sturti/E+ via Getty Images

introduction

Tren Techniques (New York Stock Exchange: TT) is a leader in the global heating, ventilation and air conditioning (HVAC) systems market. Over the past year, the company’s shares have nearly doubled, driven by accelerating demand as well as margin improvement. However, despite the bullish outlook As for business, I think stocks have gotten ahead of themselves, which is why I’ll avoid stocks. In this article, I will discuss the merits of Trane Technologies as a business, its competitive advantages, and its financial aspects. I will also discuss my thoughts on the company’s long-term outlook as well as valuation, and why I find it unattractive today.

Company overview

Trane Technologies is in the heating, ventilation and air conditioning (HVAC) business. Once known as Ingersoll Rand, the company spun off its industrial business in the third quarter of 2020 and retained its heating, ventilation and air conditioning (HVAC) business.

However, Trane Technologies is not like that Only one freelancer; They operate under many well-known and distinguished brands in the industry such as Trane and Thermo King, among many others. You see it a favour For its innovative energy efficient HVAC solutions for residential, commercial and industrial customers, while Thermo King focuses more on temperature control. This includes temperature control systems for things such as perishable goods so they can be stored and transported safely.

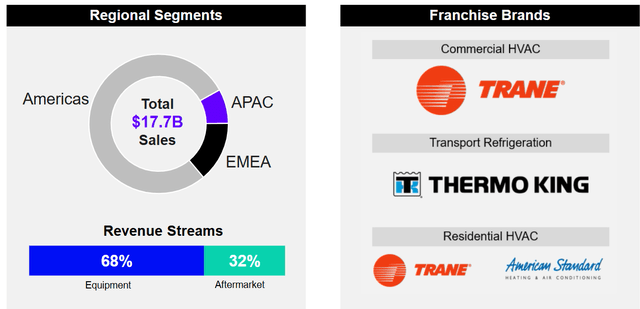

As a global company, its products and services can be found in many countries. About 78% of revenue comes from North America, 14% comes from EMEA, and 8% comes from Asia Pacific.

background

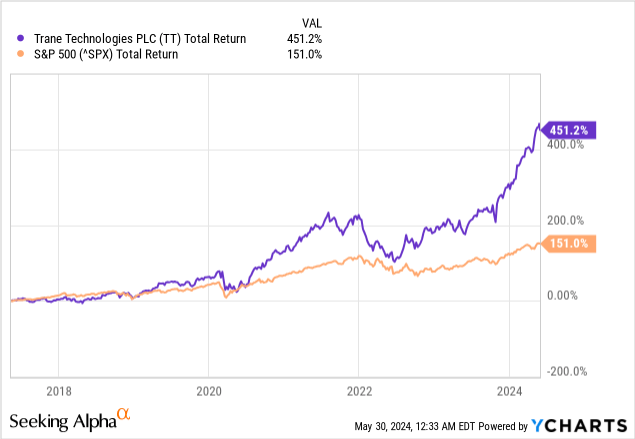

Trane Technologies has a strong history of outperformance. Over the past 10 years, the company has generated a total return of 451.2%, compared to the S&P 500’s return of just 151%. Calculating the total return annually over the past 10 years results in a compound annual growth rate of 18.6%, which equates to doubling your money approximately every 4.1 years.

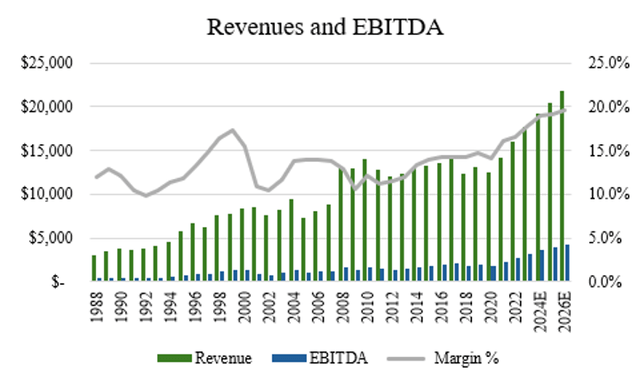

Trane Technologies’ financial performance hasn’t been nearly as impressive. In the past decade, the company’s revenue and EBITDA have grown by 3.7% and 7.8%, respectively, a far cry from the stock’s 18.6% CAGR (Source: S&P Capital IQ). In the past five years, the company’s revenue has grown at a CAGR of 7.4% with EBITDA growing at a CAGR of 12.2%. So, with modest returns compared to the impressive share price performance, a significant portion of the company’s share price return came from multiple expansions.

