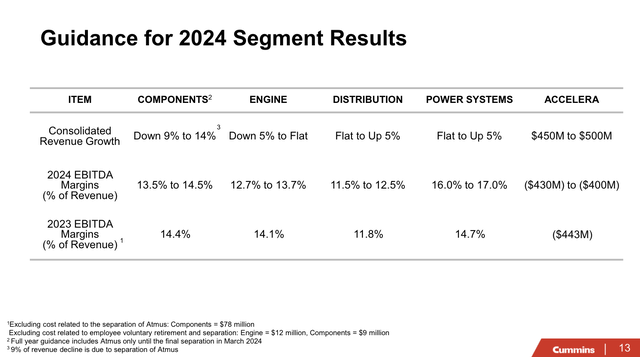

As you can see the margins are higher. The guidance rise was not significant, but given the ongoing inflationary headwinds, I am very happy to see a slight upward revision in this environment.

Overall, the combination of cyclical headwinds in motors and components and favorable secular growth supporting distribution and power systems makes sense, providing the company with needed headwinds in a very challenging environment.

Cummins Company

This brings me to the next main part of this article.

Dividends and buybacks

However, I would also like to mention the spin-off of the filtration business, Atmus Filtration Technologies (ATMU), which has been an independent public company for over a year.

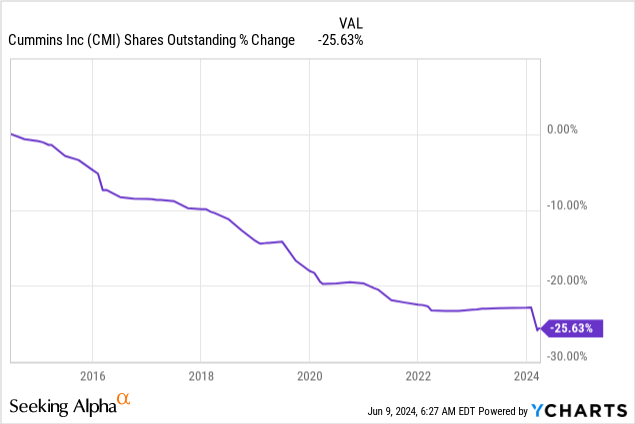

According to the company, this separation through a tax-free stock exchange reduced the number of outstanding shares of the company by 5.6 million.

This had a significant contribution to the 26% decline in outstanding shares over the past 10 years, which helped the company boost the per-share value of its business.

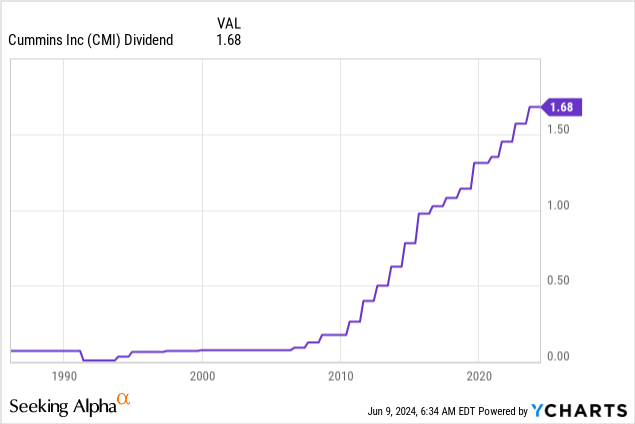

Furthermore, CMI pays a very reliable dividend.

After raising its dividend 7% on July 12, 2023, it currently pays $1.68 per share per quarter. This translates to a return of 2.5%.

These profits are protected by a low payout ratio of 35%. It has a five-year compound annual growth rate of 8.1% and a history of 18 consecutive annual dividend increases.

Although a 2.5% yield isn’t amazing, CMI has found a nice balance between dividend growth and buybacks, reporting consistently high dividend growth while maintaining a low payout ratio.

Given how volatile CMI’s business is, this is something I liked a lot.

It also helps that the company has an A-rated balance sheet with a leverage ratio of less than 1x, which means it doesn’t need to prioritize debt reduction over cash distribution.

Cummins is very optimistic about its future

So far, in this article, we have discussed the company’s good performance in light of the challenges and positive distributions to shareholders.

What we didn’t discuss is her long-term outlook.

