Olga Kazakova/iStock via Getty Images

You may have heard the expression, “Make hay while the sun shines.” In essence, this means taking advantage of opportunity when conditions are right. Regarding investing in the stock market, our current situation is unique An opportunity to take advantage of the rising market before this opportunity is lost. One way for income investors like me to benefit from the strong US economy coupled with the growth in cloud AI infrastructure Consumer spending remained strong Despite High Inflation, You Should Buy YieldMax AMZN Option Income Strategy ETF (NYSEARCA: AMZI).

In my last article reviewing several YieldMax high yield ETFs, I mentioned how Magnificent 7 stocks and growing investment in AI are pushing some YieldMax ETFs forward leading to continued monthly strength Income generated by option premiums from the underlying reference asset. In this review, I want to examine how AMZY will benefit from the continued outperformance of its benchmark asset, Amazon (Amzn) stock.

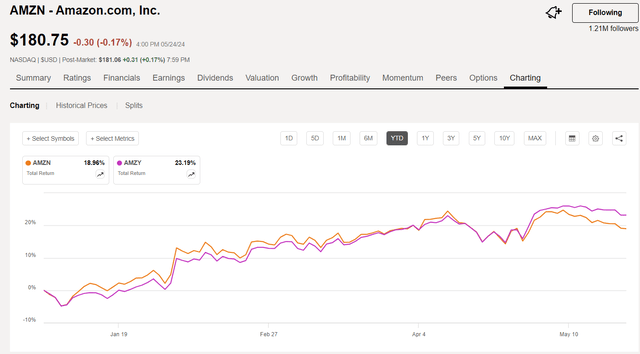

Amazon sees its stock continuing to outperform in 2024, rising more than 54% over the past year and nearly 19% since the beginning of the year. According to fellow SA analyst Beth Kindig, whose research I respect, AMZN could soon join the $2T club due to growth from AWS and announcements.

Meanwhile, Amazon is well positioned to capitalize on rapidly growing demand for AI, with a multi-billion dollar run rate on AWS of AI products already. Combined with advertising, the two drive strong margin expansion and aid in both top and bottom line growth; In turn, this growth creates an attractive valuation in the bottom line.

Seeking alpha

AMZY hay making

From the YieldMax website:

The YieldMax™ AMZN Option Income Strategy ETF is an actively managed fund that seeks to generate monthly income by selling/writing call options on AMZN. AMZY follows a strategy that aims to deliver compelling returns, while retaining a defined share in AMZN’s price gains.

The Fund does not invest directly in AMZN. Investing in the Fund involves a high level of risk. Single source risks. Specific characteristics of the issuer may cause an investment in the Fund to be more volatile than a traditional pooled investment that diversifies risk or the market overall. The value of the Fund, which focuses on individual AMZN securities, may be more volatile than the value of a traditional pooled investment or the market as a whole and its performance may differ from the value of a traditional pooled investment or the market as a whole.

The Fund’s strategy will limit its potential gains if AMZN shares increase in value. The Fund’s strategy is subject to all potential losses if the value of AMZN shares declines, which may not be offset by income received by the Fund. The Fund may not be suitable for all investors.

Fund shareholders are not entitled to any dividends paid by AMZN.

AMZY generates income from buying and selling call options on AMZN stock without actually owning any AMZN common stock. Therefore, AMZN’s stock price only indirectly affects AMZY’s price. AMZY aims to provide monthly income rather than capital gains from rising stock price. If you want growth, buy AMZN, if you want income, buy AMZY, while the sun shines (bull market).

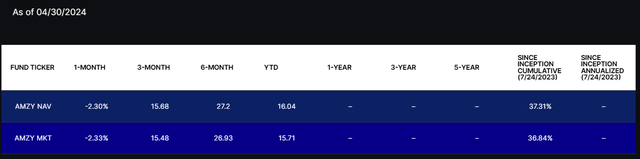

AMZY’s total return performance over the past nine months (as of 04/30/24) has been impressive with a total return of approximately 37% at market price since inception (07/24/23).

Yieldmax

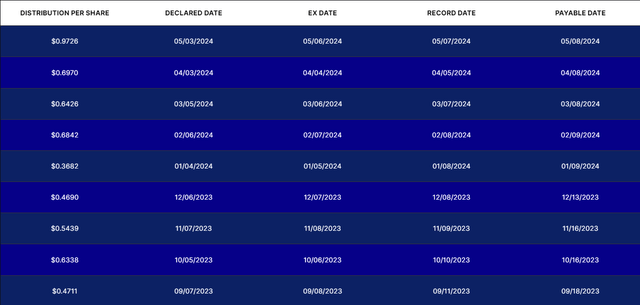

While AMZN’s stock price alone is already up about 20% this year, AMZY has generated a better YTD total return of 23% (assuming dividends are reinvested). For income investors like me, I’m more interested in the income generated by AMZY since its inception in July 2023. Details of AMZY’s distribution are shown in the excerpt from their website:

Yieldmax

The website shows a distribution rate of 51%, which is simply based on the most recent distribution of $0.9726 in twelve, assuming a level distribution. But the dividends are variable and are based on the amount of income earned from options trading that month. The distribution rate and 30-day SEC yield are explained in a footnote, which is also worth reading for those who may be interested in this fund.

