Kencheruti/iStock via Getty Images

About a year ago, I wrote a preliminary article reviewing the Fairlead Tactical Sector ETF (NYSEARCA:Tech). I have been cautious with the fund’s strategy, as TACK’s “systematic technical model” is new and untested.

With a year Let’s review TACK’s performance and see if my cautious stance is appropriate.

Looking at the returns from inception, the TACK ETF does a good job of limiting major drawdowns. However, when it comes to bullish participation, the TACK ETF has lagged significantly behind the S&P 500 because its models can be too slow to adjust.

For investors looking for a low drawdown fund with good vertical engagement, I suggest they look elsewhere.

Brief overview of the fund

The Fairlead Tactical Sector ETF uses a systematic technical analysis approach to manage a portfolio of sector ETFs and alternative assets such as bonds. And gold.

TACK ETF is managed by Katie Stockton, a frequent market commentator and guest on CNBC. She was previously Chief Technical Strategist at BTIG and Chief Market Technician at MKM Partners.

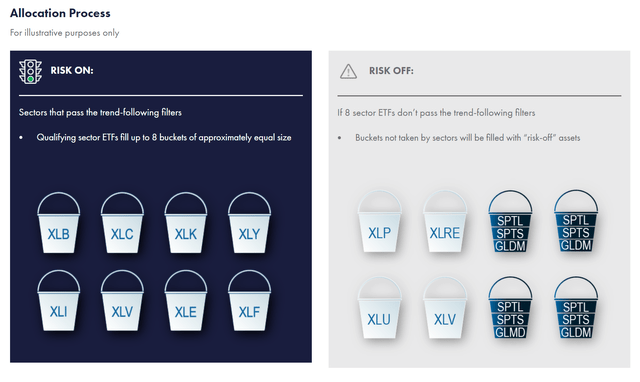

The TACK ETF uses a systematic “trend following” filter to evaluate 14 ETFs for inclusion/exclusion in the fund (Figure 1). When markets are considered “risk on,” the TACK ETF will allocate to risk ETFs such as the Select Materials SPDR Fund (XLB) and the Communications Services Sector SPDR Fund (XLC). When markets are “risk off”, the TACK ETF will be allocated to defensive sectors like the Utilities Select Sector SPDR Fund (XLU) or alternative assets like the SPDR Gold Minishares ETF (GLDM).

Figure 1 – TACK strategy overview (fairleadfunds.com)

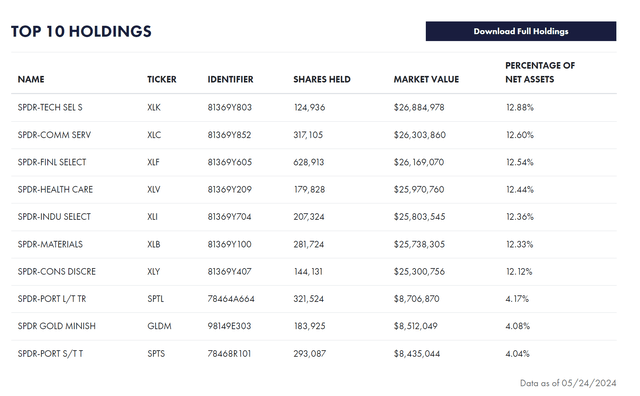

Currently, we can see that the TACK portfolio is somewhat “high risk”, as it has allocations to all “aggressive” ETFs except the Energy Sector SPDR Fund (XLE) (Figure 2). Defensive holdings are also minimal, with only 12% of the portfolio allocated.

Figure 2 – TACK portfolio holdings (fairleadfunds.com)

The purpose of the TACK investment strategy is Benefit from sector leadership While protecting the wallet from large withdrawals through active withdrawals Asset distribution.

Weaknesses in the strategy

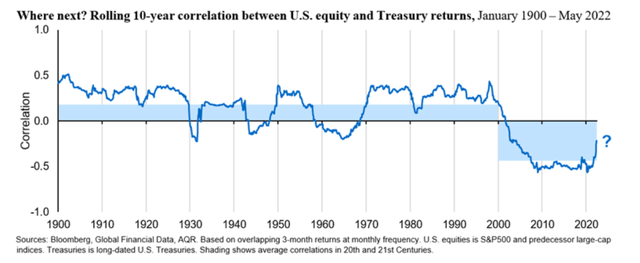

In my previous article, I mentioned two concerns that I can foresee regarding the TACK strategy. First, TACK’s “risk off” allocation makes the implicit assumption that alternative assets such as long-term Treasuries, as represented by the S&P Portfolio Long Term Treasure ETF (SPTL), will provide a hedge against market withdrawals. This is based on the negative correlation between stocks and Treasuries that has been in place since the early 2000s (Figure 3).

Figure 3 – Relationship between Treasuries and Stocks (Investment and Pensions Europe)

However, the relationship between bonds and stocks is not constant. As we saw in 2022, both the SPTL and SPDR S&P 500 ETF Trust (SPY) suffered significant losses as the Fed raised interest rates, causing bonds and stocks to repricing (Figure 4). When the correlation is positive, the effectiveness of TACK hedges is reduced.

Figure 4 – SPTL and SPY both decline in 2022 (Searching for Alpha)

Another concern I had with the TACK ETF was that its “systematic trend following” filter seemed to have significant lag, such that even though many sectors had broken out with new uptrends in 2022, the TACK ETF was still in Very defensive posture when he reviewed the box.

