Evening pictures

introduction

I have good news and bad news.

The bad news is that a lot of cyclical companies are currently showing stock price weakness, as the market seems to realize that cyclical growth is unlikely to rebound soon.

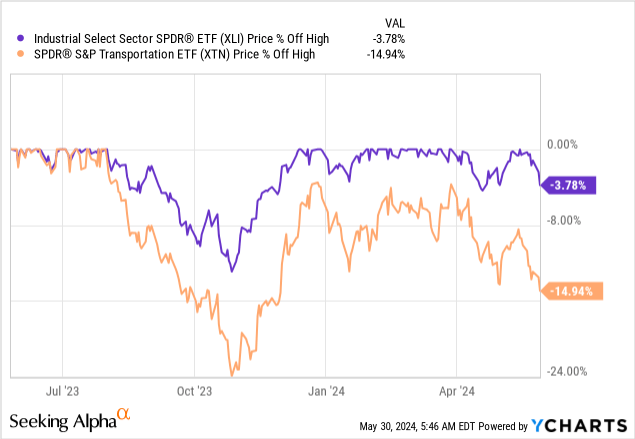

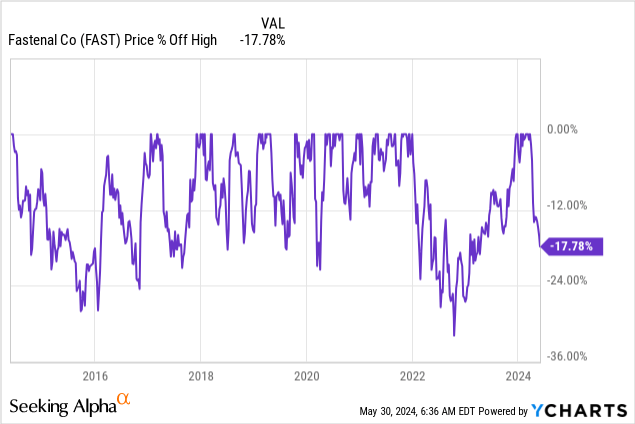

Although we are far from a sharp sell-off, industrial stocks have weakened and are now trading roughly 4% below their 52-week highs. For example, shares of Cyclical Transport (XTN) sold off by 15%.

