Nastasek

Glacos Company Overview

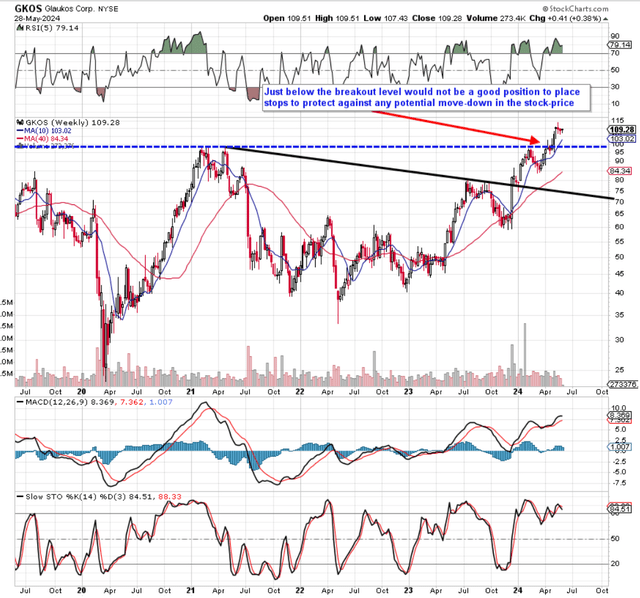

We wrote about it Glaucus institution (New York Stock Exchange: Geckos) in January of this year when we maintained our ‘hold’ rating on the glaucoma treatment company. The reasons for our cautious stance at that time were the overvaluation of the stock and its sustainability Print negative profitability. As we see below, two important technical phenomena have occurred over the past 20 weeks.

First, stocks broke above the downtrend line of a multi-year stock cycle. Second, in just the last sessions of this month, shares have also risen above their 2021 highs. This means the stock’s value has risen 34%+ since our commentary in January of this year.

Suffice it to say that each of these technical results could be a precursor to a new bull market in Glaucus from this point on. However, due to the fact that breakout in stocks of all time There has been a recent spike, and we still need more clarification on whether this hack is real or not.

Therefore, for additional reasons discussed below, we believe the correct course of action here is for long-term investors to continue to “hold” the stock but not overweight their existing positions. Furthermore, if a false breakout actually appears on the technical chart, the prime location to place a stop loss will be at the breakout level shown below. Furthermore, if the stock indeed continues to gain strength, long-term investors can continue to follow the stock higher with higher stop-loss positions over time. This strategy allows the investor to benefit from upside gains while simultaneously reducing downside risk if the position moves in the opposite direction.

Intermediate technical GKOS (stockcharts.com)

Double-digit sales growth is pushing GKOS stock north

In the company’s most recent first-quarter earnings report (announced May 1), management increased full-year guidance based on rolling 20% year-over-year growth in both its U.S. and international glaucoma businesses. Total sales for the quarter ($85.6 million) grew 16% less than the same period 12 months ago, due to the Corneal Health franchise (4% growth) reporting slower growth than larger franchises. What pushed the stock price forward in May was an upgrade from Jefferies to a “buy” rating. Truist Securities reiterated its bullish stance this week.

The lion’s share of CEO commentary on the earnings call focused on the U.S. glaucoma franchise, which accounted for nearly half of total consolidated net sales in the quarter. The company’s iStent portfolio pushed sales forward in the first quarter but updated news about the launch of the iDose TR was actually what piqued investors’ interest on the recent earnings call. The early signs from a feedback standpoint look bright in terms of surgeons who have benefited from early access and completed treatment. Furthermore, encouraging updates were provided regarding payment and associated market access.

It remains to be seen whether iDose TR will have the potential to revolutionize the field of glaucoma treatment, but management is certainly confident. We have consistently seen in this industry that strong market access to products is vital to ensuring that sales can grow and multiply over time. Perhaps the biggest reveal is CMS’s new permanent J token, which (once it becomes effective from July) should directly lead to improved market access and payment methods for iDose TR.

The CEO announced additional promising developments in a recent Q1 earnings call regarding market access and reimbursement for the iDose TR, as we learn below:

CMS has signed off on CPT codes designed to be used to cover the procedural component of iDose TR 0660T and 0661T for Ambulatory Payment Classification or APC 5492 effective April 1, 2024. This translates to a national average facility fee of approximately $3,900 in the HOPD setting and more than $2,000 in the ASC setting. We have participated in several initial educational meetings with Max as part of our efforts to secure coverage and payment of professional fees throughout 2024. We have successfully entered the Medicaid Drug Rebate Program, or MDRP. Finally, we have successfully begun early initiatives to secure coverage for commercial and Medicare Advantage plans, efforts that we plan to accelerate in the second half of 2024 after Code J goes into effect.

Still, strong sales growth is not leading to improved profitability trends

However, despite the bullish fundamentals discussed above, Glacos continues to report negative earnings and the share count continues to rise. Although growth stocks often indicate negative earnings, the magnitude of a stock’s growth path over time is always in line with the trend of a company’s earnings.

To this point, Glaukos has reported $40.5 million in GAAP earnings in the first quarter, the highest net profit number (worst earnings) since the second quarter of fiscal 2022. Suffice it to say, despite the company’s bottom line growth, This growth is still not “falling” to the minimum level, which raises concern from the shareholders’ point of view.

Continued negative profitability meant that over $13 million worth of additional shares were issued in the first quarter, however, shareholders’ equity continued to decline to $450.7 million during the quarter. These are not shareholder-friendly trends, especially if these trends continue over time.

What growth investors can sometimes overlook is the fact that companies create value by investing cash today to generate returns tomorrow. This means that sales growth is only one part of the equation. Another crucial step is the ability to achieve a healthy return on capital (ROC). As noted above, however, with regards to Glaukos’s faltering profitability, the company’s ROC over the past 12 months comes in at -8.76% which is a far cry from Glaukos’ 5-year average of -5.94% (in relation to the trend).

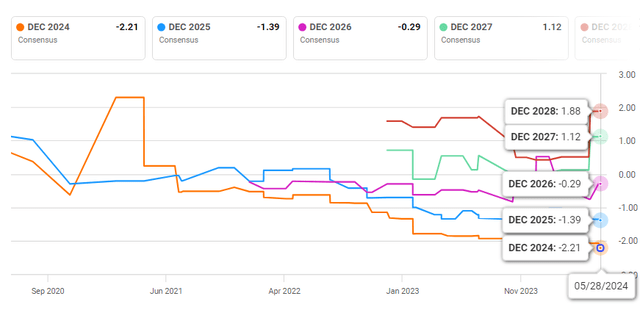

Therefore, although earnings are expected to break even this year ($2.21 EPS), followed by sustained growth in the following years, investors should remember that all of Glaukos’ projected forward-looking growth has been fully absorbed by The stock price at this point. . This essentially means that any further deterioration in EPS revisions will not be adequate for sustainable share price gains.

Glaukos EPS Consensus Reviews (Searching for Alpha)

Conclusion

In summary, despite Glaukos’ continued strong sales growth and accompanying upside guidance in the first quarter, we are reiterating our “Hold” rating on the stock for now. First, it has been very little time since stocks hit all-time highs, so patience is needed to ensure that the newly formed support will actually hold up if tested. Second, the extended valuation, in relation to EPS revisions and the weak ROC trend, are additional reasons why we recommend adopting a trailing stop loss strategy here. We look forward to continued coverage.