Topicus Stock: Poised to Benefit from a Momentum Rebound in the Technology Sector (Upgrade) (TOI:CA)

Khanshit Khirisuchalwal

Early this month Tobicus (TSXV:TOI:CA) released its results for the first quarter of 2024. This analysis will examine the latest developments at Topicus and the company’s financial position. I last covered Topicus last November year when I discussed the 3Q23 financial numbers. I gave the stock a “hold” rating. TOI has risen about 25% since then.

Topicus is a leading provider of Vertical Market Software (VMS) solutions. The company is largely focused on acquiring VMS businesses with growth potential. These accretive M&As (although some may end up being dilutive) have helped Topicus grow its top line and generate cash flow since its spinoff from Constellation Software (CSU:CA). As a serial acquirer, looking at organic growth in sales is just as important as overall growth in sales, because total sales are typically affected by the timing of M&A deals.

The company generates its revenue primarily from software licensing fees, professional services fees, hardware sales, and other recurring fees. Given this revenue structure, retaining existing customers is a priority for Topicus. A recurring revenue stream from existing customers provides more predictable cash flow and operational stability, considering the company’s serial mergers and acquisitions. Topicus’s acquisitions are primarily aimed at expanding the vertical’s service offerings and thus increasing its market share and revenues. Introducing a new vertical software solution takes a lot of work. It takes experience and deep domain knowledge to build mission-critical solutions tailored to a specific industry. Acquisitions make VMS expansion faster. Growth comes at a high cost for vertical software companies like Topicus. That’s why in my analysis of vertical software companies, I emphasize organic growth and recurring revenue from existing customers.

Looking at Q1 numbers, I’d consider Topicus’ resilience or lag in organic revenue growth, and how much it strengthens (or weakens) the bottom line based on expenses and margins, operating cash flow and free cash flow available to shareholders.

A look at Topicus Q1 CY24

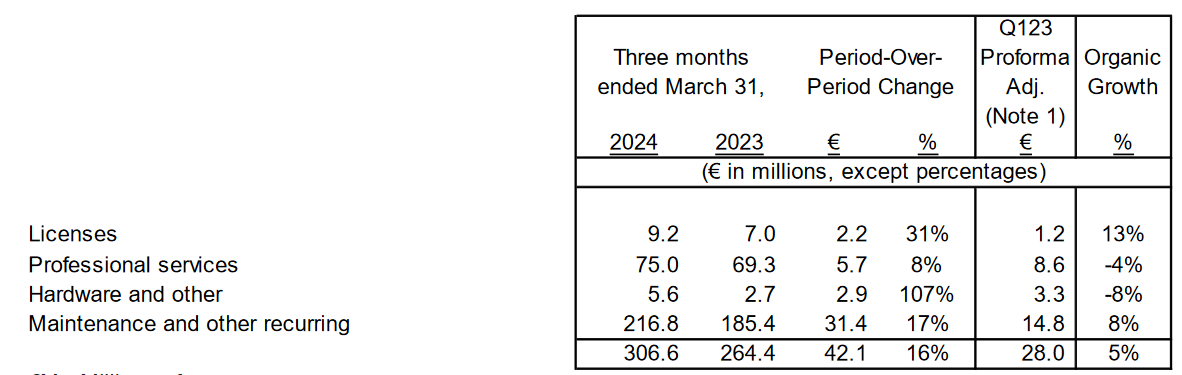

For the top line, sales were up 16% year over year. Most of the growth is due to acquisitions. The company recorded sales of €306.6 million. Sequentially, this is a slight decline from Q4 sales of €309.7 million. Q1 organic revenue growth was 5%, which is also a 200 basis point decline from Q4 organic revenue growth of 7%. Since 3Q23, organic growth has declined by at least 300 basis points.

Revenue generation (Topicus MD&A)

The overall breakdown of revenue composition shows that Topicus has maintained the trend of getting the lion’s share of its revenue from recurring services. Maintenance and recurring revenues provide a stable and predictable outlook for the company’s sales and business sustainability. Maintenance and recurring revenue increased 17% year over year and saw a sequential increase of 6%. While the top line appears to have seen some contraction in sequential revenue, a closer look shows that the larger composition of the top line (maintenance and recurring) has seen growth. Topicus’ sequential revenue declines were impacted by lower sales from licensing and professional services. These license sales are typically one-time payments for new product registrations and can experience some seasonality. Therefore, I maintain that Topicus’s top line has remained healthy.

As a company that operates multiple VMS businesses, Topicus incurs high expenses and employee expenses take a large share of Topicus’ expenses. For the first quarter, operating expenses increased 15% year-over-year and 3% sequentially, largely driven by an increase in employee expenses. Topicus’ acquisitions in the first quarter added more employees to the company. Hence, higher staff expenses.

Quarterly results (Topicus MD&A)