TACK performed poorly from the start

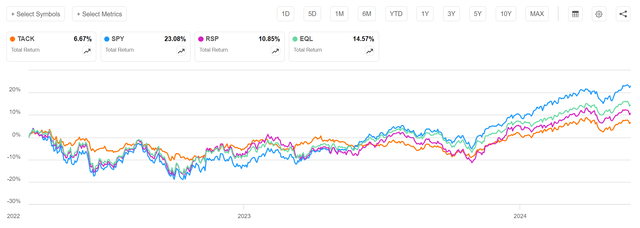

Ultimately, these two weaknesses caused the TACK ETF to significantly lag the SPY ETF from the start, with the TACK ETF returning 6.7% compared to 23.1% for the SPY ETF, 10.9% for the Invesco S&P 500 Equal Weight ETF (RSP), and 14%. 6%. ALPS Fund Percentage of Sector Equal Weight (EQL) (Figure 5).

Figure 5 – TACK underperformed SPY (Searching for Alpha)

Good defense but not enough attack

Given the two weaknesses mentioned above, the main driver of TACK’s poor performance appears to be the lack of violations. For example, from TACK’s inception (03/23/22) to January 25, 2023, when it crossed the 50 DMA above the 200 DMA on the SPY ETF (50 DMA below 200 DMA is typically associated with a bear market), TACK fulfilled the ETF ) promised to reduce withdrawals, falling 1.1% compared to 8.6% for the SPY ETF (Figure 6).

Figure 6 – TACK Low drawdowns during bear markets (Searching for Alpha)

However, since January 25, 2023, Spy has left TACK in the dust, returning 34.7% compared to 7.9% for TACK (Figure 7).

Figure 7 – TACK was very slow to turn to risk (Searching for Alpha)

While trend-following strategies are expected to underperform in the long term because the model needs time to shift from “risk off” to “risk on,” this level of underperformance may be untenable for a fundamental holding in Any investor’s portfolio.

Think of other ways to reduce withdrawals

For investors concerned about market drawdowns, I suggest they consider other investment strategies rather than the “systematic trend following” used by the TACK ETF. For example, investors could consider the JPMorgan Hedged Equity Fund (JHEQX) which uses a “put-the-collar” strategy.

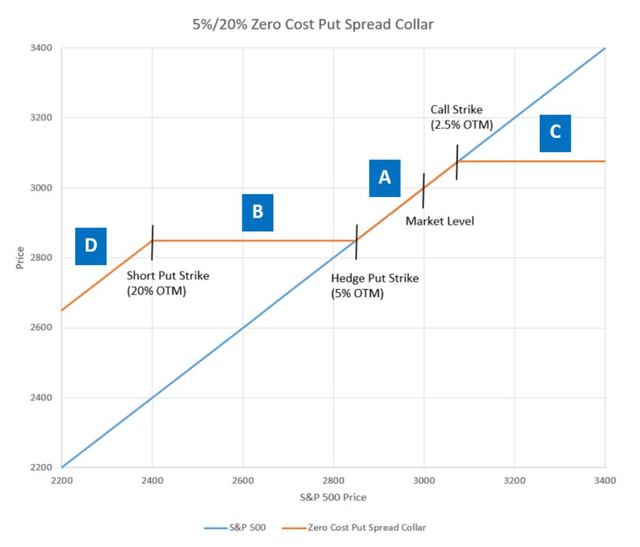

The Put Collar strategy has a 5%-20% spread on the S&P 500 Index that is funded by selling at-the-money (“OTM”) calls on the index (Figure 8). By owning the put spread, the JHEQX Fund is protected from average drawdowns of 5-20% on the S&P 500, although large market incidents in a short period such as the COVID-19 collapse can still cause drawdowns larger than 5 %.

Figure 8 – Illustrative strategy for placing collars (swanglobalinvestments.com)

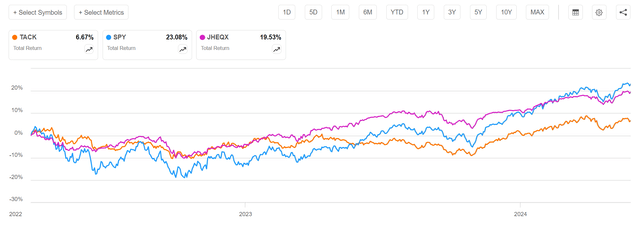

When measured since the start of TACK, JHEQX has matched TACK’s drawdowns by approximately 1% but has performed much better since the markets entered a new “bull market” (Figure 9). Overall, JHEQX has returned 19.5% since March 23, 2022, compared to 6.7% for TACK and 23.1% for the SPY ETF.

Figure 9 – JHEQX vs. SPY and TACK (Searching for Alpha)

Although JHEQX has a high investment hurdle of $1 million minimum investment, JPMorgan recently launched an ETF based on a similar strategy, the JPMorgan Hedged Equity Laddered Overlay ETF (HELO), which does not have the same strict minimum investments. I last wrote about the HELO ETF here.

Conclusion

The TACK ETF is a ETF that systematically allocates to sector ETFs based on their trend-following characteristics.

Unfortunately, my initial concerns are starting to show as the TACK ETF has significantly lagged the S&P 500, particularly in the current uptrend, and its strategy lacks offensive power.

For investors looking for funds that can limit drawdowns while still providing decent upside participation, I suggest investors consider the HELO ETF that uses a “divergent collar” to protect investors from large drawdowns.

I rate the TACK ETF as either Avoid or Avoid Catch.