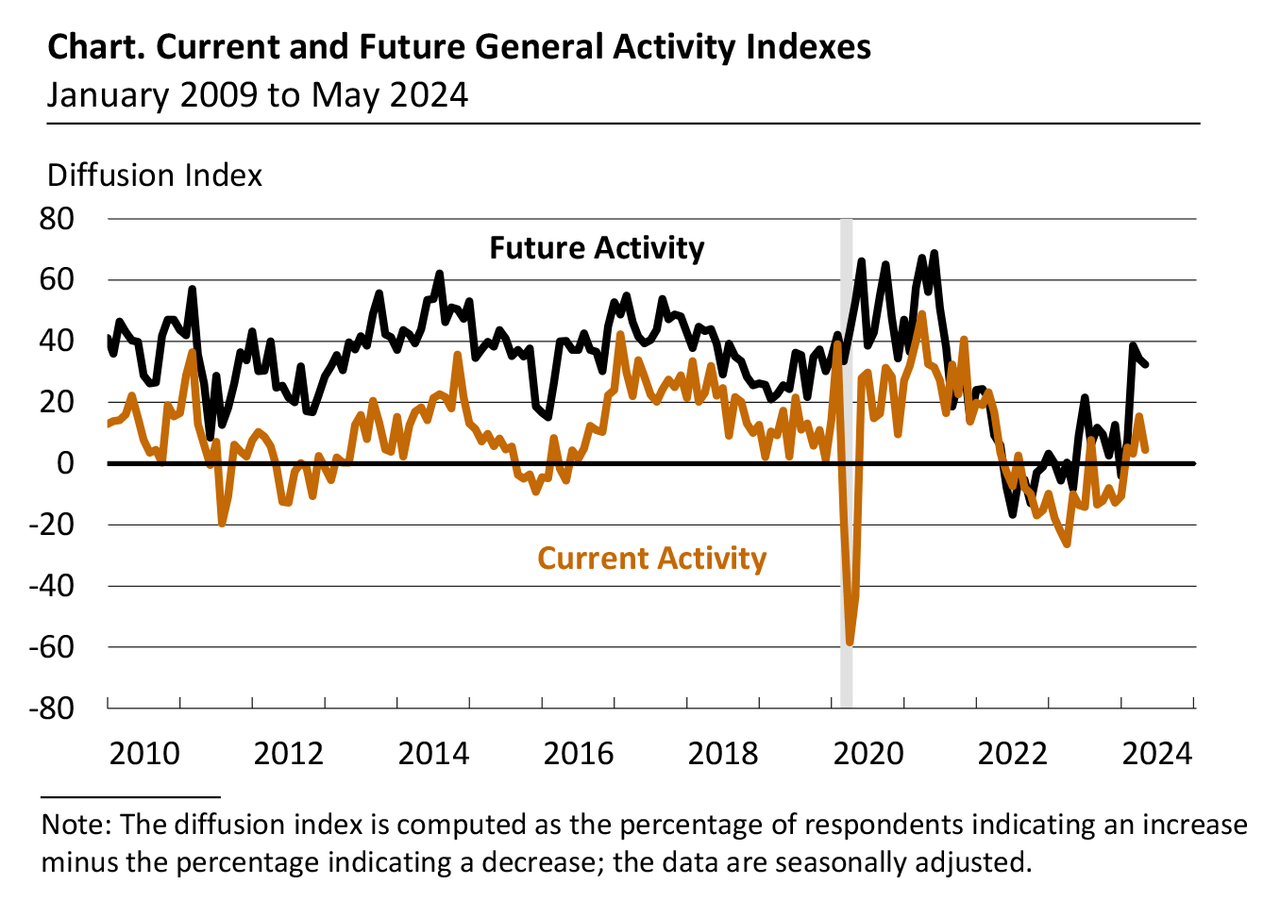

The reasons are due to flat inflation, geopolitical uncertainties, the Fed making clear that it needs more evidence of inflation falling significantly before normalizing interest rates, and the fact that cyclical growth indicators such as the Philadelphia Fed Manufacturing Index (current conditions) continue to show sluggish growth. Unable to start a meaningful uptrend.

Federal Reserve Bank of Philadelphia

The good news is that this comes with opportunities, as A A few very attractive cyclical stocks are currently struggling, bringing their valuations back to reasonably attractive levels.

One of these companies is Fastenal Company (Nasdaq: Fast)a company that began its coverage with A Catch Classification on March 26 in an article entitled “Fastenal: A new member of the aristocratic Dividend Club, you probably didn’t know him.”

Since then, shares have fallen about 16%, even though the market was trading near all-time highs.

In this article, I’ll revisit my thesis, explain what makes it so special, and how recent events have affected the risk/reward for dividend (growth) investors like me.

So lets get to it!

What makes Fastenal so special?

Before we dive into the financial numbers, I want to quickly reiterate why the FAST Index is on my radar.

Fastenal is an industrial company with a market cap of $37 billion.

This Minnesota-based company is a great industrial distributor that sells to a wide range of customers, including heavy industry, transportation, non-residential construction, and many more.

Fixed

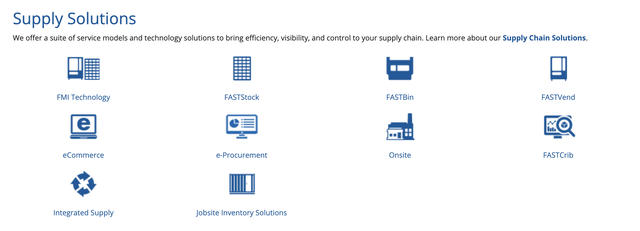

The company has found a way to take industrial distribution to the next level by operating a network of on-site locations and branches powered by e-commerce to deliver industrial supplies when and where they are needed.

Fixed

Although I usually stress that I prefer companies with a wide moat, I also like companies that have found a way to penetrate markets with low barriers to entry.