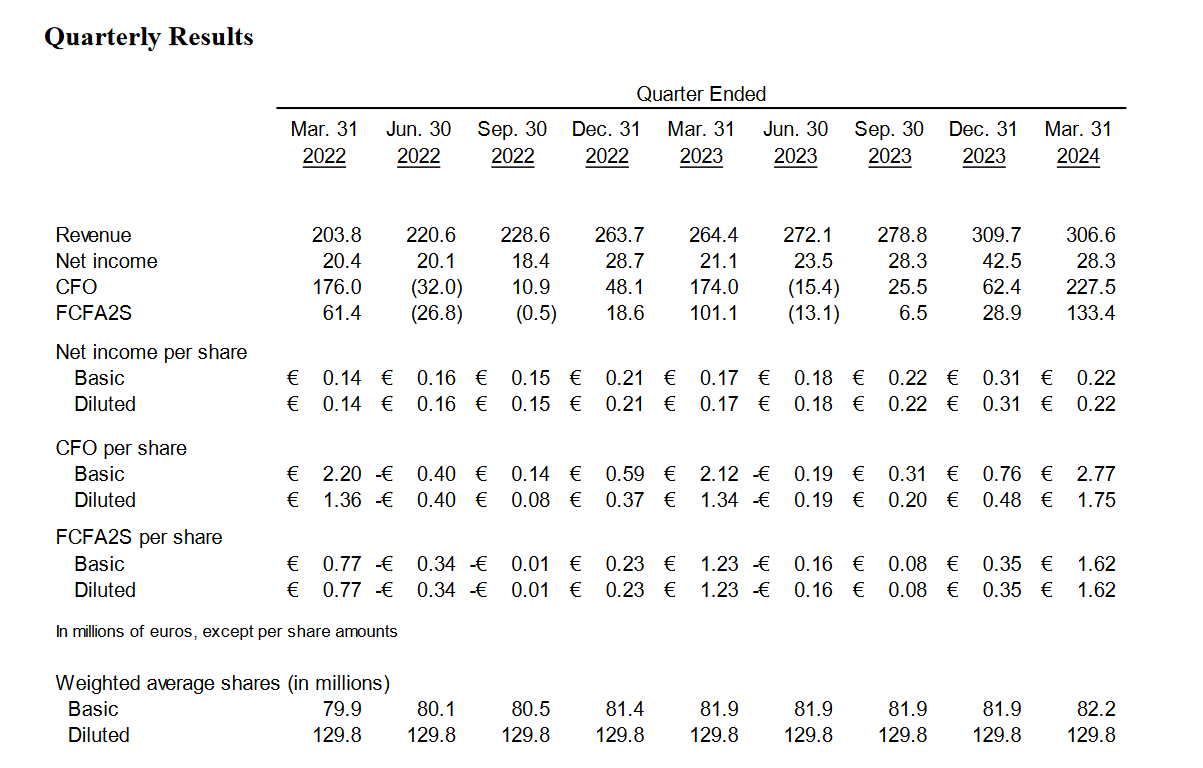

The increase in operating expenses impacted the sequential decline in Topicus’ first-quarter net earnings. While net income rose by about 34% year-on-year, net income saw a sequential decline of 33%. EPS for the first quarter amounted to €0.22. Cash from operations (CFO) per share was €2.77 or €1.75, on a basic and diluted basis, respectively. Most Topicus companies bill customers for annual software maintenance fees in the first quarter of each year, resulting in a disproportionate amount of cash being received in the first quarter compared to the remaining three quarters. This seasonality in cash receipts affects the CFO per share. Regardless of seasonality, Topicus’ cash generation remains strong. How this cash generation meets M&A and dividend payment expenses is one aspect for investors to keep an eye on.

Net change in cash flows (Topicus MD&A)

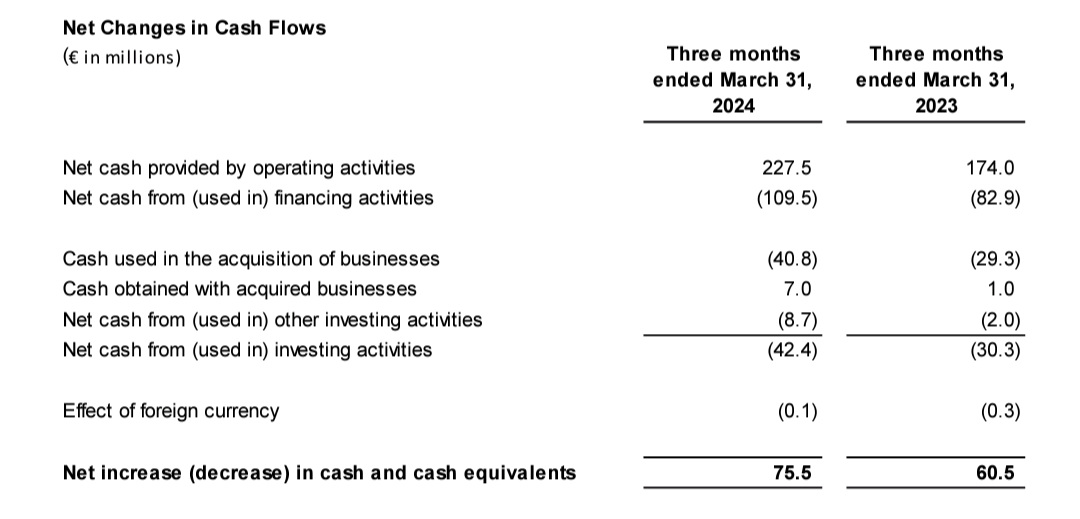

Topicus deployed capital for acquisitions and dividend payments in the first quarter. Net distributed capital exceeded CFO for the first quarter. Despite this, Topicus continued to increase its cash position by €75.5 million by obtaining financing from other sources, increasing the debt level by €102.5 million, bringing total debt to $328.2 million. Topicus has not yet diluted shareholders but has opted for debt financing instead.

minimum

While Topicus may not have met consensus estimates in the first quarter, the company still demonstrated operational resilience, participated in mergers and acquisitions, and generated impressive free cash flow. Topicus’ recurring revenue (which is a significant portion of a vertical software provider’s revenue) as a percentage of total revenue remains strong. Topicus is a stable company with a fairly predictable top line. Technology stocks are starting to regain lost momentum, and consumer and discretionary IT spending is seeing some recovery.

The Company experiences some seasonality in its operations due to mergers and acquisitions and the timing of cash receipts. Analyzing this company requires looking under the hood – overall revenue distribution, expense analysis, and cash flow dynamics.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.