Tony Anderson

thesis

Today’s thesis is about Griffon (New York Stock Exchange: GFF), a diversified company offering home and construction products. The GFF has made impressive progress since November 2023; Its stock price rose 54%. Despite the run-up, it looks undervalued, and I think it has potential To grow more. I will discuss the favorable factors and why to prepare, and after analyzing all the factors, I will state my opinion on what to do in case of GFF.

About GFF

GFF is a diversified company that supplies home and building products internationally. The company was founded in 1774 and is headquartered in New York. Below are some of the leading brands owned by the company.

GFF Investor Relations

GFF0 operates in two parts. Home and Building Products (HPB) and Consumer and Professional Products (CPP).

Home and building Products (HP)

In this segment, GFF manufactures and sells garage doors and steel rolling doors through its subsidiary, Clopay Corporation. They sell products through Home Center dealers and retail chains. This sector generates 60% of the company’s revenues. As you know, the construction market took a hard hit in 2023. As a result, the construction sector struggled to achieve overall growth in 2023. In 2024, the construction market saw improvements compared to 2023, especially in the residential sector due to lower prices. Mortgage rates. GFF has seen an improvement in residential door volume, and the improvement in residential volume is expected to drive revenue growth. However, although there has been an improvement in market conditions, they are still far from ideal, and the construction market has not yet fully recovered. Therefore, I expect lower or flat overall revenue growth in FY24 compared to FY23.

The HPB segment was also the main driver of GFF margin growth. EBITDA margin in HPB segment in 2QFY24 was 32.8% while EBITDA margin in CPP segment was 7.1%.

Consumer and Professional Products (CPP)

In this segment, GFF sells professional tools and branded consumer products such as cultivators, post drills, rigs, wire and lumber racks, and storage cabinets through its subsidiary, AMES Companies. This sector generates 40% of the company’s revenues. This segment is currently experiencing a decline in customer demand and volumes in North America and the UK which is impacting the growth of the main product line.

As I mentioned earlier, the margins of this sector are much lower than the margins of the HPB sector. To address this problem and increase margins, it adopted a global sourcing strategy, which I will talk about later in the report. The global sourcing strategy is paying off, and the numbers are improving. Q2FY24 EBITDA margin improved to 7.1% in Q2FY24 compared to 6.2% in Q2FY23. Improving margins in this segment is definitely a big positive for the company and will boost Its profitability. Management expects the expansion of its global sourcing strategy to be complete by December 2024. Management aims to achieve EBITDA margins of 15% in the CPP segment. I see margins improving in the long term, but they may struggle in the short term due to lower demand in North America which could increase discretionary spending.

Tailwind

GFF has some tailwinds that will fuel its future growth. The average age of owner-occupied homes in the United States is 40 years, which is old and will require renovation and remodeling. Therefore, in the coming years, GFF could see good growth, especially in the HPB segment, due to rising remodeling activities.

Statista

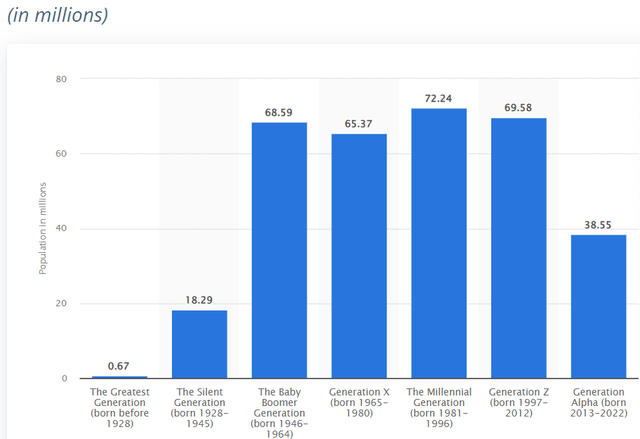

In addition, the population of Generation Z and Millennials is the highest in the United States and is maturing. So a large proportion of people, especially in Generation Z, will be moving out of their parents’ home and many will be starting a new family and GFF will be a huge beneficiary of this due to the increase in family formation.

Moreover, the outdoor living trend is gaining momentum at an impressive pace. Homeowners, especially Generation Z and Millennials, are showing great interest in transforming their outdoor spaces. In fact, 53% of homeowners made changes to their spaces in 2023, indicating a strong and growing market. Spending on renovation also saw a significant increase of 60% during the period 2020-2023. This increased enthusiasm and spending among homeowners could serve as a strong catalyst for the renovation business and the HBP sector.

Market environment

unique

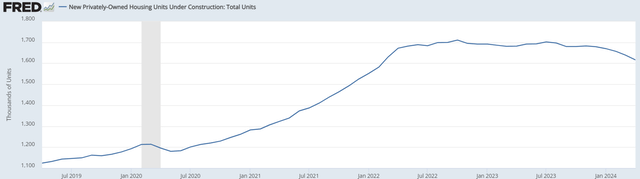

Mortgage rates fell after the 2020 recession, and people took advantage of the opportunity. Construction activity saw growth after 2020. New privately owned residential units under construction continued to rise after 2020. However, due to high inflation rates and rising interest and mortgage rates, the numbers began to decline, and the residential and commercial construction market slowed under. The chart above shows that new construction units peaked in October 2022, but have been declining since then. The mortgage rate rose to 8.45% in October 2023, and since then it has been declining and has reached 7.02% so far, which is lower compared to the average of the past 50 years.

