The good one

introduction

I just read an interesting article in the Wall Street Journal that discussed the accelerating trend of shoppers buying store brands to deal with rising inflation.

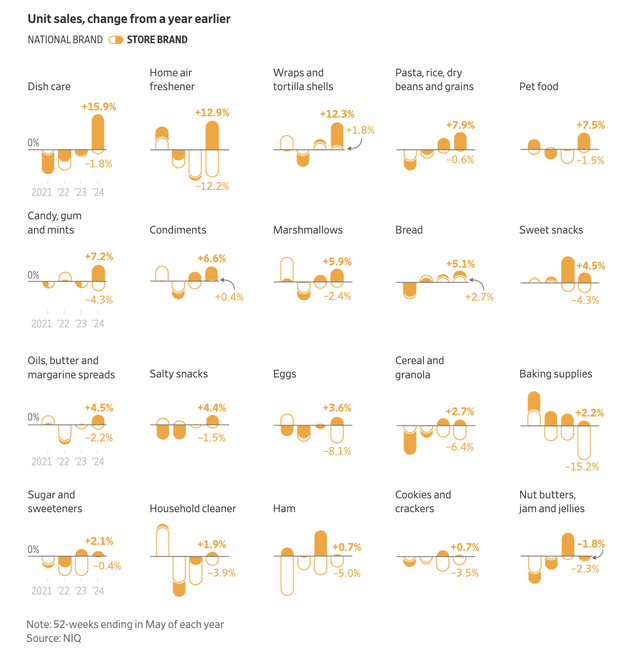

As we see below, demand for store brands has exploded, including products in the categories in which the companies operate Tend to be low customer loyalty, such as dish care, air fresheners, pasta, candy, etc.

The Wall Street Journal

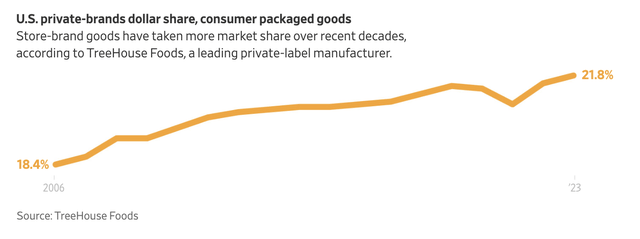

Looking at the chart below, we see that nearly $0.20 of every dollar spent in grocery stores goes toward private-label products – this is the highest number “ever.”

The Wall Street Journal

Also note the acceleration after the pandemic, when inflation became an issue.

The reason I bring this up is to show the lasting impact of inflation which is still very ‘sticky’.

I also bring this up because I recently wrote an article titled “High and low returns Multiples – 3 of my favorite dividend stocks to buy now.”

In that article, I explained my intent to own stocks with attractive valuations, inflation protection, and wide moats to prepare for what could be an unfavorable market environment, as Jamie Dimon, CEO of JPMorgan, explained:

“Stocks are very high, and I think the chance of inflation staying high or interest rates rising is higher than people think,” the CEO said. “My view is that whatever the world is calculating for a soft landing, I think it’s probably half that. I think the chances of something going wrong are higher than people think.” —Jamie Dimon via Bloomberg

One of the stocks I highlighted in that article was AbbVie (New York Stock Exchange: ABBV)the first healthcare stock I bought for my dividend growth portfolio.

Since my last in-depth article on AbbVie was written on February 5, it’s time for another focused article explaining why I consider AbbVie to be one of the best growth/income hybrids on the market.

So lets get to it!

The perfect combination of growth and value

Ignoring special dividends, AbbVie is the fifth highest yielding stock in my portfolio for dividend growth.

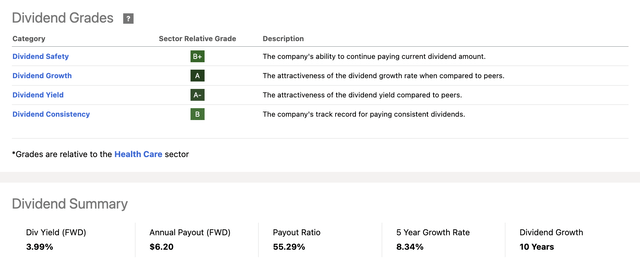

The company currently pays $1.55 per share each quarter, which translates to a yield of 4.0%.

These earnings come with a very favorable alpha earnings scorecard, supported by a payout ratio of 55% and a five-year CAGR of 8.3%.