Last month, the company held an Analyst/Investor Day, which included a number of comments I’d like to share with you.

On a long-term basis, the company is working on a “Destination Zero” strategy, which aims to balance investments in conventional engines and zero-emission technologies through its Accelera business.

Until now, Accelera has not been of much interest (with all due respect) due to its small size. In the first quarter of 2024, the segment had sales of less than $100 million, with a loss of $100 million in EBITDA.

This slow adaptation strategy makes sense, as I expect the conventional engine market to remain relevant for several more decades. Rushing into next-generation technologies can be a mistake, as some companies have discovered the hard way in recent years.

For example, car companies are increasingly focusing on hybrid cars rather than pure e-mobility.

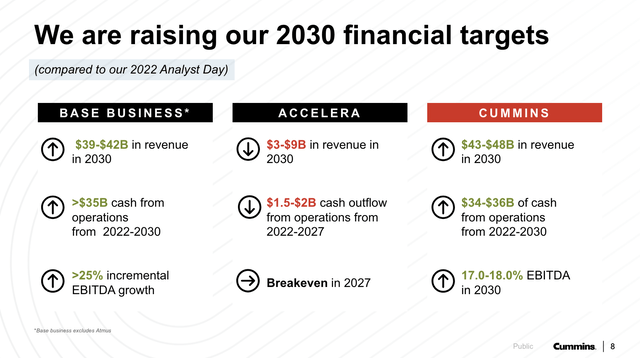

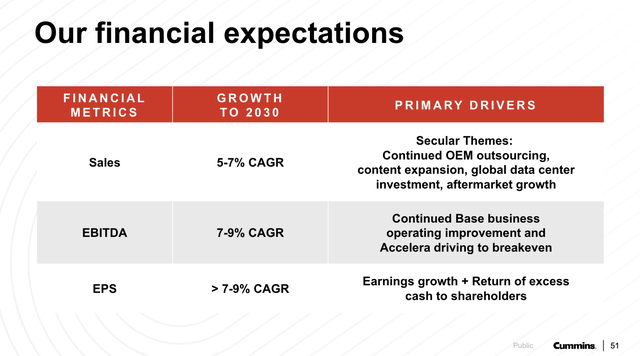

To add some color to these developments, the company expects Accelera to break even in 2027, with the potential to generate revenues of between $3 billion and $9 billion in 2030.

Cummins Company

Overall, the company is more optimistic about its business than it was two years ago. I added emphasis to the quote below.

(…) We raise our financial outlook for 2030. We are increasing our core business revenue forecast to $39 billion to $42 billionAnd that Up to $6 billion to $7 billion of what we shared two years ago. We are also increasing our forecast for cash flow from operations to $5 billion to more than $35 billion in our core businesses. And We are committed to additional EBITDA growth of 25% compared to 20%. Which we shared previously. – CMI Analyst/Investor Day 2024

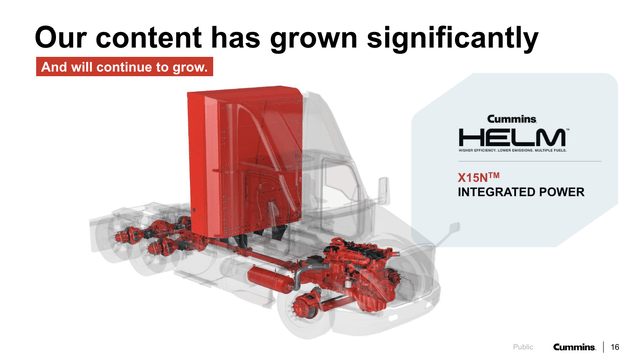

Overall, these favorable numbers are supported by diversification, including rebranded HELM (High Efficiency, Low Emissions, Multi-Fuel) engine platforms and the integration of Meritor’s powertrain solutions.

These deals strengthen its product portfolio and allow the company to offer highly efficient diesel engines capable of transitioning to alternative fuels such as natural gas and hydrogen.

Essentially, the company owns a growing portion of the truck’s critical parts, so to speak, making it an increasingly important supplier to OEMs.

Cummins Company

Speaking of OEMs, the company has joint ventures to manufacture battery cells and partnerships with companies like Daimler and Isuzu. It also works with companies like Walmart (WMT) and Chevron (CVX) to promote natural gas solutions.

