the wolf

Co-authored with Long Player.

introduction

There are more than 2.6 million miles of energy pipelines in the United States, keeping the economy supplied with biofuels for domestic use and exports. They form part of the country’s critical infrastructure Safely deliver natural gas, crude oil and petrochemical products to power plants, refineries, terminals, industrial facilities, homes and businesses.

Legendary investor Bill Gross has been pounding the tables for MLPs (Master Limited Partnerships), calling them an excellent source of significant deferred tax returns. He points out that MSPs have strong financial profiles and are significantly undervalued, mainly because regulation makes it difficult for mutual funds to invest in partnerships. Today, we will discuss Western Midstream Partners, L.P (New York Stock Exchange: Weiss), a middle-of-the-road MLP that Mr. Gross considers the best of the bunch.

WES operates 24 collection systems, 75 processing facilities and 7 Natural gas pipelines, 15 crude oil/NGL pipelines, and 16,000 miles of pipeline infrastructure. Midstream MLP provides collection, compression, treatment, processing, commodity transportation and wastewater disposal services to clients in the Delaware Basin of west Texas and New Mexico and the DJ Basin of northeastern Colorado. These are among the most active and productive basins in the United States

Note: WES is a master limited partnership that files a Schedule K-1 for tax purposes.

Let’s start with the good news

WES recently announced a 52% increase in distribution during its first quarter press release. Not only does distribution increase, but the strength of the balance sheet also increases. The current quarterly dividend of $0.875 per share calculates to an impressive annualized yield of 9.3%.

Since January 2020, WES has reduced the number of its outstanding units by more than 15%, indicating that management believes the company is undervalued. In addition, WES has continued its deleveraging efforts by repurchasing approximately $150 million of its senior notes at 96% par value since the beginning of 2024. Now, with a debt ratio of 3.3x and a target of reaching 3.0x, management intends Find out what else could happen. Must be done to raise the price of the common unit.

This traditionally undervalued sector is self-financing its growth

The midstream MLP sector as a whole is cheap and unfavorable, as bond king Bill Gross has pointed out. Therefore, there is significant potential for capital appreciation waiting for carriers to return to historical valuations. One thing to keep in mind is that although partnerships and midstream companies grew faster during boom times, this growth largely came as condominium offerings diluted. Therefore, shareholders often saw only a small portion of this growth in the form of increased dividends and higher prices.

Today, most midstream companies (or partnerships) are much stronger financially than they were during the boom. WES, in particular, was able to fund its entire capital budget and distribution payments while still having some free cash flow remaining. For the first quarter of 2024, the partnership recorded the highest quarterly net income ($559.5 million) and EBITDA ($608.4 million) in its operating history, generating $225 million in free cash flow before dividends and $1. $5 million after dividends. We expect future per-unit growth to come from a combination of organic growth as well as common unit repurchases. These records were primarily driven by increased productivity across its operating assets across production lines.

We note that processed volumes decreased slightly due to generally lower profit margin joint venture sales. However, the fireside conversation after the conference call indicated that these sales created a one-time margin increase for some actions due to the change in earnings mix.