Seeking alpha

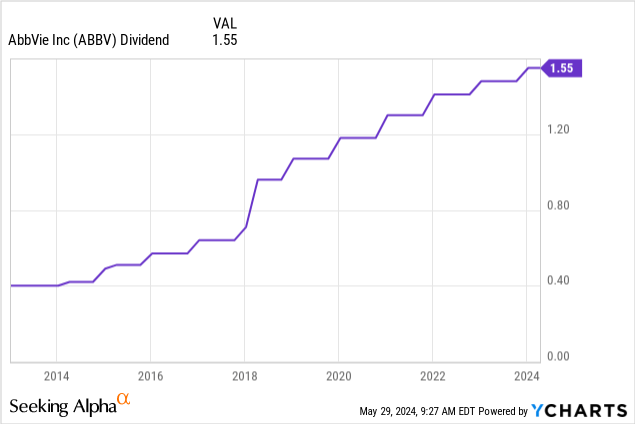

Furthermore, the company has increased its dividend every year since it was spun off from healthcare giant Abbott Laboratories (ABT) in 2012.

Also, technically, AbbVie is the dividend king with 50 or more consecutive annual dividend increases, where Abbott has that status.

Both Abbott and AbbVie have raised their dividends every year since their split.

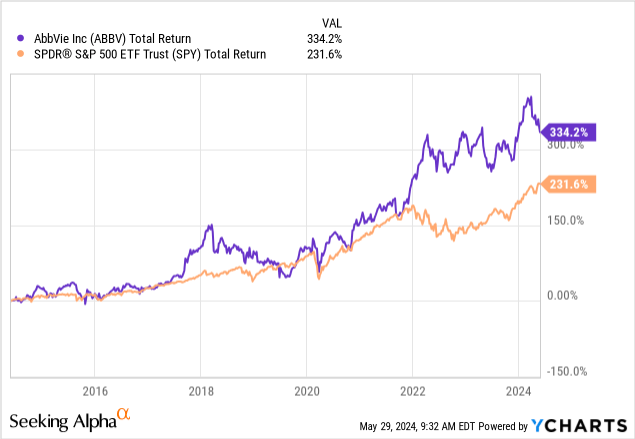

Furthermore, the company has a very positive total return, with the pharmaceutical giant with a market cap of $275 billion generating returns of 334% over the past 10 years, beating the S&P 500’s return of 232% by a wide margin.

This outperformance includes periods of high uncertainty, such as losing the patent on its flagship drug, Humira.

I’ve added emphasis to the quote below to highlight the size of the deal (and still is):

Humira, which enjoyed market exclusivity for 20 years until its patent expired at the beginning of 2023, has achieved great success. $21.2 billion for pharmaceutical company AbbVie in 2022 and about $200 billion since it first came to market.. -Health care drink

The good news is that AbbVie continues to demonstrate its ability to innovate, strengthen its portfolio, and set the stage for what I expect will be many years of high shareholder returns and capital gains.

AbbVie’s future is bright

During Bank of America’s healthcare conference earlier this month, the company highlighted its strongest benefit: a great product portfolio.

The company’s growth platform represents about 80% of its business, with growth in the mid-teens.

Furthermore, despite challenges like the aforementioned Humira erosion, the company’s growth platform is performing well, with $5.6 billion in growth this year alone and growth in the mid-teens from its previous Humira platform in the first quarter.

In the first quarter, total revenue was $12.3 billion, $400 million higher than the company expected.

The previous Humira platform saw growth of more than 15%.

Our first quarter results were well above our expectations, driven by excellent performance from Humira’s previous growth platform. Based on our strong results and significant momentum, we are raising our full-year forecasts. ABBV earnings announcement for the first quarter of 2024

The new guidance sees adjusted EPS at between $11.13 and $1.33, with net sales of at least $55 billion — $800 million more than previously expected.

