5 Insights from the Federal Open Market Committee’s (FOMC) upcoming interest rate decision in June

Atheate Chinaguin/iStock via Getty Images

Stock markets will begin next week pricing in disappointingly strong May job growth data on Friday. Ordinary people prefer an economy that adds jobs, while stocks want that economy to decline For the central bank to reduce interest rates.

Investors have two other economic considerations ahead. On Wednesday morning, the Bureau of Labor Statistics will announce inflation levels for May 2024. In my preview report, I expect an increase in clothing, no change in food prices, and a decline in auto goods. At 2 p.m. that afternoon, the Federal Open Market Committee (“FOMC”) will issue its statement and announce its decision on the monetary policy interest rate.

Ahead of this meeting, the CME FedWatch tool downgraded the probability of a rate cut following the Fed’s June and July meetings. Although the markets expect higher interest Interest Rates Longer What should readers expect from the FOMC next week? Moreover, in September Fedwatch indicated an increased likelihood of interest rates not changing. The odds increased from 31.3% on June 6, 2024 to 51%.

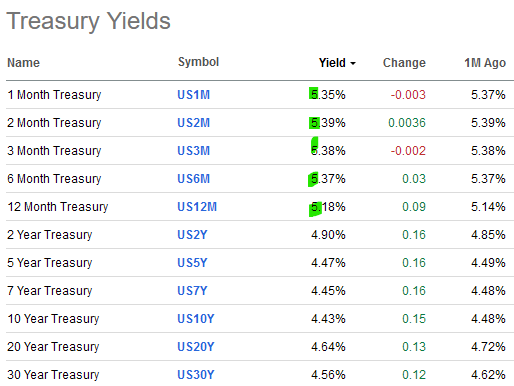

Readers should once again monitor US Treasury yields after the meeting. The returns are about the same as a month ago. They are higher than 5.0% for the short term and are generally lower for those maturing in two years (US2Y) or later.

Seeking alpha

The Federal Open Market Committee may offer investors five insights for stock markets.

1/ Insights into job growth in May 2024

In May, nonfarm payrolls rose by 272,000. Markets expected the economy to add 182,000. Health care added 68,000 jobs in May. The government resumed employment, adding 43,000. Employment in entertainment and hospitality added 42,000 people in the month, while food services and drinking establishments employed 25,000 people.

Among the areas of job growth, readers should exclude government jobs data. It is partly linked to fiscal policy, which also increases pressure on inflation. Governments use these funds to employ public service workers. It in turn enhances the employment report. The Federal Open Market Committee may introduce these functions to evaluate the effectiveness of its monetary policy. Most importantly, the bank wants the economy to add jobs to the supply side of production. Since inflation is demand-driven and supply-constrained, inflation is mitigated because jobs added to production would increase supply.

As for stock ideas, in light of the rise in government jobs, investors should continue investing in the defense industry. For example, RTX (RTX) closed at an all-time high.

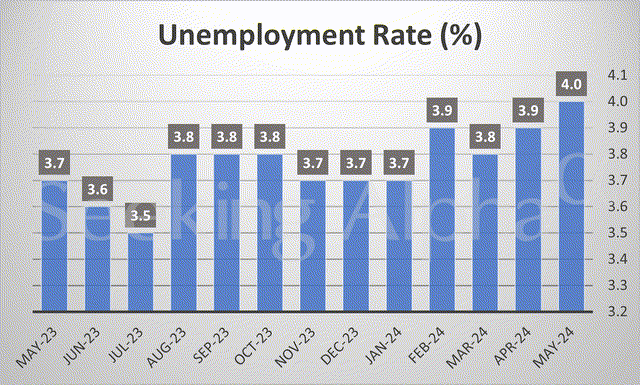

The Federal Open Market Committee may comment on the uncertainty surrounding the unemployment rate rising to 4.0%, the highest level in two years. Conversely, the labor force participation rate fell from 62.7% in April to 62.5% in May, with the labor force participation rate at its highest level since May 2002. However, the Bureau of Labor Statistics reported that Jobs have almost doubled.

Seeking alpha

In its May 1, 2024, press release, the FOMC said job gains remained strong and the unemployment rate remained low. Since job growth strengthened last month, the committee should expect a reduced impact on employment by keeping the current Fed funds rate at 5.25% to 5.50%. He will reiterate his statement that monetary policy has a better balance between achieving employment and inflation targets.