Interest rates remain high in 2024, although interest rate cuts are expected in the second half of 2024. However, no one can say with certainty that we will see interest rate cuts. However, I think we are likely to see further interest rate cuts because we have seen 11 interest rate hikes over 2022-2023, but since the beginning of 2024, rates have not changed, and it looks like the Fed may keep interest rates unchanged and lower them in the end. Down by the end of 2024. The Fed expects a three-quarter point cut in 2024. Looking at these numbers, I believe the current market environment is better than it was in 2023 and is constantly improving. Although I wouldn’t consider it ideal, it would be nice to have some interest rate cuts, in my opinion.

Financial performance

GFF announced 2QFY24 results on May 8, 2024. 2QFY24 revenue was $672.8 million, which was 5.3% lower than 2QFY23 revenue. The reasons for the decline were lower demand in America Northern, UK and unfavorable product mix in the HBP segment. The decline in revenue is justified because the construction market is still recovering from rising mortgage rates and interest rates. Although we saw negative growth this quarter, GFF has recorded good growth since 2020. Its revenue has grown at a CAGR of 7.3% since 2020.

The most notable result was the improvement in margins and income. EBITDA for the CPP segment rose 2% despite an 11% decline in sales. Net income was $64.1 million in 2QFY24; It reported a net loss of $62.3 million in Q2FY23. Therefore, improved profitability was the highlight. The increased efficiency is due to Gryphon’s global sourcing strategy. In order to improve margins and gain a competitive advantage, Griffon adopted a global sourcing strategy, which helped it shift towards an asset-light model. Griffon ceased operations at its four mills and four lumber mills. They also reduced their US facility footprint by 30% and headcount by 600. Griffon’s efforts have paid off for them, and if they continue to dedicate themselves, we will continue to see margin improvement.

I have a positive outlook for margins and see the majority of margin improvement coming from the CPP segment. But talking about revenue, I see consistent growth in FY24. I think we will see revenue growth once interest rates start to come down and the construction market picks up.

Discounted cash flow analysis

Author’s calculations

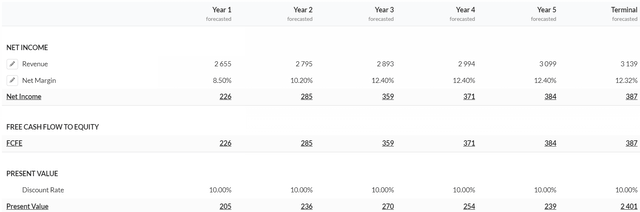

I decided to perform a discounted cash flow analysis because it would give us a rough idea of the fair value of the GFF. I would be very modest in assuming these numbers, because I believe that if we invest, we should assume the worst. You estimate revenue and net income for the next five years. For the first year of revenue, I went with the company’s guidance of $2.65 billion, and for the second year, as I expect the construction market to recover, I assumed five percent growth in revenue, and over the next three years, I assumed 3.5% growth.

As for net income margins, I expect margins to improve because clearly the outsourcing strategy has proven beneficial. Now, in the case of the first year income margin, I went to a 100 basis point improvement. For the second year, I assumed a 200 basis point improvement as there would be no charges related to the global sourcing strategy.

I decided to choose a discount rate of 10% in the case of GFF. Thus, the final value comes to $2.4 billion, and after adding the FCF values, the stock values reach $3.6 billion. Now, to calculate the fair value of GFF, I divide the equity value by the shares outstanding. The number of issued shares is about 49.6 million shares. So, after accounting, the fair value, according to my estimates, comes in at $72.72, which is 7.5% higher than the current share price of $67.52. The DCF model shows that GFF is undervalued; Although the upside is not significant, it is still undervalued.

Take the technology

Trading offer

The griffon was on a roll. Its stock price is up 54% since November 2023. The stock appears to be taking a breather now after a strong run. It is now forming a base at $64.9 and consolidating. The combination will be good after a good period of operation. I think that once the price breaks above the $75 level, we may see another rally, but until then, we could see a good consolidation for about a month or two. For investors, the $64.9 level is important because if the price drops below it, there could be a trend reversal. So investors should monitor this level carefully. Until this level breaks, I think there is no need to worry because the stock looks strong and those who have already invested in it can continue to ride it. However, starting a new position now does not seem ideal, because it is not the best risk-reward setup. New positions can be created after the price exceeds $75.

Bearish scenario

Recent results haven’t been great. Revenues declined, but despite this, GFF’s stock price rose and reached all-time highs. I think the market has taken into account the potential hopes for lower interest rates and improved margin. The situation could get worse if interest rates are not lowered in the coming months. The price could take a major hit if expectations in terms of interest rate cuts and margin improvement are not met. As I told you earlier, revenue growth expectations are not due much to market conditions. So, even if we see flat or slightly negative growth, it may not have a significant impact on the stock price. But the main risk here is that if margin expectations are not met, the rally we have seen in GFF could quickly run out. As of now, these are the only major risks I see in GFF.

Take the final

Griffon seems to be in a good place at the moment. They are taking initiatives to improve efficiency and margins, and they are also successful. There are tailwinds, and it has the potential to grow. In addition, compared to 2023, market conditions are better now. However, I think the market has taken into account the interest rate cuts and margin expectations. Although the valuation seems undervalued, it’s not a screaming buy. Based on the assessment, the upside appears limited. So, considering every aspect, I think the Griffon is the best in my opinion. A patch in Griffon could present an opportunity. But until then, I’d rate Griffon stock as a hold.