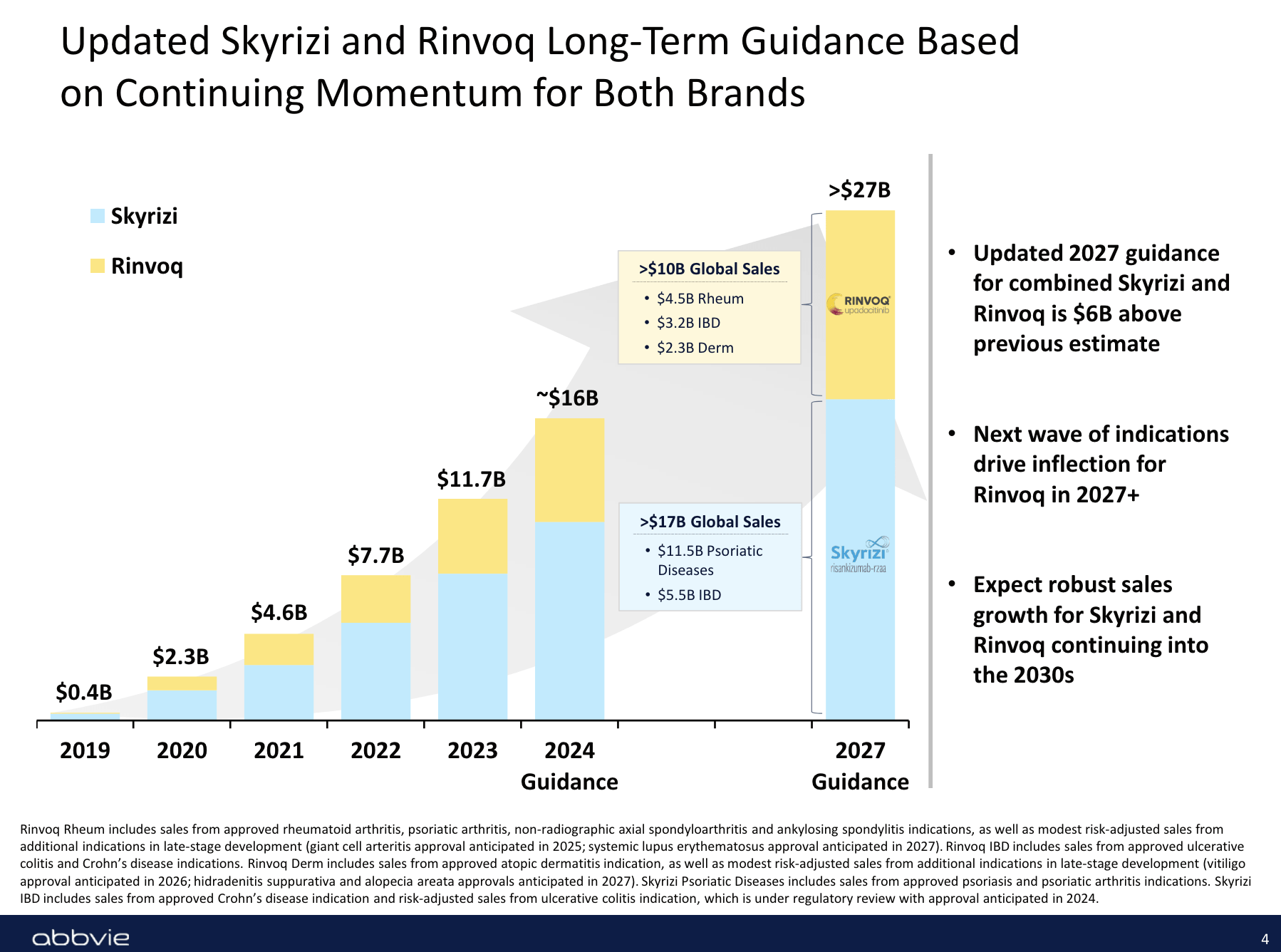

Two notable properties I also mentioned in “High returns and low multiples“They are Skerries and Renfolk.

These two properties achieved combined growth of over 50% in their fifth year on the market.

To add some color, Skyrizi, with global sales of $2 billion and operating growth of 48%, has significantly improved its position as a market leader in biologic psoriasis treatment.

Biologic medications differ from systemic medications because they do not target the entire immune system.

Likewise, Rinvoq achieved global sales of US$1.1 billion, which represents an increase of 61.9%.

Sales of these two drugs are expected to exceed US$27 billion by 2027, which will rise from US$16 billion in 2024E – a CAGR of 19%!

AbbVie

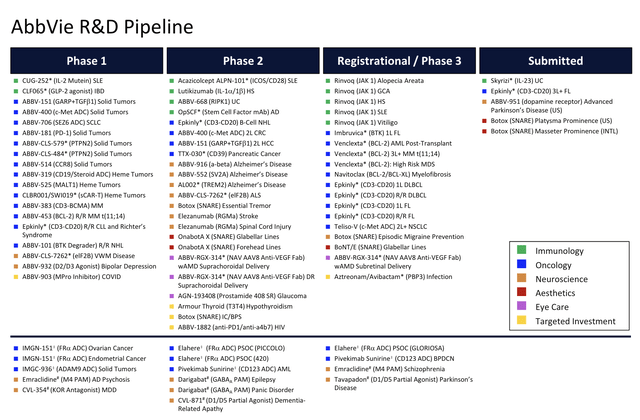

Better yet, the company has a promising pipeline, including oncology programs, such as 383, a bispecific BCMA CD3 in myeloma, and 400, an ADC that uses the Topo-1 warhead.

