Evening pictures

More and more attention is being paid to the supply side of the economy.

The focus…is on labor productivity growth.

Even Treasury Secretary Janet Yellen is raising this topic these days.

My latest effort On the growth of labor productivity in this Last post.

Labor productivity growth appears to be driving the real economic growth occurring in the US economy.

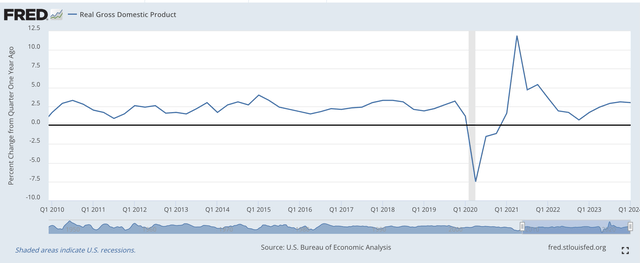

Real GDP Growth: YoY (Federal Reserve)

From the third quarter of 2009 through the fourth quarter of 2019, as you can see, the U.S. economy’s growth rate was in the 2.0 percent range… a little more… a little less.

The compound annual growth rate in the United States during that period was about 2.2%.

Then came the COVID-19 disruptions that continued into 2020 To early 2022. As you can see, economic growth has been everywhere. But starting in the second quarter of 2022, growth seemed flat.

The compound rate of real economic growth has risen to about 2.2 percent annually since then.

Labor productivity growth during the recent period remained at about 2.3 percent.

Thus, since about 2009, the growth rate of the US economy has been roughly equal to the rate of increase in labor productivity.

This outcome, as I have said in previous posts, is consistent with the fate of the economy being fundamentally dependent on the supply side of the economy.

And if you notice, except for the period of time when the US economy was facing the major disruption caused by the Covid-19 pandemic and the subsequent recession, the two variables… economic growth and labor productivity growth have largely moved together.

This is a picture of a supply-side dominated economy.

Two things can be observed, politically speaking, during this period.

It seemed as if the government’s economic policies were focused on longer-term results, and short-term fluctuations in the economic cycle did not receive much attention.

Under the guidance of Ben Bernanke, the Fed focused on a new approach to monetary policy, one that relied on quantitative easing…or, later…quantitative tightening.

Mr. Bernanke stated that this approach to monetary policy would lead to higher stock prices. Rising stock prices would inflate consumer wealth. As consumer wealth rises, consumer spending will rise.

Moreover, if public policy efforts continue over a long period of time, the increase in consumer spending will occur at a steady pace and there will be few larger fluctuations in the economy.

An additional benefit of this approach to monetary policy is that a rising stock market would attract any “excess” wealth created by “inflation” of consumer wealth. This would reduce the money going to consumer price inflation, so the economy would grow steadily, and consumer prices would not spiral out of control by generating consumer price inflation.

The other side of the policy approach, or quantitative tightening, would have almost the opposite effect.

As things were going, before the impact of the Covid-19 pandemic hit the economy, policy achieved roughly what the Fed set out to do.

The economy grew steadily after the end of the Great Recession, unemployment fell, and inflation remained at around 2.2% to 2.3%.

The only real complaint against this approach is that since economic growth depends on labor productivity growth… the supply side of the economy… policymakers have not gotten the economic growth… of about 3.0 percent… achieved in… Previous periods of economic expansion.

But policymakers have had the longest period of economic expansion since World War II. Not too shabby.

On top of that, inflation has remained around 2.3% or so…again, not too bad.

And the stock market went up… and up… and up.

Income/wealth inequality grew very rapidly during this period.

Another comment here: The government’s budget produced a large deficit. However, with low inflation and ample money coming from the Federal Reserve, nominal interest rates remained very low throughout the time period.

During the COVID-19 pandemic and subsequent recession, the Federal Reserve entered into another period of quantitative easing to combat the major collapse of the economy. The government’s fiscal policy has also joined this battle.

Again, this policy seems to have worked things out, but too much money has been put into the economy by the Fed. It appears that much of this money is still in the banking system, even at this late date.

In March 2022, the Federal Reserve entered a period of quantitative tightening to combat inflationary pressures that had built up. We are now in the twenty-seventh month of this quantitative tightening.

The economy appears to still be growing at a pace slightly above 2.0 percent, the unemployment rate remains at a 50-year low, and inflation has fallen but has not yet fallen below the Fed’s 2.0 percent inflation target.

The economy appears to want to return to levels consistent with labor productivity growth, at around 2.3 percent or so.

In fact, many economists now believe…and I do, too…that the US economy will grow by about 2.4% by 2024.

This would be a very good performance if the US economy can achieve 2.4 percent annual growth for 2024.

Moreover, the US stock market hit new historic highs.

So income/wealth inequality continues to rise.

The new approach to monetary policy seems to have worked over the past fifteen years. Taking the Fed “out of the picture” using quantitative easing and quantitative tightening techniques reduces the “shocks” the Fed imposes on the banking system… and thus the economy.

By not building economic policy focused on “aggregate demand,” the Fed… and the federal government… are not constantly “shocking” the economy by changing policies and causing investors and others to restructure their portfolios.

This means that the Fed… and the federal government… do not change their policy positions and, therefore, do not force banks and companies to constantly “guess” about the intentions of the Fed… and the federal government. …Therefore, they are not constantly “guessing” what their strategy should be.

Given the current strategy, the Fed decides on a specific stance… quantitative easing or quantitative tightening… and then lets the financial markets and the supply side of the economy do their work.

This provides a more “stable” environment for investors to build their investment strategies. Investors appear to be benefiting from this environment. Just look at the increases in income/wealth distribution that have occurred.