Nikada

Al Hilal Capital (Nasdaq: CCAP) is a medium-sized institution focusing on private credit financing for small and medium-sized enterprises, which have already achieved a good stage of cash generation.

In December last year, I issued a bearish article on CCAP. The rationale behind The recommendation to avoid BDC lies in the fact that the CCAP portfolio had some quality gaps that made the overall investment case risky. For example, momentum and current levels of non-accrualism were sending the wrong signals about the fundamental defensiveness of investments. Furthermore, CCAP had an above-average leverage factor, which made the profile riskier.

However, in February of this year, after evaluating the Q4 2023 earnings report, I changed my stance on CCAP rating BDC as a Buy. The reason for this was the poor performance of the CCAP share price compared to the combined BDC market With improving fundamentals (eg, increased national insurance per share, decreased leverage etc.).

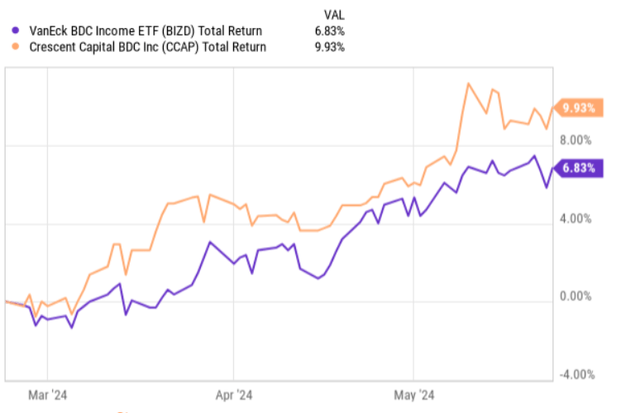

Since publishing my Bullish Thesis Revisited, CCAP has clearly outperformed the market.

Ycharts

Now, CCAP has released its first-quarter 2024 earnings set, which we can evaluate to determine if the bullish case has not exhausted due to the recent rise in the stock price.

Dissertation review

Overall, CCAP was able to record a good performance during the first quarter of 2024, which fully justifies the market reaction by materially raising the share price.

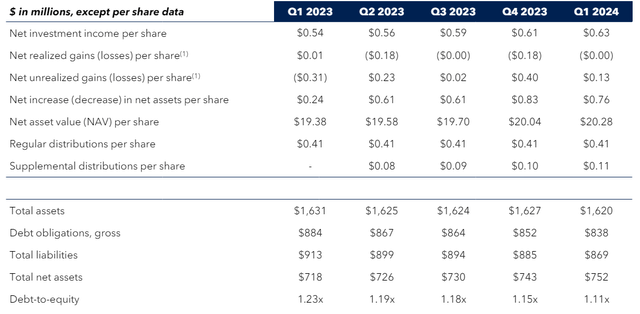

One of the most important items – net investment income per share – came in at $0.63 for the first quarter of 2024 which represents an increase of approximately 3% compared to the previous quarter. If we compare this result with the first quarter of 2023, the improvement would be much stronger. Interestingly, in this quarter CCAP achieved its highest overall quarterly investment income result (about $50 million), with the lion’s share of this arising from recurring cash generation.

In the table below, we can see well how strong momentum CCAP has gained since Q1 2023 through continued growth of net investment income as well as strengthening of its underlying net asset value base. The increase in net asset value was achieved primarily through retained earnings, as both basic and additional earnings did not fully consume the generated cash flow base.

CCAP Q1 2024 Earnings Report

Now, there are many factors that have contributed to the growth of net investment income, but two of them can be considered to be the main ones.

Before I address these two factors in detail, I want to highlight the fact that CCAP’s debt-to-equity ratio has also experienced positive momentum, declining quarter-over-quarter since the first quarter of 2023. In theory, this should create headwinds to the net Investing in CCAP generates income due to a smaller asset base from which CCAP can obtain positive spreads. However, despite this, the administration still fulfills its obligations.

In terms of the key factors driving net investment income higher, the first factor is capturing attractive spreads, which have not trended lower for CCAP for more than 5 consecutive quarters (in contrast to the overall trend in the BDC space). As the net asset base expanded and spreads remained high, net investment income increased accordingly.

The second factor is the presence of some unusual elements that temporarily inflated the results. Over the last two quarters, CCAP recognized non-recurring income mostly from accelerated depreciation, fee income and common stock dividends. These components generated higher than normal cash flows – by about $0.5 million on a quarterly basis. However, if we adjust for these elements, the overall net investment result would still be in positive growth territory for the first quarter of 2024.

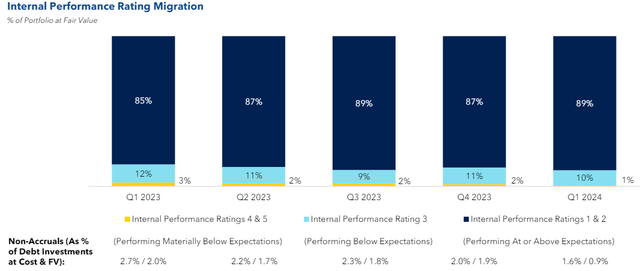

Meanwhile, the core portfolio improved in the first quarter of 2024 compared to the previous quarter. For example, the overall share of well-performing loans (at or above expectations) expanded by 200 basis points, and non-performing loans reached their lowest levels since Q1 2023. This dynamic is not typical of the overall BDC market where several players have registered A deterioration in portfolio conditions (including a rise in non-accrual positions).

CCAP Q1 2024 Earnings Report

Finally, as a result of the above data points and strong momentum in fundamentals, CCAP announced an increase in fundamental earnings of $0.1 per share. In the context of CCAP’s track record of delivering stable, uninterrupted dividend flows for 22 consecutive quarters, the recent dividend increase is a strong message about the sustainability of the current yield.

Bottom line

The first quarter 2024 results confirm that CCAP is already enjoying positive momentum in the core metrics of its business.

The portfolio continues to gradually expand, with external leverage playing a less significant role as most of the growth has been absorbed through retained cash generation. The growth in the portfolio combined with CCAP’s ability to protect spreads from the systemic pressure that currently applies to many BDCs, contributes well to the net investment income figure.

Another aspect worth appreciating is the positive dynamics at the quality end of the portfolio, where exposure to well-performing investments increased, while non-accruals decreased further to very insignificant levels (~0.9% of portfolio value).

In short, Crescent Capital is an obvious, defensive buy for BDC investors, who seek income stability combined with an element of steady growth.