If you’re wondering what an ADC is, you’re probably not alone.

ADCs are an emerging class of drug compounds that combine the efficacy of anticancer drugs (often called payloads) with the specificity of mAbs to the tumor site, thus Combined chemotherapy and immunotherapy. – National Institute of Health

Please also note that the Topo-1 warhead is not a weapon designed by a US defense contractor but rather a Topoisomerase I inhibitor, which is critical in delivering drugs to tumors.

Speaking of oncology, ImmunoGen’s acquisition of the company adds tremendous value to its oncology platform.

The addition of ImmunoGen therapy for ovarian cancer will accelerate our ability to help patients today, expand our oncology pipeline, and drive long-term revenue growth over the next decade. – ABBV

In addition, the anticipated approval of new indications, such as UC for SKYRIZI (see overview below) and additional indications for RINVOQ, covering conditions such as vitiligo, HS, alopecia, lupus, and GCA, are expected to drive growth.

AbbVie

According to the company, RINVOQ indications alone will add “A few billion dollars at peak revenue.“

Please note that these forecasts are included in the 2027 indicative chart I showed in this article.

Beyond innovation, the company’s commercial strategy focuses on improving its core market presence and expanding into neuroscience and oncology.

In order to grow successfully here, the company is improving its marketing efforts and strategic partnerships to gain market share more quickly.

As a result, the company expects high single-digit annual revenue growth through the end of the decade, which bodes very well for its valuation, earnings growth and overall TSR picture.

evaluation

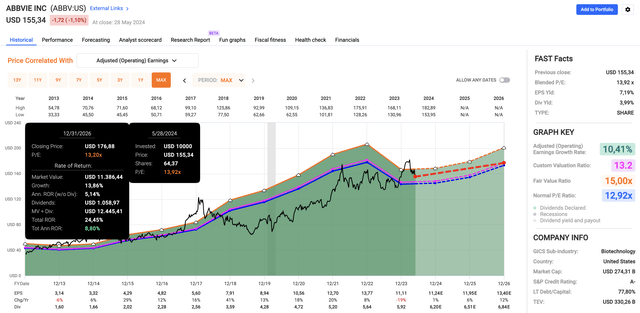

AbbVie, which has a credit rating of A-, is trading at a blended P/E of 13.9x, which is slightly above its normalized 10-year P/E ratio of 13.2x.

Quick charts

Looking at the FactSet numbers in the chart above, analysts expect EPS growth to accelerate, from a 19% decline in 2023 (due to Humira) to 1% growth in 2024 and 12% growth in 2026.

Combining this with a dividend of 4% and a multiple of 13.2 times, we get an expectation of annual returns between 8 and 10%, which I would expect to come in at the upper end of that range if the company can maintain double-digit annual EPS growth after… that. 2026.

As a result, I continually buy more ABBV shares based on corrections, making them the cornerstone of my dividend growth portfolio.

He stays away

In light of the challenging macroeconomic environment, one standout company in my portfolio is AbbVie, which offers an ideal mix of income and growth.

Despite the loss of the Humira patent, AbbVie’s innovations and strong product portfolio, including drugs like Skyrizi and Rinvoq, are driving its impressive performance.

Furthermore, with a promising pipeline and strategic expansion into oncology, AbbVie is poised for sustained growth, which could see sustained double-digit annual EPS growth.

Hence, trading at a reasonable valuation with a 4% dividend yield, AbbVie remains the cornerstone of my dividend growth strategy.

Pros and Cons

Positives:

- Juice Profits: AbbVie offers an attractive, well-covered 4% yield with consistent upside.

- Growth potential: With promising drugs like Skyrizi and Rinvoq, AbbVie is in a great position for significant growth.

- innovation: AbbVie’s ability to innovate and expand in areas such as oncology comes with long-term growth opportunities.

- evaluation: By trading at a reasonable P/E ratio, AbbVie stands out in the market with a high overall valuation.

cons:

- Loss of Humira patent: The recent expiration of Humira’s patent shows the biotech giants’ vulnerabilities.

- Relying on innovation: AbbVie’s growth depends heavily on the success of new drugs and mergers and acquisitions.

- a race: The pharmaceutical sector is highly competitive.

- Regulatory risks: Changes in healthcare regulations and drug approval processes could negatively impact AbbVie’s operations and profitability.