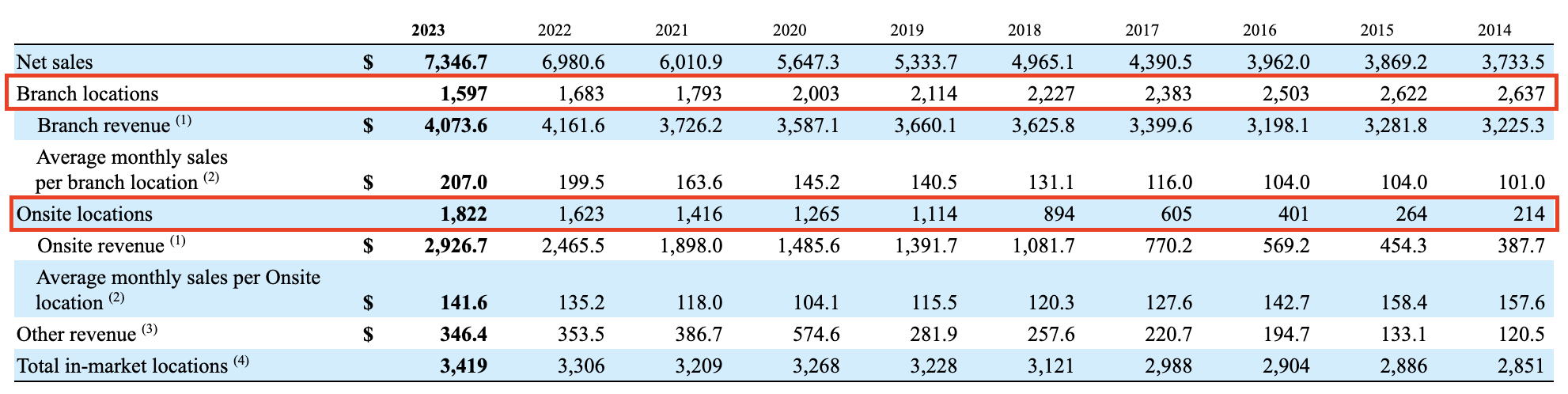

Fastenal has found a great way to do this, shrinking its branch locations from 2,637 in 2014 to less than 1,600 this year.

At the same time, it boosted its on-site positions from 214 to more than 1,800 during the period, bringing supplies closer to customers.

Fixed

On-site locations offer services such as daily replenishment of supplies, backed by advanced data to improve the process.

By including technologies and systems such as Fastenal Managed Inventory (“FMI”), FASTStock/FASTBin, and FASTVend, it has created a vending machine-like network that gets customers vital supplies whenever they need them.

Fixed

Nearly 66% of the company’s installed base consists of locker-based solutions similar to the vending machines where we buy cans of Coke and bags of potato chips.

Fixed

As I wrote in my previous article, the company finished last year with an installed base of 111,800 FASTVend models with an estimated growth potential of 1.7 million vending machines.

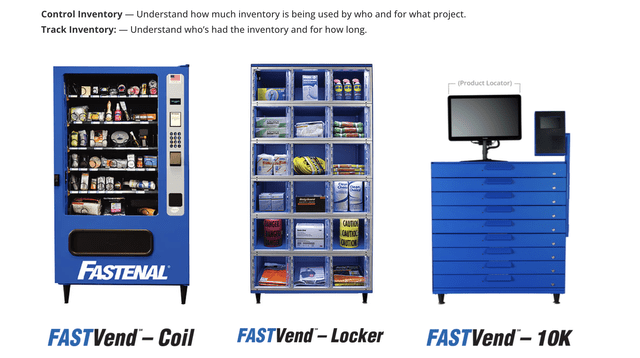

This has allowed the company to return 245% over the past 10 years, surpassing the S&P 500’s return of 228% despite the recent share price sell-off.

