Achisata Khamsuan/iStock Editorial via Getty Images

This is my first look at the drug dictionary (Nasdaq:LXRX). I am fascinated by its good money, approved assets and many late assets. I am frustrated by its meager revenues and exorbitant expenses. that it The overall story certainly highlights another difficult day in the world of pharmaceuticals.

Sources for this article will include documents released in connection with Q1 2024 earnings reported on 02/05/2024 including:

press release – “launch“;

group call – “communicate“;

10-S — “10-S“;

Presentation – “Power point“.

Sotagliflozin, the main treatment offered by Lexicon, faces ongoing developmental challenges.

general

The 10-K filed on 03/12/15 for the period ending 12/31/14 provides the following information on the genesis of sotagliflozin (LX-4211):

Developed internally.

Its main indication at the time was sotagliflozin in the treatment of type 1 diabetes Three phase III trials are in the planning stage;

It intends to stop testing for type 2 diabetes unless it can establish a collaboration partner.

In 2015, Lexicon secured a profitable collaboration on the development and commercialization of Sotagliflozin with Sanofi (SNY).

Zinquista (sotagliflozin)

On 03/2018, the European Medicines Agency accepted for review Sanofi’s regulatory submission for sotagliflozin in the treatment of type 1 diabetes. On 05/2018, the US Food and Drug Administration approved Sanofi’s NDA submission for sotagliflozin, branded ZYNQUISTA. I set the date 03/2019 PDUFA. The Sanofi statement announcing the filing noted that the non-disclosure agreement was based on:

…Data from the inTandem clinical trial program that includes three phase III clinical trials evaluating the safety and effectiveness of Zynquista in approximately 3,000 adults with poorly controlled type 1 diabetes….

On 03/2019, the FDA dropped the application with the CRL. On 04/2019 ZYNQUISTA was approved in the European Union for certain adults with type 1 diabetes and a BMI ≥ 27 kg/m22. On 07/2019 Sanofi terminated its ZYNQUISTA partnership with Lexicon. On 08/2022, EU approval was withdrawn.

As for ZYNQUISTA and the FDA, Lexicon has taken a never-say-never approach. The CRL has appealed; I lost the appeal. She continued to appeal the order. The most recent 10-K (p. 1) describes the multi-year saga in one paragraph as follows:

We are separately seeking regulatory approval for sotagliflozin as a treatment for type 1 diabetes. The FDA issued a complete response letter regarding our New Drug Application (NDA) for the treatment of sotagliflozin in type 1 diabetes in March 2019, which we appealed. Following FDA feedback from recent discussions, we are now preparing to resubmit our NDA for patients with type 1 diabetes and CKD (chronic kidney disease). We report positive results from three phase III clinical trials of sotagliflozin in type 1 diabetes.

Clinicaltrials.com lists the following three completed phase III trials of sotagliflozin in the treatment of type 1 diabetes:

NCT02421510 – Effective completion date 06/2017;

NCT02384941 – Effective completion date 02/2017;

NCT02531035 – Effective completion date 04/2017.

Accordingly, Lexicon is simply arguing with its existing data in an attempt to undermine the FDA, despite losing its previous appeals. This may be effective. Time will tell. The situation is not particularly convincing.

INPEFA (sotagliflozin)

While Lexicon has struggled with its ZYNQUISTA-branded sotagliflozin in treating diabetes, its INPEFA-branded sotagliflozin in heart failure has had more success with the FDA. On 05/2023, INPEFA received regulatory approval from the Food and Drug Administration (FDA) with the following description of the approved indications:

INPEFA is a sodium-glucose cotransporter 2 (SGLT2) inhibitor indicated to reduce the risk of cardiovascular death, hospitalization for heart failure, and urgent visit for heart failure in adults with: • heart failure (1) or • type 2 diabetes, kidney disease Chronic diseases and other cardiovascular risk factors.

As I write on 05/27/2024 it has been a full year since INPEFA was approved. dictionary Power point Slides 6-15 focus on the huge potential that INPEFA approval brings to the lexicon. Notable slides include:

Slide 6 — “By 2030, the burden of heart failure (HF) in the United States is expected to rise to 8.5 million patients and $70 billion in costs”;

Slide 7 – “Hospitalizations and readmissions drive most health care costs”;

Slide 8 – “The SGLT category – including INPEFA – is positioned for significant growth in the treatment of HF.”

Slide 10 – “INPEFA awareness, prescription intent and healthcare provider satisfaction continue to increase as promotional efforts expand across target customers”;

Slide 11 – “INPEFA targeting: approximately 150 cardiovascular specialists focusing on the largest number of cardiovascular prescribers”;

Slide 12 – “Higher volume high frequency prescribers contribute significantly to INPEFA uptake with plenty of room for rapid growth”;

Slide 14 — “INPEFA TRx trading volume rose 26% in Q1 2024”;

Slide 15 — “INPEFA coverage is expected to accelerate during the second half of 2024 as active dialogue with priority payers progresses.”

