OXLCM: CEF securities are maturing, looking for a high-yielding alternative (NASDAQ:OXLCM)

-Oxford-/E+ via Getty Images

thesis

Series Preferred Stock 6.75% for 2024 (Nasdaq: OXSLSM) are exchange-traded fixed-term preferred shares of a closed-end fund of Oxford Lane Capital Corporation (OXLC). We covered these securities last year here, where we designated them ‘Buy’ rating based on short maturity, low risk and high returns. The securities have generated a steady stream of income ever since, outperforming Treasury funds. With the redemption deadline approaching soon at the end of June, investors need to start deciding which alternative securities to enter into once they have the full principal amount of the notes in their accounts.

In this article we will provide a comprehensive overview of CLO to equity CLOs, the ongoing need for leverage, explore the alternatives available from the OXLC capital structure and the larger market it can be used to replace. OXLCM in the investor’s portfolio.

Total setup for CLO equity funds

CLO stocks have become a sought-after asset class in the past year, with many institutional pension funds allocating increasing capital to the sector:

Pension plans and insurance companies have been piling into funds that invest in equity tranches of collateralized loan obligations in recent months, according to a number of asset managers who spoke on condition of anonymity. The inflows have helped a slew of hedge funds and other money managers, including GoldenTree Asset Management, Sculptor Capital Management and Carlyle Group Inc. and CVC Credit Partners, have raised at least $3.1 billion in less than a year for strategies dedicated to these investments alone. .

Source: Bloomberg – “Hedge funds are drawing pension money into the riskiest corner of the $1.3 trillion credit market“

The low default rate environment combined with high risk-free rates has favored CLO stocks. However, OXLC is not just accumulating CLO shares, it is buying them with more leverage on top. OXLCM is a form of leverage of the fund.

Continued demand for the asset class will translate into the IMF maintaining the same level of leverage, and thus there is potential for a new name issuance to replace the outstanding term preferred security, although the Fund has been issuing a significant amount of common stock of late as we will see shortly.

Financing adjustments

Let’s take a quick look at how the leverage portion of CEF currently stacks up:

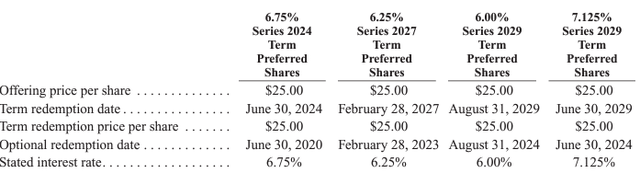

Term preferred stock (Annual Report)

According to the EEF Annual Report, the above represents the current preferred shares issued by the CEF. In addition, the Fund also has outstanding notes:

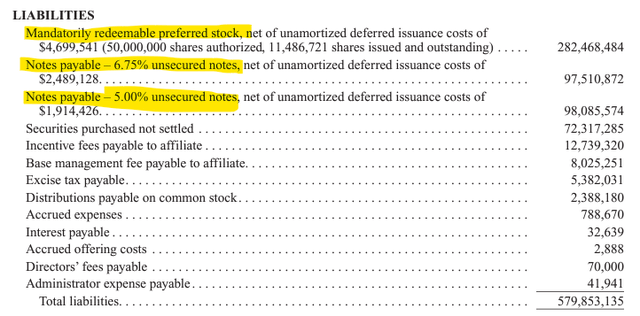

- $100 million principal amount of 6.75% senior unsecured notes due 2031. The 6.75% notes will mature on March 31, 2031 and may be redeemed in whole or in part on or after March 16, 2024.

- $100 million principal amount of 5.00% senior unsecured notes due 2027. The 5.00% notes will mature on January 31, 2027 and may be redeemed in whole or in part at any time after January 31, 2024.

We can see the above liabilities neatly summarized in the fund’s balance sheet:

CEF Commitments (Annual Report)

OXLCM represents $68 million in financing that is due soon. However, the Fund has been very active in issuing new common shares:

Issuing new shares (SEC Notice)

To maintain the same amount of leverage as before, the math suggests that the CEF must issue an alternative term for the preferred equity tranche. However, with spreads being so tight in credit markets, the CFC may choose to run a lower leverage ratio for a period of time.

What are the alternatives?

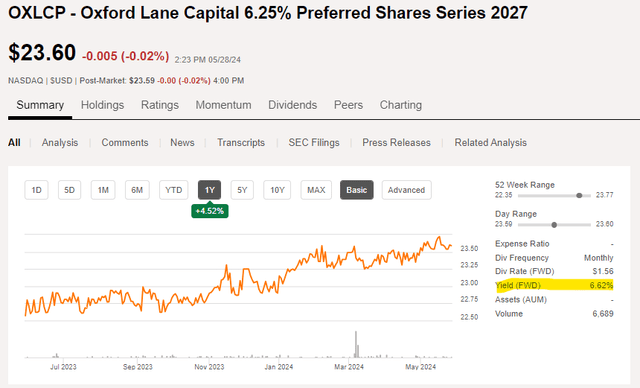

We initially chose OXLCM because of its very short maturity and higher yield than can be obtained in the Treasury market. If the CEF issues no other debt (in the form of bonds or preferred stock), the securities with a shorter duration than the CEF are 2027 preferred stocks and bonds.

While they both have very similar maturity dates, preferred stocks have a higher coupon, and therefore a higher current yield:

OXLCP details (Sa)

However, term preferred stock has a completely different duration and therefore represents an investment with credit spread and interest rate risks. We would have preferred to see one-year CEF securities, but there are none.

The OXLCP will not be redeemed before its maturity date, so expect a duration profile closer to 2.5 years here. Although it is short, it is subject to risk aversion events.

There have been a plethora of new releases in this space, some of which we’ve covered with ‘buy’ ratings:

- “EICC: New CEF Preferred Shares”

- “PMTU: attractive debt from mReit”

However, the term of the new securities is much longer than one year. An investor looking for a “cash-like” instrument would do well to read our articles on Floating Treasury Funds and Short-Term Bond Funds, which are better suited to risk-averse investors:

- “Soviet Union: With Market Turmoil, Floating-Rate Treasury Bonds Pay Off”

- “PULS: Staying in cash has paid off”

It is yet to be seen whether CEF will issue new debt in the form of preferred shares to replace outstanding debt, or will choose to run a lower leverage ratio, but any new security will have a longer-dated profile versus OXLCM. Although there is no “one-for-one” alternative here, the above alternatives are good choices as we have assigned “buy” ratings and determined the risks and rewards associated with each name.

Please also note that the Fund’s last “dividend” date is June 14. Therefore, if you are thinking of selling the name early, it is best to wait until the relevant date to get the last interest payment on the name. .

Conclusion

We own OXLCM, and so far have placed it in the “cash equivalent” pool of our investments. Since there are no very short-term alternatives in the CEF preferred equity space, we may allocate this cash to Treasury funds or short-term bond funds, as described above in the article. We hold the name pending the final interest payment until the maturity date at the end of June when we get the principal back.