nicoletaionescu

Co-authored by Treading Softly

The last time I explicitly stated that I was using a particular fund to bet on the success of the American economy and the success of the American people, I wrote:

“You have to have income To survive one should not rely on doomsday predictions. Time and time again, they cannot accurately predict what default rates will persist in the markets they are supposed to oversee. This reminds me that the US economy often performs beyond what others expect of it. Too often, people have doubted the United States’ ability to continue to deliver strong economic returns, or weather the coming storms, and the nation continues to prove skeptics wrong. “I have learned that it is more profitable to bet with the United States than against it.”

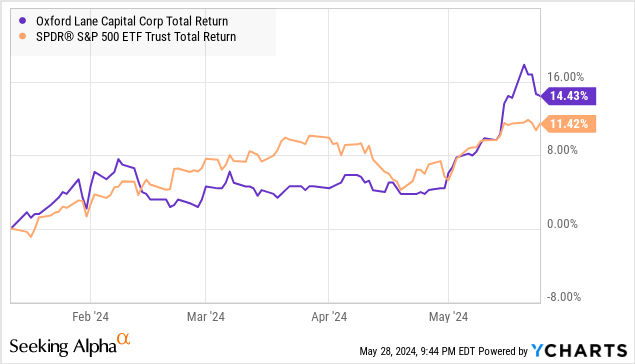

Those Those who disagreed with me did not disagree about betting on the American economy, but rather they disagreed about certain aspects of the work of the fund itself. They felt that management was overpaid, that the fund’s expenses were too high, and they constantly worried about its ability to provide strong overall returns. I am happy to point out to any of those who have expressed those concerns or comments that I appreciate them pointing out what they thought were valid concerns. I’m also happy to note that since we last wrote about this great fund and our bet on the US economy, it has outperformed even the most beloved index – the S&P 500 (spy).

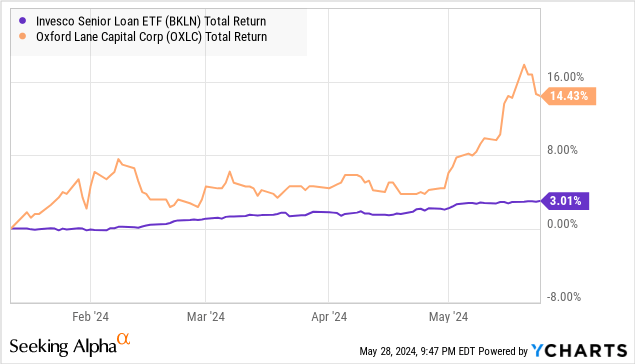

However, I will say that constantly comparing a fund that invests in leveraged debt to the S&P 500 is not a good comparison over the long term. It should be compared to a fund that invests in similar debt without additional leverage. For this reason, I prefer to use the Invesco Senior Loan ETF (BKLN). It allows you to compare your performance with a similar CLO (Collateralized Loan Obligation) investment against a similar investment. Oxford Lane Capital Corp (NASDAQ:OXLC), which invests in the same financial instruments with leverage.

If you invested in the same direct loans, you would have achieved a positive total return of approximately 3% over the same time frame. OXLC was able to provide a total return of over 14%, largely due to the effect of compound leverage. CLO securities use leverage, and OXLC applies leverage at the fund level. Leverage magnifies returns in both directions. This is unpleasant if the asset class goes down, but great when it goes up.

Let’s examine OXLC’s latest results more closely and see if it can maintain its strong income and returns!

Get paid to keep betting on yourself and others

We love it when earnings reports start increasing earnings, and that’s what happened OXLC. It increased its distribution by 12.5% to $0.09 per month, as of the July distribution. What makes this increase even more notable is that OXLC already had a nosebleed yield of 18% before the increase. OXLC’s primary asset class is “equity” tranches of collateralized loan obligations. Collateralized loan obligations (CLOs) are instruments that purchase bank loans, usually from companies with credit ratings of B/B+, and then securitize them, paying out returns in a “waterfall” fashion with the lowest-yielding senior tranches repaid first, followed by subordinated debt tranches and finally, the equity tranche bearing the first loss risk. , while also getting the biggest bonus.

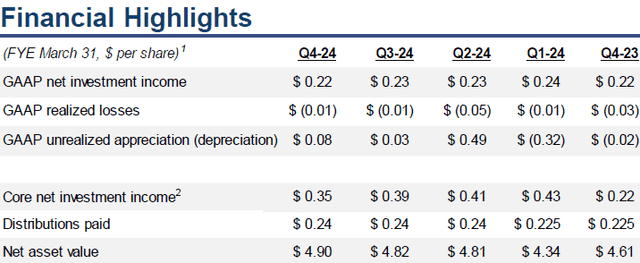

This increase is well supported by underlying net investment income, and OXLC’s NAV was up 6% year over year. source.

OXLC March Offer

However, with returns now reaching a staggering 22% of net asset value, it’s natural to question whether this push is sustainable over the long term. The answer is, it depends.” As OXLC investors, it is important for us to understand the moving parts that determine OXLC’s total return.

Notably, the new dividend is $0.27 for the quarter. This is less than “core net investment income,” but greater than “GAAP net investment income.” The primary difference between these numbers is that GAAP NII attempts to amortize credit losses.