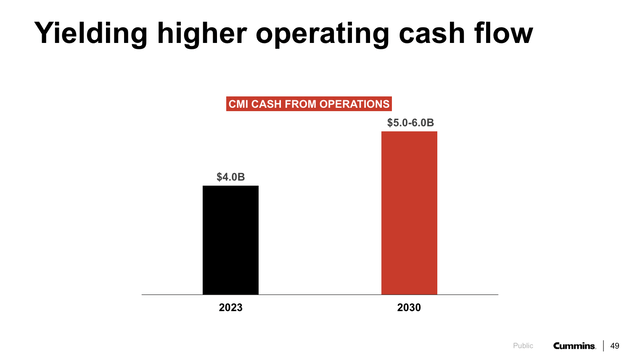

Financially, the company expects higher revenues and margins to boost operating cash flow by at least $5.0 billion in 2030.

The midpoint of its 2030 guidance implies a compound annual growth rate of 5%.

Cummins Company

Earnings per share are expected to double by at least 7% through 2030, supported by buybacks and all the growth drivers mentioned above.

When we add a dividend yield of 2.5%, we get an annual return forecast of around 10-12% (EPS growth + earnings), excluding any changes in valuation.

Cummins Company

Please note that the company’s sales guidance is primarily based on organic growth.

evaluation

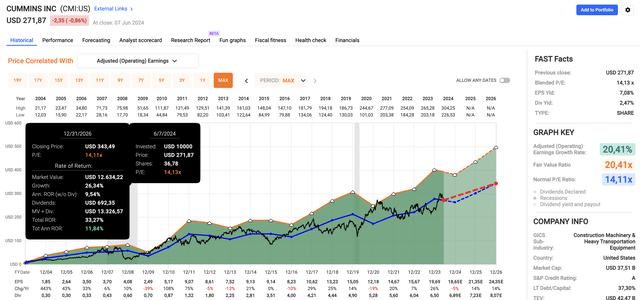

Using the FactSet data in the chart below, we see that the CMI is expected to record a 5% contraction in earnings per share this year. Given the difficult economic environment, this makes sense.

However, in 2024 and 2025, the company is expected to see 14% growth in earnings per share.

Quick charts

This bodes well for its valuation, as the stock trades at a P/E ratio of 14.1x, in line with its 20-year average.

This implies a fair share price of $340, 25% above its current price.

It also suggests an annualized return of 10-12%, which is in line with long-term expectations based on the company’s earnings guidance and well-protected dividends.

If I didn’t have a lot of industrial exposure already, including DE and CAT, I would look to buy CMI, because it provides well-diversified industrial exposure to clients in all the major engine-driven sectors – with increased exposure to growth markets like data centres.

However, given the economic uncertainty, I would not jump a full position at these levels.

I think gradual investing is the best solution.

If economic growth in cyclical regions continues to decline, investors will likely decline in the coming months. If the stock takes off, investors have a foot in the door.

Away

Cummins is a strong player in the machinery sector, consistently generating impressive returns despite regular economic fluctuations.

I believe the company’s diversified business model and strong relationships with major producers position it well for cyclical and secular growth.

Even with a challenging market outlook, Cummins’ focus on innovation, such as its “Destination Zero” strategy, and strong financial health support its resilience.

Through reliable dividends and strategic buybacks, Cummins continues to demonstrate its commitment to shareholders, making it a compelling long-term investment for investors seeking industrial exposure.

Pros and Cons

Positives:

- Powerful performance: Cummins has achieved impressive returns, with 17.6% annual growth since 2004.

- Diversified business model: The company’s diverse portfolio, covering everything from heavy trucks to power generation, provides flexibility and long-term growth in emerging industries.

- Solid finances: With a reliable dividend, strategic buybacks, and an A-rated balance sheet, CMI is likely to remain a great place for dividend growth for many years to come.

- Future growth: The “Destination Zero” strategy and partnerships for next-generation technologies enable Cummins to achieve sustainable growth, as it adapts to a more sustainable industry.

cons:

- Cyclical industry: The machinery sector’s dependence on economic cycles can lead to fluctuations.

- Economic uncertainty: Current manufacturing sentiment and economic headwinds indicate potential challenges ahead.