**The distribution rate and 30-day stock yield are not indicative of future distributions, if any, on the ETFs. In particular, future distributions on any ETF may differ significantly from the distribution rate or 30-day return of the securities. We do not guarantee distribution within ETFs. ETF distributions (if any) are variable and may vary significantly from month to month and may be zero. Accordingly, the distribution rate and 30-day yield of securities will change over time, and this change may be significant. The distribution may include a combination of ordinary dividends, capital gains, and a return of an investor’s capital, which may reduce the Fund’s net asset value and trading price over time. As a result, the investor may suffer significant losses on his investments. These distribution rates resulting from unusually favorable market conditions may not be sustainable. Such conditions may not continue and there should be no expectation that such performance will be repeated in the future. Additional Fund risks can be found below.

AMZY = high risk reward

The main reason why income investors might want to buy some AMZY now is because all is well with AMZN, but it may not last. Even with a surge in AI spending driving margin growth at Amazon and other big tech companies, the impact of a slowdown in consumer spending will impact everything, including technology spending. This quote from a Morningstar article sums up this concern:

It’s also worth noting that for tech giants like Amazon AMZN, Meta Platforms META, Alphabet GOOGL/GOOG, and Microsoft MSFT, a significant portion of today’s revenue comes from digital advertising, not AI. Advertising is only profitable if consumers continue to spend.

If you want to invest in AMZY for income, I wouldn’t consider it a “buy and hold” investment. You should only buy AMZY if you believe that the value of AMZN will continue to rise in the foreseeable future. I believe AMZN is poised to continue rising as consumer spending remains strong, and the AI revolution is just beginning.

Strong consumer spending

My wife and I had just returned from vacation to Zion National Park, and on Monday, May 20 (while local kids in Las Vegas and southern Utah were still in school), the park was bustling with tourists from all over the world. We had to wait 30 minutes for a shuttle up to the Narrows, which had hikers elbow to elbow when we arrived.

Hike along the banks of the Zion River to the narrow entrance (author’s photo)

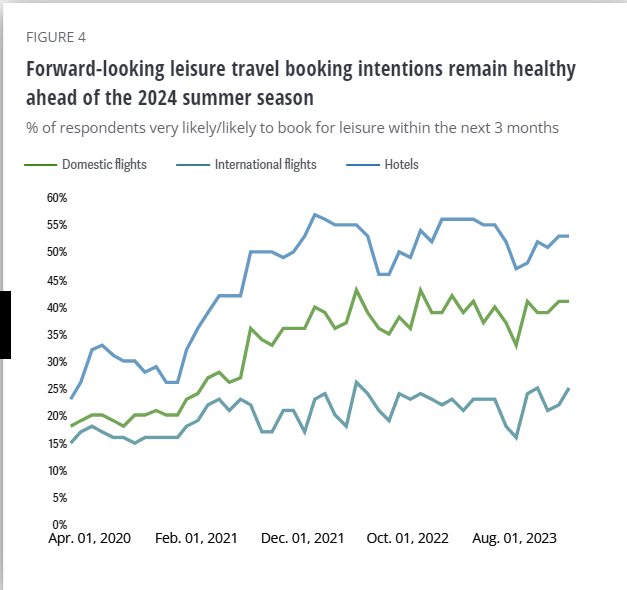

Now I realize this is just one person’s perspective, and it may not be typical in other parts of the country or the world, but at least it seems to me that the US economy is strong, and people are spending. According to this insight from Deloitte, as of April 2024, the consumer is resilient and leisure travel sentiment is particularly strong at the moment.

Deloitte

As of an April 26, 2024 article from Axios, consumers seem “unstoppable”:

The economic surprise in recent years has been the resilience of the American consumer: high borrowing costs and persistent inflation do not hinder overall spending.

In numbers: For the second month in a row, personal consumption expenditures rose 0.8% in March, the strongest in more than a year.

Even after adjusting for constant inflation, spending still rose significantly, with an increase of 0.5%.

AMZN Q124 earnings report results indicate that sales remain strong through 2024.

Sales at the company’s online stores rose 7% while brick-and-mortar stores saw a 6% increase in sales. Third-party seller services grew 16% while ad sales rose 24% due to growth in stores and the Prime Video business. Sales of subscription services increased by 11%.