Cash flows from a CLO stock position are lumpy, and OXLC does not receive the same amount of cash each month. Each month depends on the primary borrowers actually paying their bills. Interest payments will continue to accrue until the day the borrower defaults and stops paying. As a result, the OXLC could be sitting there collecting interest the whole time, and one month later, the borrower stops paying, and the OXLC potentially realizes a capital loss.

GAAP accounting attempts to balance the reporting of cash flows, even though the cash flows themselves are lumpy. This is done by using the “effective yield,” which is the yield you can expect to receive based on historical default and recovery rates.

Over the past year, the amount OXLC received in cash dividends was significantly higher than expected in GAAP net income. From the OXLC Annual Report (emphasis added):

“We note that there may be significant differences between Oxford Lane’s earnings prepared in accordance with generally accepted accounting principles (“GAAP”) in the United States and our taxable earnings, particularly with respect to collateralized loan obligation (“CLO”) share investments where our taxable earnings are based on the distributable share of earnings as determined under tax regulations for each investment in CLO shares, while GAAP earnings are based on the calculation of the actual return. Additionally, since our taxable earnings are generally not known until after distributions are made, they may represent These distributions are a return of capital on a tax basis. While GAAP income from our investments in CLO shares for the year ended March 31, 2024 was approximately $285.4 million, we received or are entitled to receive approximately $444.1 million in distributions from our investments in CLO shares.“.

Cash dividends were 55% higher than reported in GAAP net income. From an accounting standpoint, overpayments are reported as a “return of capital” and reduce the OXLC cost basis. For tax purposes, the calculation is completely different and is based on the distributable share of profits for each CLO. As a result, there is often a material difference between taxable income and GAAP net investment income.

As a RIC (regulated investment company), OXLC is required to distribute the majority of its taxable income, and failure to do so results in an excise tax. Last year, OXLC’s 18% return wasn’t enough to distribute all of its estimated taxable income. As a result, it had to pay a 4% excise tax of $5.4 million, meaning that Oxlic underpaid for its distribution by $135 million (about $0.564 per share). However, it should be noted that taxable income is an estimate that is subject to review upon expiration of the CLO. The actual taxable nature of CLO distributions is not fully known until the CLO distributes all of its assets. OXLC’s current estimates of taxable income may be revised higher or lower in the future. So don’t put the $0.564 figure in the bank. However, if circumstances remain benign, the $0.564 represents taxable income that will eventually be distributed either through distribution increases, supplements, or specials. Peer Eagle Point Credit Co, Inc. was (ECC) is in a very similar situation and has been paying regular supplements to reduce the amount of undistributed taxable income it has.

This accumulation of undistributed taxable income is likely the primary driver behind OXLC’s decision to increase its distribution.

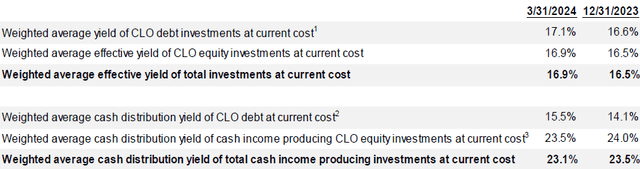

Going forward, how much can we expect from OXLC? The actual yield, which includes the expected impact of a default, rose to 16.9%. The cash dividend, which is the actual cash received divided by the current cost, is 23.1%.

OXLC March Offer

OXLC’s current distribution falls in the middle, which, we think, is a very sweet spot. It is unrealistic to believe that every borrower will pay as agreed. Borrowers defaulting is simply the fact that they are in the lending business. On the other hand, default rates have been trending well below average, corporate credit is on reasonably stable ground, and corporate leverage is not excessively high, as we have seen before in periods such as the global financial crisis. One of the reasons I’m so bullish on CLO stocks is that COVID-19 has created an opportunity for many companies to reduce their debt and improve their balance sheets. As a result, below-average defaults are likely to persist this cycle.

An OXLC may want to retain capital to rebuild book value, but tax rules require it to distribute most of its taxable income. As a result, we get an increase in distribution because OXLC has a “problem” making too much money. The new distribution exceeds earnings estimates generated by GAAP, meaning that to be sustainable, default rates must remain below average. We believe it is likely to happen; However, investors should be aware that the distribution size has exceeded this limit. On the other hand, the actual cash coming in now still greatly exceeds the distribution. This has allowed OXLC to obtain more investment and grow its future profits.

Conclusion

The nice thing about investing in debt is that you have one of two outcomes – you either get a positive return on the money you invested, or you suffer a loss. This means that default rates remain crucial to the long-term outlook of what you can expect to get from a fund like OXLC. We have observed that OXLC has been able to rebuild book value through capital preservation while continuing to pay you and me a strong income. I like it when a company or fund has a problem with making too much money. Because of their structure, they are forced to pay me more. I find this to be a win-win.

When it comes to retirement, you can never have too much income. If you have more income than you need to pay your bills and enjoy your chosen lifestyle, you can then reinvest that and easily continue to grow your income month after month. I like to think of OXLC as what I call an “income catalyst.” In chemistry, a catalyst is a substance that helps speed up or even causes a chemical reaction to occur. It is not always required in large quantities. You can add a little position in OXLC to your retirement portfolio and see a huge explosion in the amount of income.

That’s the beauty of my income method. That’s the beauty of income investing.