Kortnik

In the current economic landscape of inflation, high interest rates, and contraction in traditional bank lending, we believe private credit represents potential investment opportunities. This article outlines three main reasons why investors should consider allocating capital to private credit in large, large amounts Mixed returns.

1. Banks decline further: Regional banking crisis creates opportunities

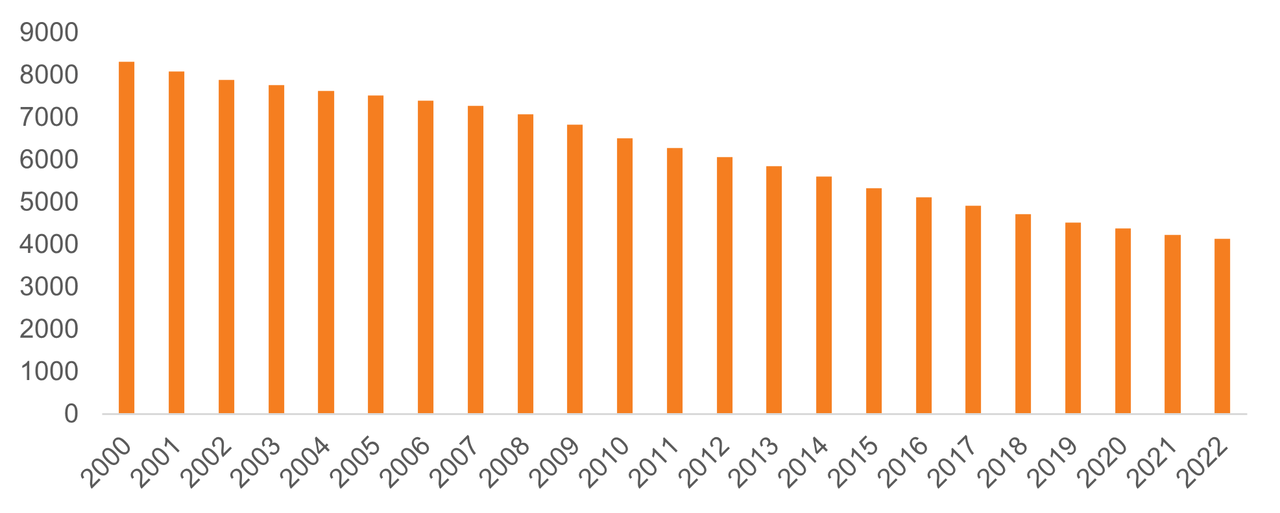

The recent regional banking crisis, epitomized by the struggles of institutions such as Silicon Valley Bank, has intensified the ongoing trend of traditional banks withdrawing from lending to small and medium-sized businesses. This is partly due to the continuing decline in the number of commercial banks operating in the United States, as shown in Figure A below. This has opened significant opportunities in asset-based lending to private credit investors.

Figure A: Number of FDIC-insured commercial banks in the United States

Source: Federal Deposit Insurance Corporation. Data accessed March 27 2024. For illustrative purposes.

Asset-based lending is a financing model where the loan is secured by collateral, usually in the form of the borrower’s assets, such as accounts receivable, inventory, equipment, or real estate. Consequently, high-quality SMEs that cannot obtain financing from local banks are turning to alternative sources of capital, creating a strong supply of potential investments in asset-based lending. In contrast to corporate lending, asset-based lending tends to be more recession-resistant, providing a cushion against economic downturn.