2/Insight into the Core Personal Consumption Expenditures Price Index

The Fed will comment on the personal consumption expenditures price index, which excludes food and energy. This rose 2.8% in April and is roughly consistent with the previous three months.

|

Change from 1 month to 1 year ago |

|

|

April 2024 |

2.80% |

|

March 2024 |

2.80% |

|

February 2024 |

2.80% |

|

January 2024 |

2.90% |

Information from

The Fed prefers this index because it excludes food and energy. By excluding volatile price changes, the Fed will see inflation continue to rise above its target rate of 2.0%. The Fed will comment on services prices, which rose 3.9%, as the main contributor to the index. In comparison, commodity prices rose by 0.1%.

3/ Timing of interest rate cuts

Markets initially shrugged off Friday’s strong jobs report by rallying in the morning. By early afternoon, selling volume accelerated. The Nasdaq (QQQ) still closed the week up 2.72%. Conversely, the Russell 2000 (IWM) lost 1.17% on Friday and is down 2.22% for the week. Small businesses are more sensitive to interest rate levels. This group will not care about interest rates remaining where they are in June. Instead, he will listen to changes in the FOMC’s policy statement and Fed Chairman Powell’s choice of words in the question-and-answer session.

The Fed and stock market will also react to the CPI report next Wednesday morning. The report needs to clarify that inflation is on a steady downward path towards 2.0%.

In a less likely scenario, an exciting May CPI report would revive fears that the Fed may raise interest rates. However, the Fed Chairman is unlikely to suggest that the central bank changes its wait-and-see policy. Since last September 2023, the Fed has hinted at a pause in interest rates and several rate cuts. A sudden reversal in its policy could shake the market’s uptrend.

4/ Comment on GameStop, Meme stocks, and speculation

The media may ask Fed Chair Powell about rampant stock speculation in companies like GameStop (GME) and AMC Entertainment (AMC). We expect Powell to ignore the importance of two failures in monetary policy. Furthermore, the trading range for GME stock of $9.95 – $65.00 is a matter for the Securities and Exchange Commission. The valuations of both companies will be revised downward as their executives take advantage of the market’s folly and the rise in their shares by selling shares to retail investors.

GameStop took advantage of blind optimism in the market by selling shares twice. The company filed to sell up to 75 million shares on June 7. On May 24, it sold 45 million shares to raise $933.4 million.

Trump Media (DJT) is another example of extreme speculation. It reported revenue of $770,500 and an adjusted EBITDA loss of $12.1 million. However, the company’s market cap is $7.88 billion.

The stock market needs more than higher interest rates to tighten financial credit conditions. Even then, stocks with unusual valuations represent an isolated dynamic between speculators and short sellers. In this scenario, the companies are the “house” of the casino. The house almost always wins.

5/ Bond yields

US Treasury yields rose on Friday after a strong jobs report. It may rise again after the inflation report. The Federal Open Market Committee’s statement on Wednesday is expected to further influence bond yield rates. In a press release issued last month, the committee said it would “work to slow the decline in its securities holdings by reducing the monthly redemption ceiling for Treasury securities from $60 billion to $25 billion.” It also said it would “maintain the monthly redemption of Treasury bonds.” The agency’s debt and mortgage-backed securities are capped at $35 billion.

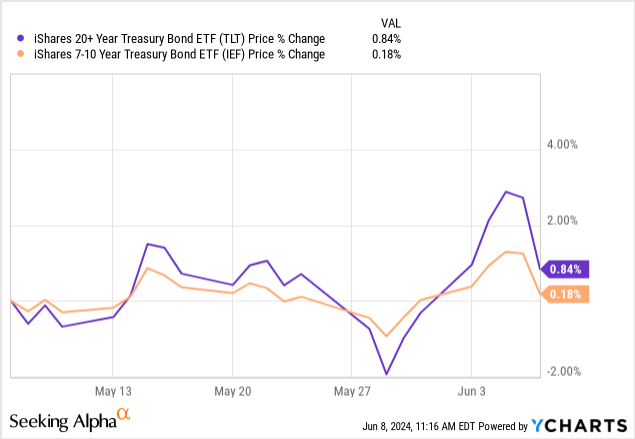

Last month, 20-year-plus Treasuries (TLT) rose 0.84%, compared to a 0.18% gain in 7-10 years (IEF).

Your takeaway

Stocks will not find their direction until after the FOMC meeting. Markets already expect interest rates to stay the same. This will hurt the Euro (FXE) and Canadian Dollar (FXC) over the next few months. This benefits the American economy, reducing the cost of imports.

We expect trading volumes for speculative stocks to continue. Long-term investors should ignore the hype. Instead, non-changing interest rates increase the attractiveness of short-term bonds (SGOV). It also builds a case for profit taking from shallow sectors, such as the Nasdaq (QQQ) and S&P 500 (SP500).