com.FinkAvenue

Investment thesis

Since my last report on IBM (New York Stock Exchange: IBM)(New: IBM: California) In January, the company’s shares fell despite largely beating revenue estimates for the quarter. This stems from IBM’s recently announced acquisition which I believe it is Strategically, it was not well received in the market. Contrary to market sentiment since the last earnings report, I still maintain a positive view on the acquisition, and believe the market has misunderstood its potential benefits.

However, IBM has maintained its leadership position by aggressively pushing open source AI, which I consider to be the most important open source development since Linux.

I am confident that these areas are crucial in terms of driving the company’s growth and helping it maintain a competitive advantage in its industry in the rapidly evolving technology landscape. Therefore, despite the current market sentiment, I see IBM’s growth supported by its strong fundamentals and initiatives, as a factor influencing my continued strong belief in purchasing.

Why am I covering the follow-up?

While the market response has been lukewarm, I believe that strong growth in IBM’s core business segments and innovation in AI and cloud technologies is fueled by its open source partnerships and initiatives, suggesting that IBM is undervalued.

Despite the slight downward trend in IBM stock since my last report, the company’s AI and cloud technology innovations continue to sustain its future financial performance.

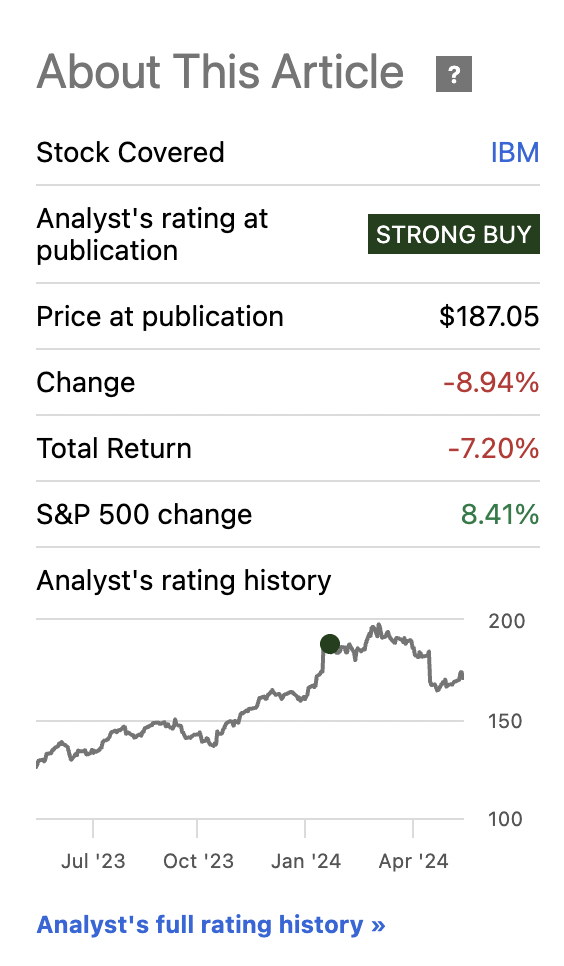

IBM stock performance (Searching for Alpha)

Additionally, I believe the company’s partnership with Meta (META) to integrate the Llama 3 model into the WatsonX AI platform will bring significant benefits due to the company’s more aggressive push for open source AI models in areas such as content creation and business analytics. Llama 3 has been tested for GPT-4 level capabilities, including reasoning and reasoning. I think this means that open source capabilities can jump significantly from here given the release of this new paradigm.

In light of these developments, I wanted to write an update to show how the company continues to execute, but the market is not rewarding it, creating an interesting opportunity. I believe that expanding IBM’s technology stack with AI capabilities with Meta, coupled with continued innovations in hybrid cloud solutions, positions IBM favorably for future growth.

Open source is great for IBM

Open source AI promotes transparency because the code and algorithms are available to everyone to enhance trust among users (in this case enterprise customers) and foster a broader base of developers to contribute to AI development. But even experts have not agreed on how to improve and use open source AI (I think this is fundamental).

One reason for this is that this technology is expected to scale through collective expertise and contributions, democratizing access to technology. In other words, there is little that can stop its growth. Companies, researchers, and developers from around the world can use and improve open source AI without the barriers and financial constraints imposed by proprietary systems. Openness can accelerate the pace of innovation because developers do not need to reinvent the wheel, but rather build on existing, openly available foundations.

This is critical in industries where proprietary solutions may not provide the necessary functionality or where the costs of such solutions are prohibitive to reduce the overhead associated with licensing fees and enable organizations to scale their AI applications without additional costs. Open source is big because it means companies can tailor tools to their operational requirements by modifying and adapting software without licensing restrictions or ownership restrictions. They can modify AI to integrate with their existing systems, customize it to suit their specific use cases, and even enhance its capabilities beyond the original scope. For reference, this is almost always how the organization works. Open source AI will continue to allow them to do this.

What management says

CEO Krishna asserted that “…the impact of AI will be of the same order as the steam engine or the Internet.”

IBM’s open source AI initiatives, such as developing Granite models and collaborating with NASA to create open source scientific foundation models, solidify their commitment to open source frameworks.