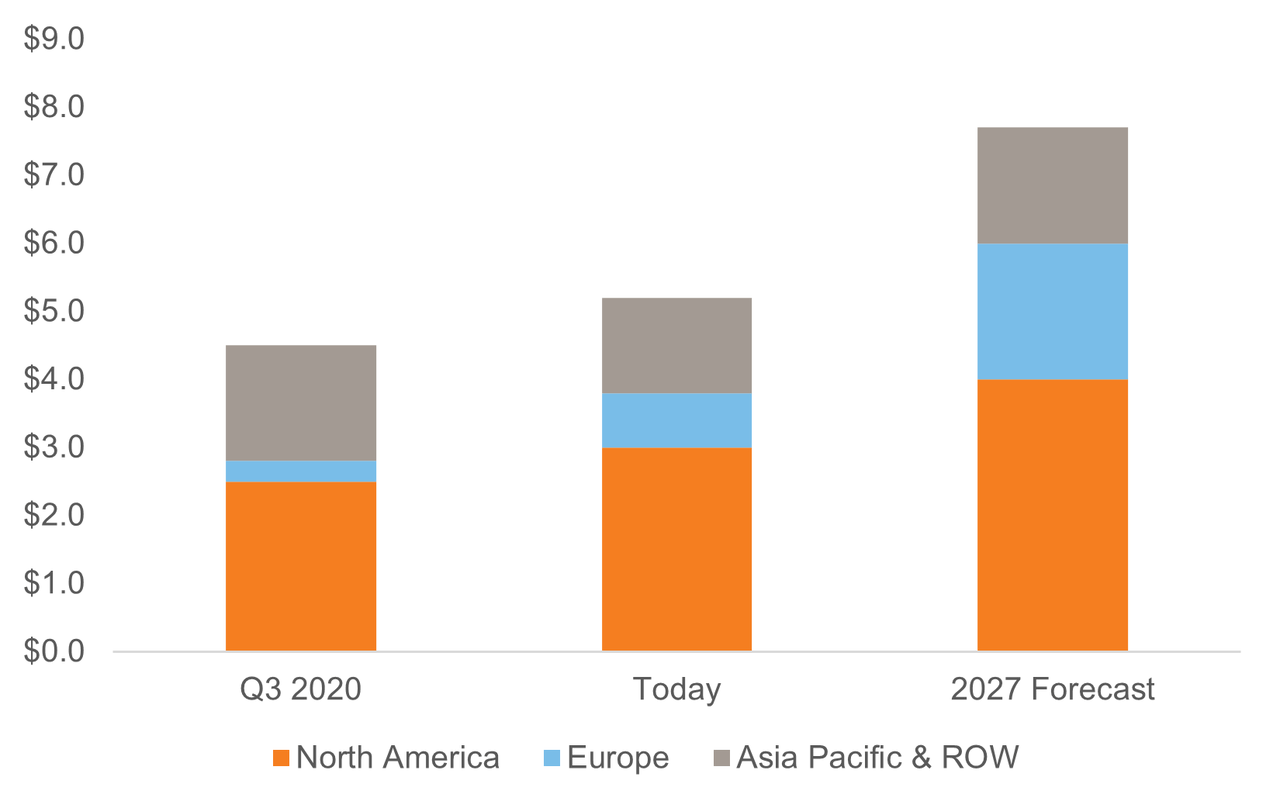

Figure B: Growth Expectations for Private Asset-Based Financing ($1 Trillion)

Source: Integer Advisors and KKR Credit. Data as of January 2024. For illustrative purposes.

Private credit investors can take advantage of this offer of opportunities and exercise selectivity to build flexible investment portfolios. Figure B highlights the significant growth trajectory expected in asset-based finance over the coming years, and depicts a landscape full of opportunities for expansion and innovation within the financial sector.

2. Upper middle market lending: Dealing with competition and pricing power

In upper middle market lending, private credit faces intense competition, especially with collateralized loan obligations (CLOs) returning as major deal contenders. The influx of capital into the market can sometimes lead to a temporary rise in competition, making it necessary for investors to adapt strategically. However, competition tends to be fleeting and varies depending on market conditions.

This dynamic creates tactical opportunities for investors to take advantage of limited periods of competition by partnering with the best general partners (GPs). Many of these large GPs have a track record of success and flexibility between direct creation up and down the volume range, while also focusing on secondary market buyouts in certain markets. By doing so, investors can deploy capital into the upper middle market when the landscape is right, while also diversifying their investments through direct creation of core middle market equity in other markets.

However, navigating this competitive landscape requires careful consideration. Investors must maintain pricing power and secure favorable terms to ensure the viability and profitability of their investments. This entails comprehensive due diligence, strategic partnerships and a deep understanding of market trends and dynamics. By utilizing these tactics, investors can improve their investment strategies and take advantage of opportunities in the private credit market.