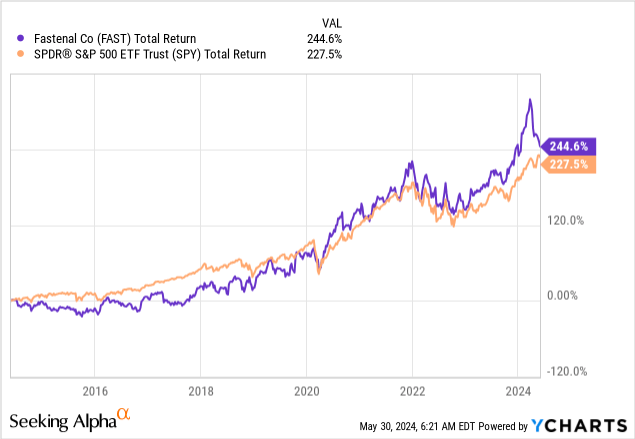

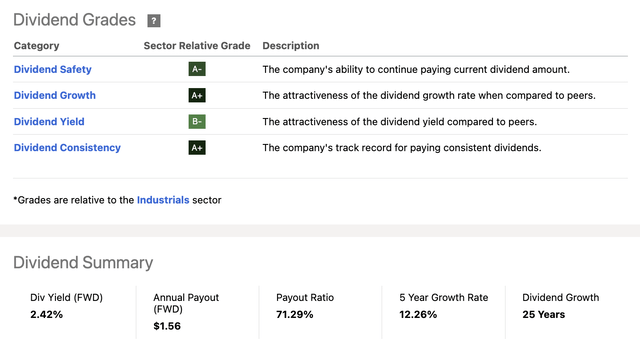

It also became a dividend aristocrat when it raised its dividend 2.6% on January 17, bringing the tally to 25 consecutive annual dividend increases.

The company currently yields 2.4%.

Using Seeking Alpha’s earnings scorecard, we see very positive results, supported by a payout ratio of 71% and a five-year CAGR of 12.3%.

Seeking alpha

So why are stocks being sold?

A closer look at the risk/reward of Fastenal

Selling supplies to manufacturers is highly cyclical, which explains why FAST investors experience frequent share price sell-offs.

As we can see below, over the past 10 years, investors have gone through countless corrections similar to the current one.

During this period there were two types of outliers:

- The industrial recession of 2015/16 caused investors to temporarily lose a quarter of their investments.

- The pandemic briefly caused stocks to sell off more than 30%.

Needless to say, none of these corrections were “random.”

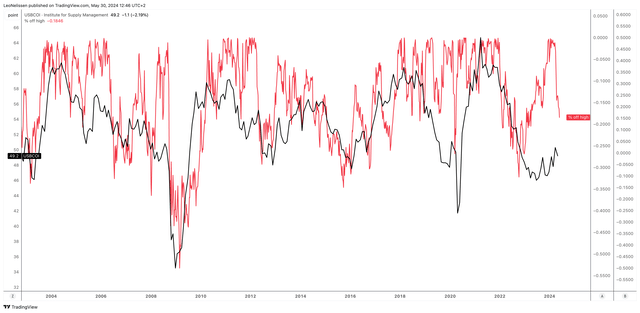

Using the chart below, we see a strong correlation between the distance (in percentage terms) that FAST shares are trading below their all-time highs and the ISM Manufacturing Index, which is one of my favorite economic indicators.

TradingView (FAST, ISM indicator)

As I mentioned in the introduction, I believe investors are currently adjusting their expectations as the cyclical growth recovery stalls.

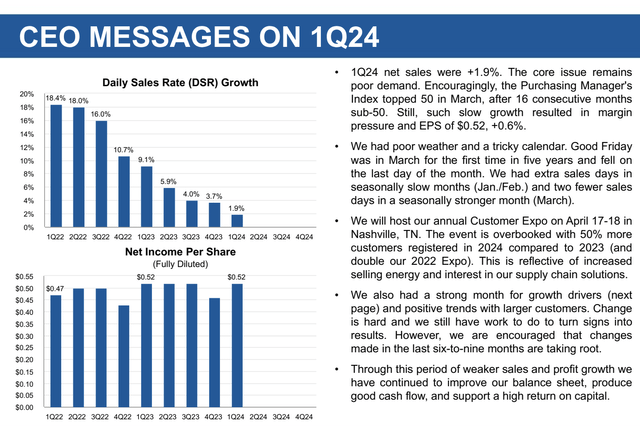

Hence, we see these challenges in the company’s most recent earnings as well, when the company used the earnings call to explain that the first quarter came with significant challenges, resulting in growth of 1.9%, below the expected growth rate of 4%.