Author, based on data from S&P Capital IQ

One way Trane Technologies differentiates itself is by focusing on sustainable technologies that align with global climate initiative trends. Over the past several years, there has been a significant push for companies to adopt more sustainable and environmentally friendly products, services and technologies into their businesses to reduce their carbon footprint.

Trane Technologies meets this demand by providing those high-performance HVAC products by meeting those needs and going above and beyond to stay on trend with a commitment to sustainability. In its 2023 ESG report, the company announced that it reduced 157 million metric tons of carbon and reduced operational emissions (Scope 1 and 2) by 44%, ahead of schedule.

On the surface, some may wonder if this is an ESG play or if there is any money and sense behind it, but for customers looking for better solutions that include data analytics, reduce air quality, reduce energy consumption, and help them meet their emissions targets, This has an impact in terms of its competitive advantage, which allows it to compete well in the market.

A large portion of Trane’s business includes after-sales services at about 32% of revenue. This is an important part of the business because it has things like maintenance, repairs, and upgrades needed for customers to be able to use their HVAC systems effectively without interruption. For Trane, this is an attractive part of the business because it creates stable, recurring, predictable revenue and reduces fluctuations in earnings.

Investor presentation

Finance and forecasts

In Trane Technologies’ latest quarterly results for Q1 2024, the company reported strong growth across the board. Organic revenue increased 14% year over year and operating margins increased 230 basis points. Adjusted earnings per share also rose significantly, with an increase of 38%.

Overall, the company looks well positioned to continue growing at a decent rate. Bookings exceeded $5 billion (up 17% organically), so the company’s growth rate has accelerated somewhat, given the operating levers and investments the company has made in R&D and capital expenditures. The first quarter ended with a backlog of $7.7 billion, up 10% from the $6.9 billion at the end of 2023. Wall Street expects 8.9% growth in 2024 (vs. 2023) and 6.4% growth in revenue for 2025, which is slightly more than CAGR of 5.5%. The expected rate of the global HVAC market until 2030 (Source: Bloomberg).

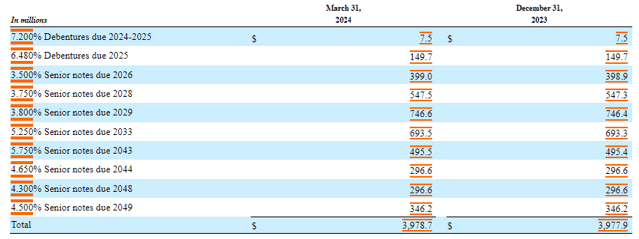

A review of Trane Technologies’ balance sheet shows that the company has total debt of US$4.88b versus cash of US$850m versus net debt of US$4.03b. Most of the debt consists of senior notes with a small portion of 2025 bonds. With a market capitalization of $72.90 billion, the enterprise value is approximately $76.93 billion for a debt-to-enterprise ratio of 5%, indicating minimal leverage in the capital structure. . With trailing-twelve-month EBITDA at US$3.33b, net debt to EBITDA stands at 1.21 times. Free cash flow conversion is a decent 69% based on $2.62 billion of cash flow from operations less $307 million of capital expenditures (Source: S&P Capital IQ).