3. European Opportunities: Favorable conditions for high-level secured lending

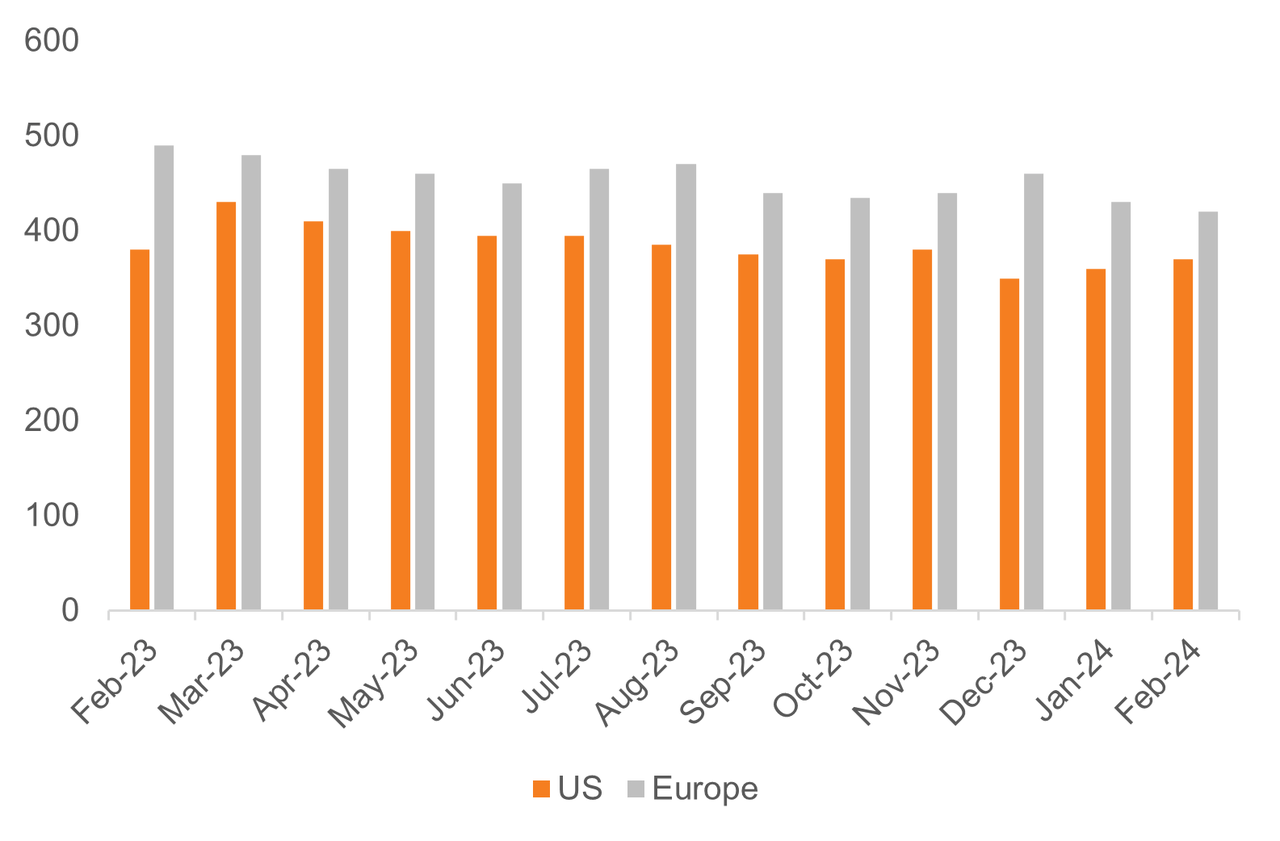

In Europe, simple secured lending presents itself as an increasingly attractive option for private credit investors. Unlike the US market, where spreads tend to be narrower due to a more mature financial landscape and higher levels of liquidity, European spreads are wider (please see Figure C), offering the potential for higher yields and enhanced returns. This can be particularly beneficial for investors seeking diversification and achieving higher risk-adjusted returns in their portfolios. This disparity in spreads underscores the attractiveness of European markets for investors seeking to benefit from favorable lending conditions. Moreover, the recent withdrawal from the market of a prominent European private credit manager has created at least a temporary gap in financing for potential borrowers.

Exhibit C: Spreads (basis points) on US versus European loans

Source: Pitchbook/LCD as of February 2024. For illustrative purposes.

In addition, European direct lending offers a significant tax advantage to non-US investors, as they are not subject to the same tax and structural restrictions as their US counterparts. This tax advantage enhances the attractiveness of European senior secured lending as a viable option for diversifying private credit portfolios and taking advantage of opportunities in global markets.

In our view, the combination of wider spreads resulting from market volatility, occasional temporary gaps in funding due to volatile economic conditions, and favorable tax conditions, make European senior secured lending a very attractive proposition for private credit investors seeking to diversify their portfolios and capitalize on available opportunities. To maximize returns in today’s dynamic and evolving market environment.

Bottom line

Despite continued uncertainty over inflation and interest rates and limited bank loans available, we believe that private credit still provides compelling investment opportunities, especially for investors seeking diversification and achieving stable returns in volatile markets.

By capitalizing on the decline of traditional banks, addressing competition in the upper middle market, and exploring attractive opportunities in European markets, investors can leverage the unique advantages of private credit in today’s environment to achieve their investment goals.

Furthermore, as the regulatory landscape evolves and alternative lending platforms emerge, we contend that now is the time to leverage the potential of private credit and position portfolios for long-term success in today’s evolving economic landscape.

Disclosures

These offers are subject to change at any time based on market or other conditions, and are effective as of the date at the top of the page. The information, analysis and opinions contained herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents forecasts of market prices and/or volume patterns using various analytical data. It does not represent a forecast for the stock market, or any specific investment.

Nothing in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion on the suitability of any investment. The general information in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

Please remember that all investments carry a certain level of risk, including potential loss of invested capital. They do not usually grow at an equal rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to minimize risk and maximize return can, at certain times, inadvertently reduce returns.

Frank Russell is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which members of the Russell Investments family of companies are permitted to use under license from Frank Russell. Members of the Russell Investments group of companies are in no way affiliated with Frank Russell or any entity operating under the “FTSE RUSSELL” brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transmitted or distributed in any form without the prior written permission of Russell Investments. They are delivered on an “as is” basis without warranty.

Corp-12503

Original post