The artificial intelligence revolution is still in the early stages

Meanwhile, AMZN is starting to take off, and the AI revolution is expected to further boost AWS profits based on Nvidia’s earnings exceeding previous estimates.

Huang added that for every $1 that cloud providers like Amazon, Google and Microsoft spend on Nvidia AI infrastructure, they can earn $5 in immediate GPU hosting revenue over four years.

In fact, Amazon is investing billions in Europe to boost AWS revenue, including €15.7 billion (about $17 billion) in Spain to expand its cloud computing infrastructure by setting up data centers in the country. Amazon intends to invest 7.8 billion euros ($8.44 billion) in Germany until 2040 and about $1.3 billion in France.

From the AMZN Q124 earnings report, AWS revenue delivered strong results with a 17% increase in AWS revenue, beating estimates of 14.7%.

“The combination of companies revamping their infrastructure modernization efforts and the appeal of AWS’ AI capabilities is re-accelerating AWS’s growth rate now at $100 billion in annual revenue,” said CEO Andy Jassy.

However, weak guidance for the second quarter dampened investor enthusiasm somewhat. Any potential slowdown in consumer spending could result in lower-than-expected consumer revenue for the company in the second quarter, which could cause AMZN’s stock price to decline in the second half of the year.

For the second quarter, Amazon expects revenue to range between $144 billion to $149 billion, below expectations of $150.1 billion. Second quarter sales include a negative impact of approximately 60 basis points from foreign currency exchange rates.

AMZN Stock Health and Valuations

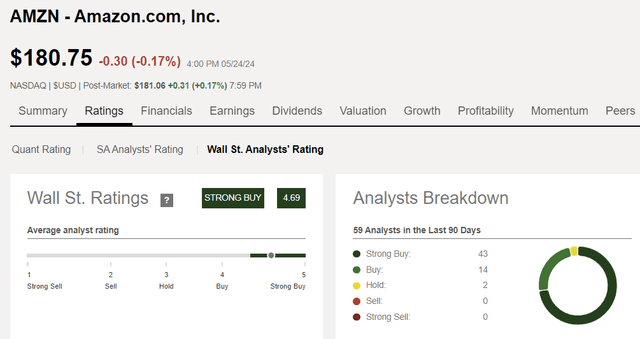

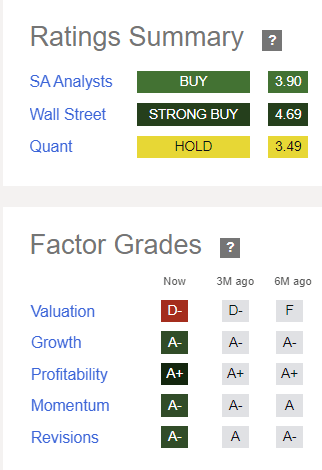

Although the SA Quant rating system only gives AMZN stock a Hold rating, 43 Wall Street analysts give it a Strong Buy, 14 analysts rate it a Buy with only 2 Hold ratings, and SA analysts rate the stock a Buy.

Seeking alpha Seeking alpha

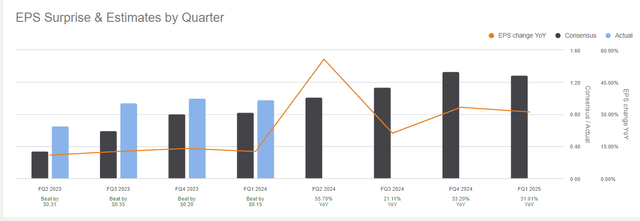

Valuation is the only bad factor, and that’s somewhat understandable with a forward P/E of around 40x. However, AMZN continues to surprise to the upside when it reports earnings, and continues to revise future estimates upward.

Seeking alpha

Amazon delivers, and you might as well enjoy the ride

Like the rest of the Great 7 (excluding Tesla), AMZN posted an excellent first-quarter performance.

Amazon said first-quarter earnings per share were $0.98, while revenue of $143.3 billion was easily above previous estimates. Wall Street thought Amazon’s quarterly results were an indication that any headwinds AWS had faced in the past were over, fueled in part by generative artificial intelligence.

If you’ve ever gone on a hair journey, it can be fun, bumpy, wild, and sometimes exhilarating! Buying AMZY would be like investing in the stock market, in my opinion. Fun while it lasts, but you have to know when to let go. Since AMZN appears to be running full steam ahead and should continue to do so for at least the rest of 2024, I would consider taking a speculative position in your income portfolio for AMZY to “energize” your distributions with its very high monthly yield of around 50% currently. If you do, be sure to keep an eye on consumer spending trends and the health of Amazon as a company, which looks very strong right now, but could change if the economy turns south.