Company filing

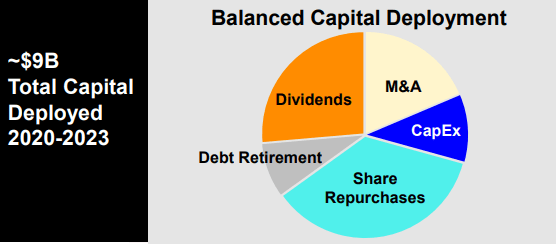

In terms of my outlook for the company, based on historical capital allocation, we can probably expect a balanced capital allocation, leaning toward dividends and stock buybacks, rather than more M&A and debt retirement. As mentioned earlier, the leverage profile is modest and with high multiples in the HVAC space, I do not expect significant opportunities in acquisitions for the company to deploy capital.

From the company’s investor presentation, Trane Technologies expects long-term value creation to come from long-term secular tailwinds, sustainability-focused innovation, margin expansion, and financial strength.

Investor presentation

evaluation

Based on 25 sell-side analysts covering the stock, there are 9 “buy” ratings, 14 “hold” ratings, and 2 “sell” ratings. The average price target over the next year is $320.99, which implies a downside of ~0.34% (essentially flat) so the analysts seem to see the company’s value being fully valued to expensive today. In my view, with such a drastic move in the share price, the valuation has gotten ahead of itself.

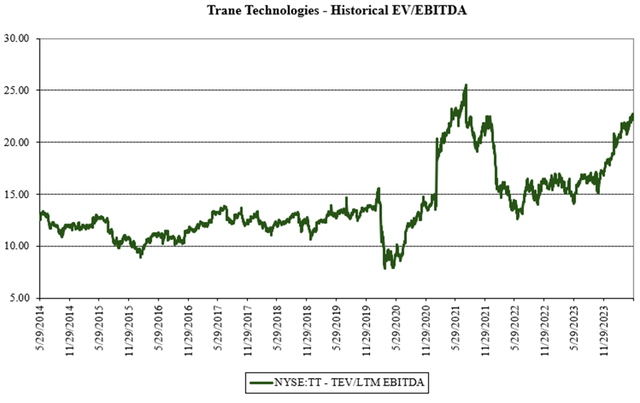

When we look at the company’s historical EV/EBITDA, Trane Technologies is trading at 21.1x EV/EBITDA, which is well above the 10.0x-15.0x range it was trading at pre-pandemic. At present, its valuation has stretched significantly and is now approaching 2021 peak levels. Keep in mind that this is not a high growth industry and multiples in private markets command much cheaper valuations; Medium to high single digit multiples (Source: Bloomberg).

Author, based on data from S&P Capital IQ

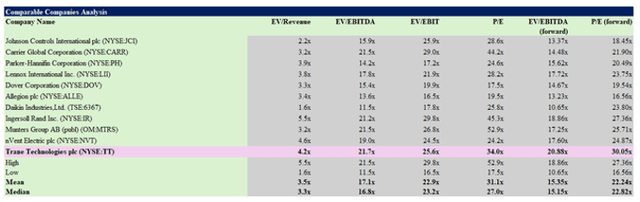

Comparing Trane Technologies to its peers, the company is trading at a significant premium. With forward EV/EBITDA and P/E multiples at 20.9x and 30.0x, the company is certainly not cheap, and it is only a matter of time (in my view) until multiples return to their historical averages and closer. In line with the peer group. Such a valuation is not sustainable for a company that is expected to grow over the long term.

Author, based on data from S&P Capital IQ

Conclusion

Trane Technologies is a global leader in the heating, ventilation and air conditioning (HVAC) market, and its climate and sustainability innovations should support continued outperformance relative to its peers. However, despite the recent rise in share prices on the back of strong demand and margin improvements, the analysis I went through today shows a valuation that appears significantly overvalued, suggesting caution for investors. In my view, while one could argue that the balance sheet is very strong and that its long runway for continued growth could accelerate, I think most of this is priced into the stock today. Since the market expects continued growth, I think it is inevitable that some sort of normalization in transactions will occur. With that in mind, I would caution investors before taking a position today, and wait for a more favorable entry before considering adding it to your portfolio.