Fixed

One issue was headwinds from lower sales days, as the CEO explained in the overview above.

However, that was an expected headwind, which doesn’t explain why sales were weak.

The main challenge was weak underlying demand, with industrial production falling slightly, which put pressure on sectors such as machinery production.

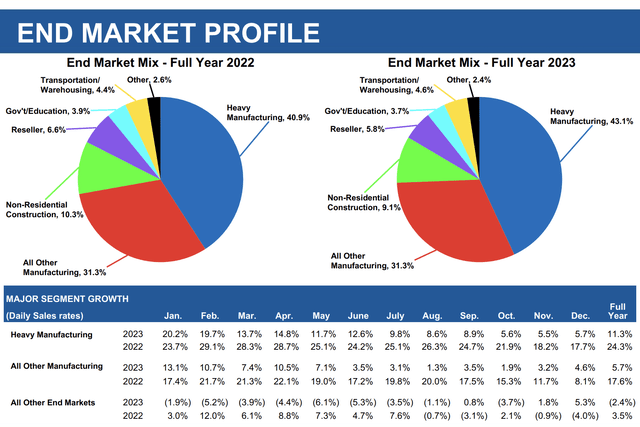

To add some color here, while overall manufacturing saw a modest growth rate of 2.6%, the fasteners product line saw a 4.4% decline, which was largely due to weak industrial production and pricing headwinds.

Furthermore, the non-residential construction and resale sectors continued to contract, albeit at a slower rate. Meanwhile, FMI’s sales remained healthy, contributing to safety products growth of 8.3%.

In addition, regional business activity was steady but weak.

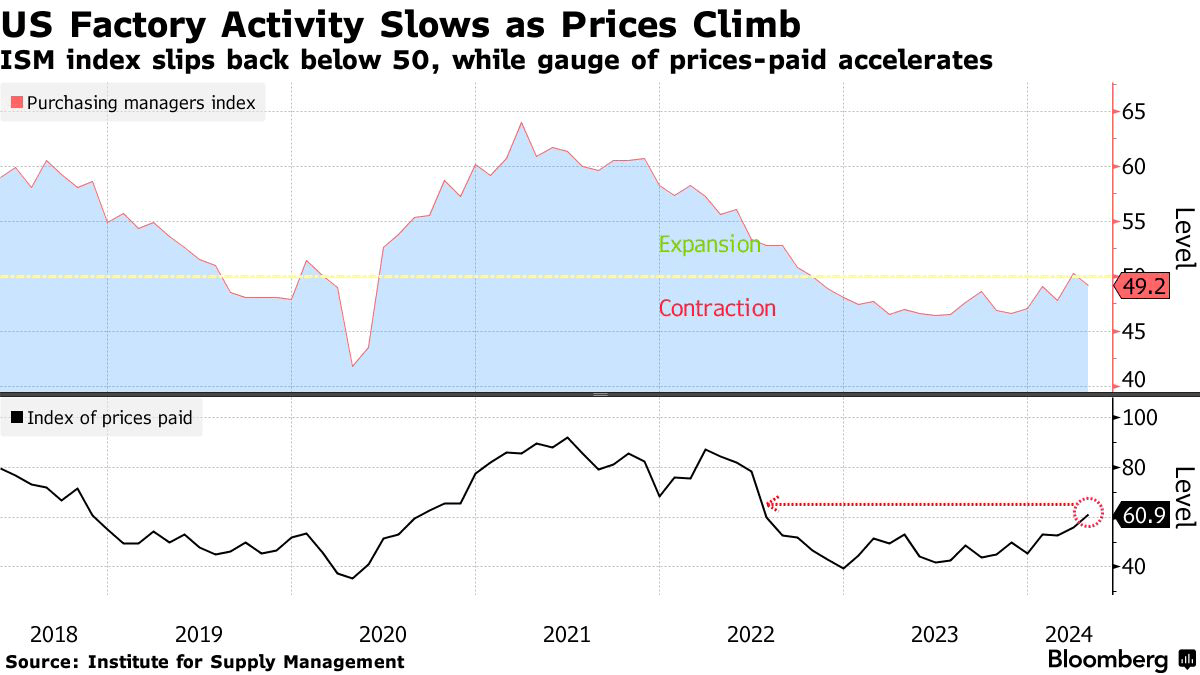

The good news is that the company highlighted that the ISM Manufacturing Index is back above 50, indicating growth.

