Felipe Dupuis/DigitalVision via Getty Images

Zim Integrated Shipping Services Limited (New York Stock Exchange: Zim) The company is seeing a strong rise in profits from its container shipping business, and the company announced that it will pay a dividend for the first quarter as well.

a A rebound in shipping rates combined with a rebound in volume has put ZIM Integrated Shipping Services back on a positive profit trajectory, which could pave the way for many more earnings to come.

I believe ZIM Integrated Shipping is poised for a sustainable recovery that can not only equate to a consistent return on quarterly dividend payments to shareholders, but ZIM also has a re-rating incentive that investors have been waiting for for a long time.

My evaluation history

Improving shipping rate trends led to a “buy” rating for the stock in April, ZIM also expected Integrated Shipping could already announce the resumption of dividend payments soon.

As the shipping company benefited from a good rise in profitability in the first quarter of 2024, amid rising sea freight rates and higher volumes, I believe the risk-reward relationship has improved a lot. Therefore, my new stock rating for ZIM Integrated Shipping stock is “Strong Buy.”

Dividend payback has finally arrived

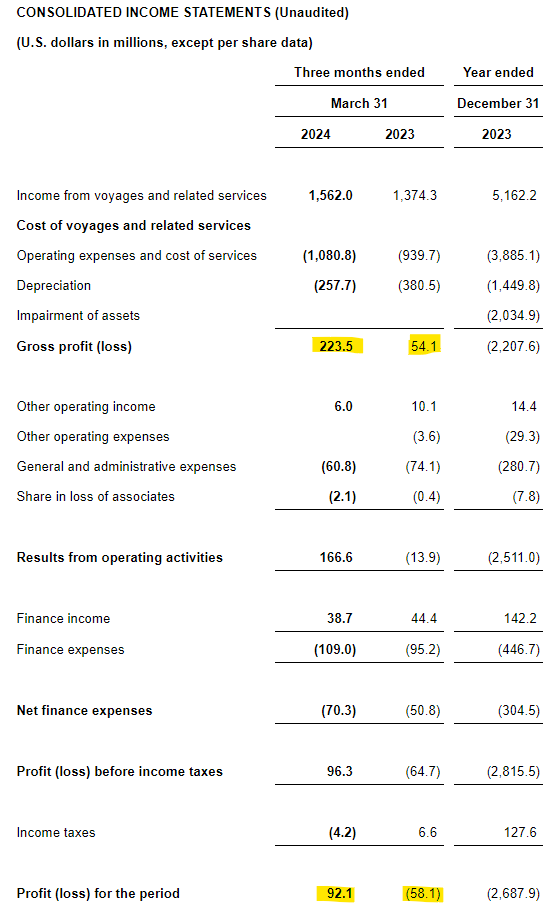

Just a quick look at ZIM Integrated Shipping’s 1Q24 reveals how profound the recent recovery in shipping rates has been impacting: The shipping company generated a gross profit of $223.5 million in 1Q24 on total sales of $1.56 billion, reflecting A 4-fold increase compared to last year. the last period.

The company also finally returned to positive net profits, which rose to $92.1 million. In the year-ago period, ZIM Integrated Shipping lost money, as it did in the fourth quarter.

Consolidated income statements (Zim Integrated Shipping Services)

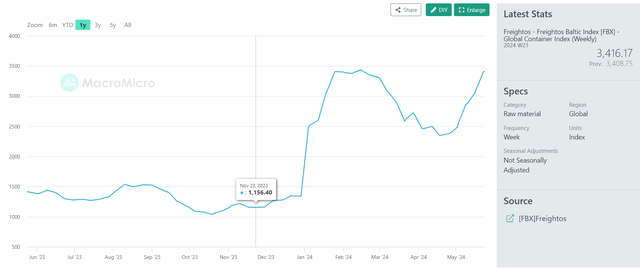

The Freightos Baltic Index, an index for container pricing, saw a sharp increase in ocean freight rates in 2024. The Freightos Baltic Index shows that the sea freight price for a 40′ container began to increase significantly at the beginning of the year, with rates topping out at $3,440 in mid-February .

After that, prices consolidated for a short period of time, but are now at $3,416 per 40-foot container, potentially hitting new highs as well. The strong rise in freight rates is a result of increased demand for freight.

Fritos Baltic Index (macromicro)

My positive outlook for ZIM Integrated Shipping relates to two considerations:

First, the most encouraging aspect of ZIM Integrated Shipping’s Q1 earnings was not the recovery in ocean freight rates, which was well understood before the company reported Q1 2024 earnings. I think the most encouraging piece of information is that the company has enjoyed a strong recovery in container volume in the first quarter.

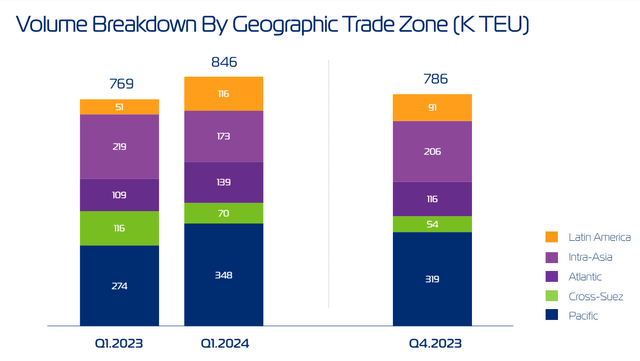

ZIM Integrated Shipping moved 846,000 TEU (twenty-foot equivalent units) in the first quarter, reflecting a 10% jump compared to the same period last year. The jump in volume combined with increases in container shipping rates has led to a very significant reversal in ZIM Integrated Shipping’s fortunes in the first quarter of 2024, in terms of net profits.