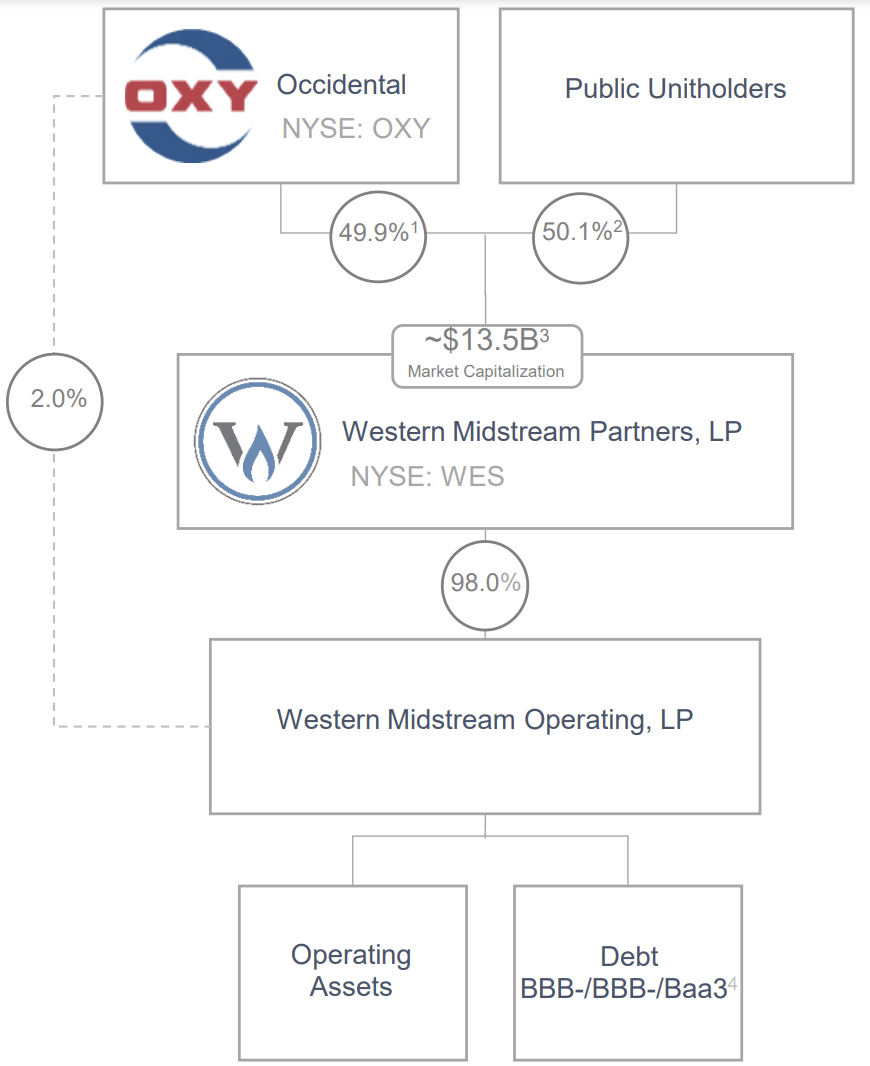

The symbiotic relationship with Buffett-backed Occidental Petroleum

The logistics sector is witnessing a lot of merger and acquisition activity, with major operators seeking to make acquisitions at premium valuations. Energy Transfer (ET) recently announced its $3.52 billion acquisition of WTG Midstream for what is estimated to be an EBITDA multiple of 7.6 to 8.5 times (based on estimated cumulative increase in EBITDA and amortization (EBITDA) to ET from the transaction). Occidental Petroleum (OXY) has an impressive history of making midstream operations extremely valuable and then selling those operations for good money.

The exploration and production giant owns nearly half of WES’s outstanding combined units, while controlling the general partner, according to its latest annual report. source.

Investor presentation in May 2024

WES is fully integrated with OXY, both from an ownership and operations perspective. In Q1 2024, 31% of natural gas throughput, 89% of crude oil and NGL throughput, and 77% of produced water throughput are attributable to production owned or controlled by OXY (Source: 10-Q).

Western Midstream has become more focused on its operations with Occidental Petroleum (OXY). The ability to coordinate capital projects with OXY will likely drive higher return on capital in the future. Warren Buffett-backed Oxy is widely viewed as financially healthy, with good debt ratings. Therefore, Western Midstream will also receive high ratings given its close ties to OXY and its low debt levels. As an essentially captive mid-cap company, financial ratings are contingent on the financial strength of the parent company. Fortunately, this maximum is very high.

Looking ahead, we see potential trimming/divestiture of the WES position by OXY and acquisition of new companies by OXY, which could provide further growth opportunities for common unitholders. As a result, Western Midstream could grow faster than OXY. One thing to pay attention to is whether midstream assets are sold or dropped to WES as a result of these transactions.

Strong client base with largely fee-based contracts

For fiscal year 2023, 95% of WES’s natural gas and 100% of its crude oil and NGL contracts were serviced under fee-based contracts, effectively protecting the partnership’s profitability against commodity price fluctuations. Contractual protections such as minimum volume commitments and cost-of-service provisions enhance the company’s low-volatility cash flows. It is worth noting that 59% of natural gas, 71% of liquid volumes, and 85% of water produced for the fiscal year 2023 enjoy such contractual protection.

The composition of the customer base in the major basins served is as follows:

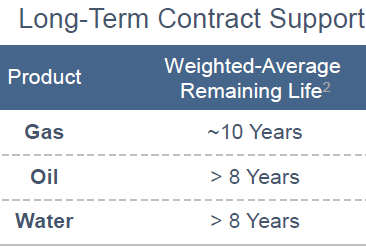

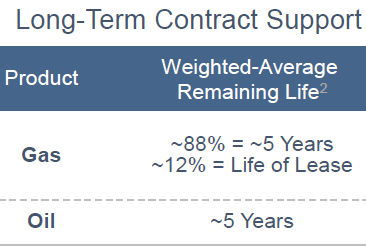

WES largely provides transportation to either long-distance communications or a consolidation service, after which a competitor transports the goods to the customer or terminal for export purposes. The partnership creates long-term contracts with creditworthy customers and has reported a weighted average remaining life of over 8 years in the Delaware Basin and over 5 years in the DJ Basin for each product. source.