The company’s commitment to open source AI is evident in initiatives and collaborations that advance innovation and development of responsible AI through the AI Alliance, which includes more than 50 organizations aiming to create an open community to accelerate the development of responsible AI systems. . A collective move toward creating a unified approach to open AI will ensure that advances in AI technology adhere to the principles of safety, security, and ethical considerations. The Alliance focuses on creating an environment consistent with broader societal values and needs.

Recently, James Cavanaugh, IBM’s CFO, explained during the JPMorgan Global Technology, Media and Telecommunications Conference that the company is seeing significant growth in its annual recurring revenue (ARR), highlighting a $14 billion book of business overall, growing at 8%. , and an ARR for Red Hat OpenShift of $1.25 billion. They also increased Red Hat’s Q1 2024 bookings by more than 40% to emphasize IBM’s strong software and cloud services. Open AI is more than just a philosophy embraced by IBM. It’s a business model that drives growth.

evaluation

I believe IBM’s current market valuation, when compared to its growth prospects and position in the industry, indicates that the stock may be significantly undervalued. Right now, IBM shares are trading well below the average P/E ratio in the sector. For example, IBM’s forward P/E (GAAP) ratio of about 19.67 trails the technology sector’s forward earnings multiple of 30.18.

Despite the low P/E ratio, IBM’s EPS estimates show strong growth, well above the sector average. IBM’s expected EPS growth is strong, with a forward-looking growth rate that significantly exceeds the sector average. IBM’s GAAP EPS growth is expected to reach 70.53% year over year, compared to the industry average of just 7.01%. This impressive growth is driven by IBM’s integration of artificial intelligence and cloud computing into its service offerings, as well as recent acquisitions such as HashiCorp, which are expected to help accelerate revenue and ultimately earnings growth.

Given this, if IBM shares converge only halfway between their current P/E and the sector average, there is significant upside potential. Specifically, moving from the current P/E ratio to the midpoint of about 24.93 (about halfway between 19.67 and 30.18) represents a potential stock price appreciation of about 27%. This is calculated based on the ratio improvement as well as the direct impact the rerating will have on the stock price, assuming earnings remain flat or improve.

The potential for this rerating is underscored by the company’s operational improvements, which may not be fully recognized by the market, in my view. Additionally, their strong EPS growth outlook puts their profitability on at least a borderline equivalent path this financial year, in contrast to the broader sector’s performance.

How does this compare to previous valuation estimates?

Previously, I wrote about how I wanted to compare IBM’s forward P/E ratio with Accenture’s forward P/E ratio, and this represented an upside of 48.3% at the time.

Since then, I remain bullish on the stock, but I offer a short-term upside estimate of 27% while they can still converge long-term at Accenture’s P/E ratio where the market sees Big Blue as well-positioned. A real acceleration trend in my opinion.

First risk: PEG

IBM’s current PEG ratio is 4.16 on a non-GAAP basis, which is higher than the industry average of 2.01. This implies that the market may be overvaluing IBM’s growth outlook relative to its earnings, which I think may lead to some current concerns about the stock being potentially overvalued.

Even with this high PEG ratio, IBM’s strong earnings per share (EPS) growth could alleviate concerns about its extended PEG ratio (that is, if it lives up to its expectations). Again, the company is expected to see strong GAAP EPS growth this year, which I think will justify this high PEG ratio.

The second danger: open source regulation

While IBM is working to leverage open source AI, governments are not keen on using it. The European Union passed a law in March 2024 to rein in various uses of artificial intelligence. Because open source AI allows anyone to download, modify, and publish AI models without strict oversight, it carries risks that include the potential for creation of malicious or misleading content, unauthorized surveillance, and even the development of autonomous weapons or other dual-use technologies. Which can be used maliciously.

In response to these concerns, the European Union has implemented the Artificial Intelligence Act, the first comprehensive legislation of its kind to regulate the development and use of AI technologies across member states. This law classifies AI systems into risk categories, and imposes more stringent requirements on high-risk applications to promote transparency and accountability across all AI deployments. For open source AI, this includes mandates on documentation and transparency. However, it allows some flexibility for non-commercial or research-based initiatives.

IBM announced that it recognizes these challenges and has developed tools and protocols to comply with these regulations and support safe AI development. For example, the company’s introduction of watsonx.governance provides organizations with the resources to effectively manage AI-related risks and ensure compliance with evolving regulations such as the EU AI Act. I believe that this balanced innovation in artificial intelligence will play a fundamental role in enhancing the company’s contributions to the artificial intelligence sector by working within a framework that mitigates potential harms.

minimum

I believe IBM represents a compelling investment opportunity because of its innovations in open source AI that will lead to significant transformation and acceleration for Big Blue. The company’s stock, which is currently undervalued based on its GAAP forward P/E ratio, represents a unique opportunity for investors in my view. IBM’s ability to leverage its open source initiatives will lead to significant growth and will reflect the impact that open source projects like Linux have had on the industry.

I also believe that IBM’s recent collaboration with Meta to integrate the Llama 3 model into their AI offerings is a very important effort to enhance the legitimacy of open source AI. Llama 3’s generative AI capabilities extend IBM’s technology expertise to lead in high-growth, high-value areas of the technology industry.

IBM’s strategic acquisitions, including its recent purchase of HashiCorp, should solidify its commitment to strengthening its cloud services and infrastructure. Although I acknowledge that these acquisitions carry inherent risks, they are still crucial to IBM’s long-term strategy to dominate cloud computing and AI. I maintain a strong buy. I am optimistic.