Volume distribution by geographical trade area (Zim Integrated Shipping Services)

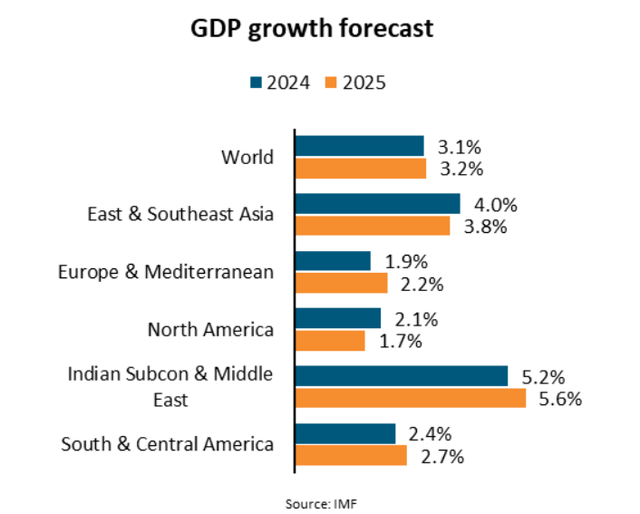

Second, the prospects for a continued recovery in shipping container volumes as well as favorable ocean freight pricing trends are strong, in my view, primarily due to IMF forecasts of strong global economic growth in 2024.

With ZIM Integrated Shipping also revising its earnings forecast for 2024, mainly due to rising demand reasons, I believe shipping rates as well as cargo volumes are poised to see sustained growth tailwinds this year.

GDP growth forecasts (International Monetary Fund)

Due to volume growth and rising freight rates, ZIM Integrated Shipping has revised its adjusted EBIT forecast upward as well: The shipping company now expects to earn adjusted EBIT of $0 million to $400 million, compared to guidance The previous amount is (300) million dollars to 300 US dollars. million.

Earnings stagnate in the rearview mirror

ZIM Integrated Shipping’s business activities in the first quarter resulted in net profits of $92 million.

Since the company had previously established its dividend policy (which stipulated that the company would pay out 30% of its profits on a quarterly basis if its net profits were positive), ZIM Integrated Shipping announced that it would pay $28 million, $0.23. Dividends per share in the first quarter of 2024.

The dividend will be paid to shareholders on June 11, 2024 with a record date of June 4, 2024. Based on a dividend of $0.23 per share, ZIM is scheduled to receive a total yield of 1% (pre-tax).

While this return may not be large enough to lure passive income investors back into buying the stock, I believe it is only the first return and many more are set to follow, especially if ZIM Integrated Shipping succeeds in working its way back to consistent profitability. In a rising freight market.

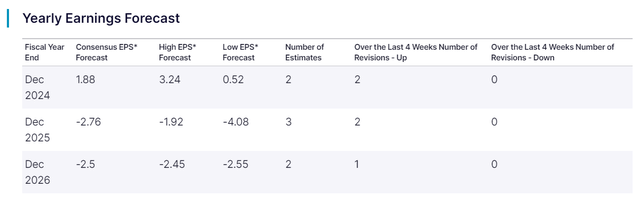

More importantly, with freight demand rising again, investors are seeing a profound move in terms of earnings estimates. In fact, the market is already modeling positive earnings of $1.88 per share, on a consensus basis, for 2024.

This means that ZIM Integrated Shipping shares are currently selling for a very modest 11 times earnings (based on current year’s estimated earnings) which is a steal, especially when taking into account ZIM’s dividend potential. In 2022, for example, the company paid a whopping total dividend of $27.55.

I’m not saying we will immediately return to this level of earnings, but what I am saying is that we may be at the beginning of a new charging cycle that could lead to a steady stream of earnings throughout the year.

Annual profit forecasts (NASDAQ)

I believe that ZIM Integrated Shipping, with its improved profit outlook and return to consistent profitability, has great re-rating potential. Earning $3 per share in 2024 is a distinct possibility (and perhaps a low estimate) as ZIM earned $0.75 per share on a diluted basis in the first quarter of 2024. Three dollars per share and an 11x multiple leads us to an implied intrinsic value of $33 (assuming no Multiple expansion in the growing shipping sector).

With the stock selling for around $22 now, a 50% upside is quite realistic, in my view. This return does not even include the payment of dividends.

Why might my investment thesis be misleading?

Higher freight rates are clearly a big boon for cash-strapped shipping companies that fell into a deep earnings slump last year. Therefore, a deterioration in the pricing trend for shipping containers is likely to have a severe negative impact on ZIM Integrated Shipping’s profit outlook.

Merchandise volume contraction may also be an early indicator that the sector is facing some more serious headwinds.

deductive

ZIM Integrated Shipping’s earnings stagnation is in the rearview mirror, in my view, and the clearest indication that this is the case lies in the fact that the shipping company has radically revised its 2024 EBIT forecast.

The appearance of net profit in the company’s data for the first quarter of 2024 is also positive, as is the increase in container volumes and the context of rising sea freight rates.

The overall outlook is favorable, and the market is now planning to return to full-year profitability, which is a dramatic change from last year.

Yes, profits are back, and they’re great, but I’m even more excited about ZIM’s ability to increase its valuation in a growing freight market.