Fastenal is one of the very few companies that actually comments on this indicator regularly.

The bad news is that since then, the index has fallen below 50 again.

Bloomberg

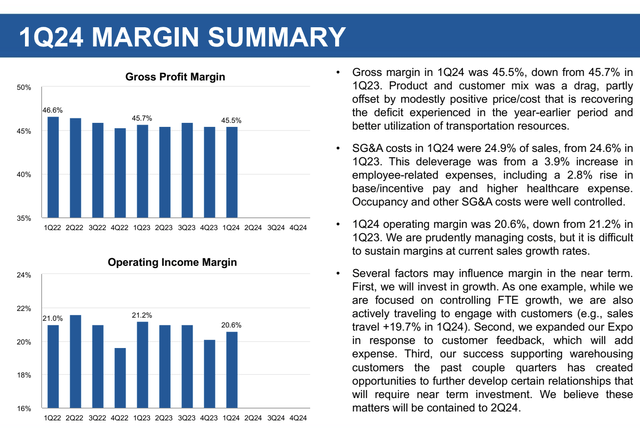

In terms of margins, we are also seeing some headwinds, primarily due to an unfavorable decline in product and customer mix, which caused operating margins to decline by 60 basis points to 20.6%, with gross margins to decline by 20 basis points to 45.5%. .

Fixed

None of these developments indicate unusual weakness.

Having said all this, while cyclical headwinds persist, the company continues to focus on the things that can actually impact it, which includes expanding on-site locations.

The number of on-site locations increased 12%, although sales through on-site locations increased in the low single digits due to slower demand growth.

In addition, the company’s e-commerce platform approached 60% of total sales. Fastenal aims to raise this figure to 66% by the end of this year, with 85% being the ultimate goal.

evaluation

Given the economic challenges, analysts expect FAST to achieve just 4% growth in earnings per share this year. This would be the worst performance since the 2% decline during the 2016 manufacturing recession.

The good news is that after 2024, analysts expect EPS growth to rebound to 10% and 8% in 2025 and 2026, respectively.

Quick charts

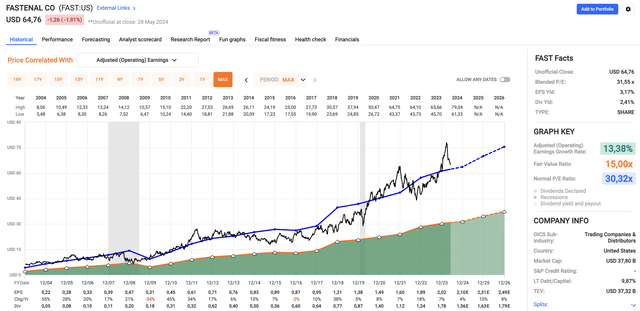

Furthermore, the company now trades at a blended P/E ratio of 31.7 times, which is slightly above its long-term average of 30.3 times.

This means the target price is $75.50, which is 17% higher than the current price.

Due to economic developments, I will change my rating to He buys If we see 10% more downside.

At this point, I’m interested in making FAST part of my portfolio, because I believe this advanced distribution business model has a very bright future!

Away

Cyclical stocks face challenges, as inflation and geopolitical uncertainties keep growth weak.

Fastenal, which has become one of the leaders in the industrial sector, saw its shares fall 16% from their recent highs.

However, despite the economic downturn, Fastenal’s unique distribution model, extensive on-site locations, and strong e-commerce platform make it a compelling investment.

Furthermore, the company’s history of consistent earnings growth and its strategic focus on efficiency and customer service through on-site services support its long-term potential.

Although current market conditions are difficult, I see a huge opportunity if the stock drops another 10%.