Investor presentation in May 2024 Investor presentation in May 2024

When Occidental took control of this midstream company, the center of operations was DJ Basin, and it saw its assets upgraded and rationalized the most. On the other hand, the Delaware Basin is in a more favorable location for exporting natural gas that will be put into operation over the next two years. Gas produced in the Delaware Basin could be much more valuable to OXY in the future. As such, the basin is likely to be an area of focus for further midstream growth in the near term.

There is a wide range of services that moving companies can provide. Management will explore these opportunities to earn more in the future as they arise. Currently, a significant portion of WES’s income comes from relocation, while larger competitors such as Kinder Morgan (KMI) and Enterprise Products Partners (EPD) generate reasonably significant income from the services that accompany that relocation. These are ways to increase the overall profitability of the partnership.

Strong commitment to shareholder returns

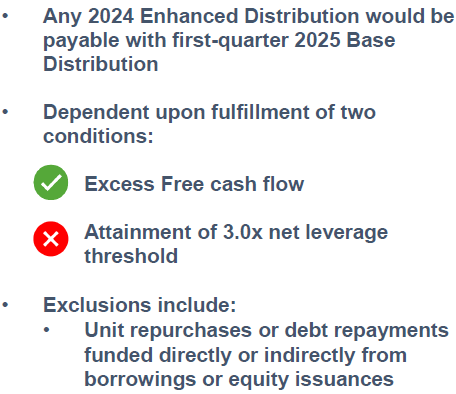

WES is a story of transformation, and it pays to continue investing to experience progress. The partnership devoted the rest of the year to current distribution and set goals for enhanced distribution in 2025.

Investor presentation in May 2024

The partnership is already in a strong position to generate free cash flow that exceeds the distribution, having provided guidance of $1.05 to $1.25 billion for the fiscal year, which exceeds the expected distribution. This target of 3x leverage is typical middle of the road with a large client. This level of debt puts it on par with EPD’s industry-leading leverage levels, creating numerous opportunities for acquisitions.

Attractive rating

The intermediate industry is known as the utility portion of the oil and gas industry because take-or-pay provisions limit the decline in profits. Additionally, this private partnership has an investment-grade debt rating with industry-leading leverage levels, increasing investment safety.

As discussed previously, this part of the industry is unfavorable but has valuable assets with highly predictable profitability. We face a future of low interest rates, even if that future is delayed, and that bodes very well for the massive distributions of deferred taxes in the multilateral corporate sector to drive a return to historical valuations.

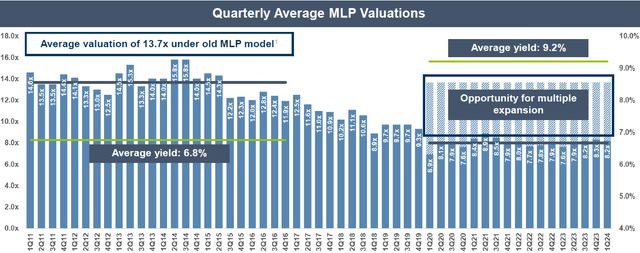

As WES notes in its first-quarter presentation, MLPs’ valuations were much higher despite their lower returns, higher debt, and pursuit of diluted capital expenditures prior to 2016. The new MLP model, which focuses on self-financing, debt reduction, unit buybacks, and restructuring Debts. All the other contributor-friendly elements certainly warrant an excellent rating. Let the industry trade at a 5.5x discount to its previous self. source.

Investor presentation in May 2024

As such, we see significant upside for WES over the next five years, and we will sit back and collect those massive tax-deferred distributions while we wait.

Conclusion

Mr. Market has yet to appreciate all the progress Western Midstream Partners, LP has made recently. The partnership maintains a strong balance sheet, generates abundant free cash flow, and provides critical services to Buffett-backed OXY.

In this article, we discuss the following benefits of investing in WES, which reinforce Bond King Bill Gross’s views on this mid-cap company.

-

Industry-leading 9.3% deferred tax return

-

Self-funds its growth through predictable free cash flows from long-term, fee-based contracts

-

Investment grade balance sheet with further debt reduction efforts

-

Excellent prospects for enhanced distribution in 2025.

With WES, we are collecting a significant deferred tax return today while we await the results of the company’s strategic initiatives and operational execution to unlock a more premium valuation. The beauty of the income method is to accumulate a healthy income while we patiently wait for the markets to recognize the true potential of our properties. This is the core of our investment strategy within our investment group.