Judging by these Power point Slides, INPEFA appears to be a crushing blow to the potential for easy success. Maybe, but judging by its first-quarter 2024 revenue after a full year on the market, there’s unlikely to be such a vaunted performance anytime soon.

Lexicon’s finances are likely to falter unless it can boost INPEFA’s revenues

the Power point The financial summary slide below shows that Lexicon is well positioned in terms of short-term liquidity. As for the long-term vision, not so much:

Lexpharma.com

During the communicateCFO Wade revealed full-year 2024 expense guidance for Lexicon, including:

…Expected R&D expenses are between $70 million and $80 million, SG&A expenses are between $140 million and $155 million, and total operating expenses are between $210 million and $235 million. These figures include non-cash expenses of between $18 million and $20 million for stock-based compensation, depreciation and amortization.

At the midpoint of expected amounts, this equates to an annual cash burn of $203.5 million. As for its cash runway during… communicateWade advised:

We expect that our current funds and investments, combined with expected product revenues, will provide us with sufficient resources to run our operations through 2026. And perhaps for a much longer period, if we achieve partnerships, that may be optimal for certain programs, for example, enabling global Phase 3 development of LX9211 via Multiple types of nerve pain.

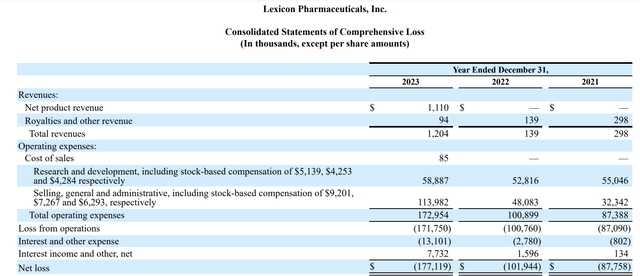

The following excerpt from Lexicon’s most recent 10-K puts Lexicon’s financial performance in historical perspective:

seekalpha.com

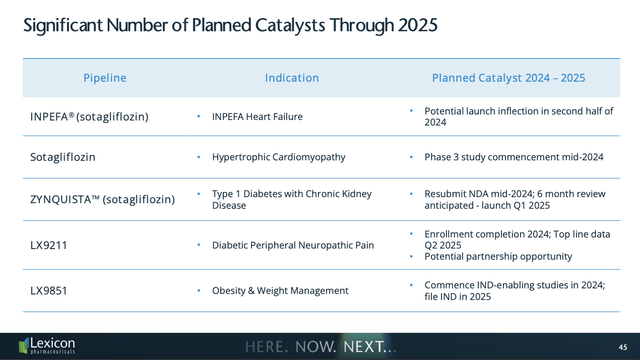

Not good is the best that can be said about this performance record. The Bulls will get rid of him. Power point Slide 45 below lists five points on which the bulls can pin their hopes:

Lexpharma.com

In terms of risk, Lexicon is the top tier

Let me make this as clear as possible, that Lexicon’s market capitalization of approximately US$0.585 billion is not at all justified by its actual performance to date. Since its inception, it has generated a cumulative deficit of approximately $1.815 billion.

It is expected to add significantly to this dismal backlog in 2024. Its only INPEFA-approved treatment had a poor initial launch with revenues of just $1.1 million for the first quarter of 2024. That’s not to say Lexicon is an obvious short-selling candidate.

Take a look at its upcoming catalysts through 2025 as shown on Slide 45. The first of these five teasers assumes a “potential shift to launch in the second half of 2024”. It gives a clear pause to those who tend to be too negative. Is there any logical justification for this?

Two questions during communicate Request additional color on this. In response, CMO Garner noted that Lexicon was counting on growth in both demand and access as drivers of the expected turnaround. In response to a question about the level of expected increase, CFO Wade advised:

…When you look at our overall coverage, it’s about 40%. But a lot of that is under utilization management in terms of step modifications, which in this space, where I think step through drugs, were approved for heart failure relatively recently and are still early in the adoption curve, that’s a very big hurdle. When we negotiate and work with payers to get formularies with contracted coverage, we eliminate those interim adjustments.

So when you look at our Medicare program it’s in the single digits and it has a chance of doubling. And a very big opportunity to significantly increase the business as well when you think about access without that kind of restriction, we think there’s an opportunity to really double the opportunity to — in many aspects, what we’re looking at in terms of the revenue that we get from INPEFA. So I think it’s an important element.

On the one hand, it appears that if there was any market demand for this drug in this indication, it would generate revenues of over $1.1 million after several full quarters on the market. On the other hand, if Lexicon can remove step adjustments from the equation, revenues could rise.

Conclusion

As it stands now, Lexicon’s track record is not worth investing new money on either the long or short side. I classify it as a “wait”. However, it is worth watching.

If it is able to demonstrate that INPEFA will in fact be able to achieve some of its potential to raise multiple revenues, it will be worth seriously considering new investment dollars. As I write on 05/27/2024, this has not happened yet.