Tim Roberts/DigitalVision via Getty Images

we Discuss the purchase Snap Company (New York Stock Exchange: Snap) “cheap” stocks in the $10-$12 range. Snap stock collapsed after the company’s fourth-quarter results in early February. Snap entered in two tranches with an average Buy ratio price around $11 I was very happy with my investment, as we may have hit another long-term low.

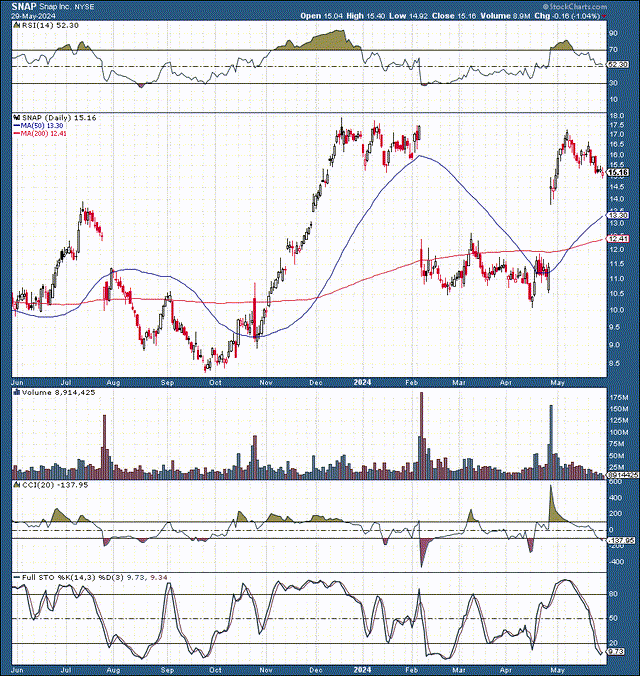

Snap: One-year planner

pop (stockcharts.com)

Snap arrow increased by about 25% After announcing first quarter earnings, which were better than expected. However, the overall gains were more significant, as Snap stock rose about 75% from its recent low of around $10 to its near-term high around the $17.50-$18 resistance range. Even with the pullback to $15-$15.50, my Snap position is up about 40%.

Furthermore, Snap is currently at an attractive buy level, in line with support between $14 and $15. Technical indicators like CCI, Full Stochastic and others indicate that Snap It has become oversold, providing a favorable buying opportunity. This should instill confidence in your investment decision, even if you’re worried about Snap closing the $12-$14 gap.

From a fundamental point of view, Snap looks very attractive. He. She Reported much better than Expected profitThis indicates a strong growth trajectory. Therefore, we do not need to see a closing of the gap from the recent rally after earnings. Snap’s growth and profitability prospects are improving faster and more than expected, providing a reassuring outlook for the future.

Furthermore, Snap should benefit from increased ad spending as the Federal Reserve lowers interest rates and the economy enters a higher growth phase. Snap should also benefit from the tailwind provided by AI, and it seems to be an underrated AI play at the moment.

Snap is also one of the only social media companies able to survive outside of Meta’s social media monopoly and could be a takeover target by a major tech company. Snap is also cheap with about four times next year’s sales, and I like Snap as a long-term investment, as Snap stock has high potential to rise significantly in the coming years.

Snap delivers – there will likely be more upside to come

There’s a reason we’ve seen a 25% post-earnings rally and a 75% trough-to-peak increase in Snap shares recently. Snap’s earnings came in much better than expected, providing a constructive picture regarding the future direction and overall prospects for Snap as we move forward.

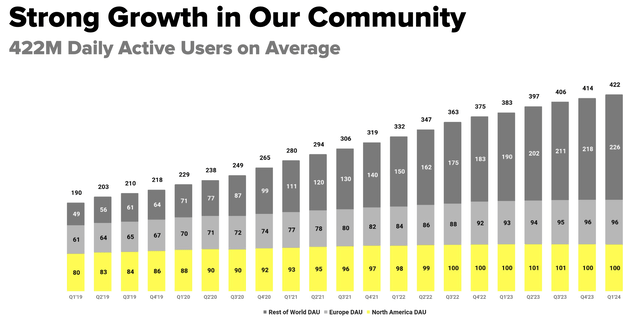

Snap reported non-GAAP Earnings per share of $0.03 in the first quarter, beating the consensus estimate by 8 cents (a big win). Snap’s revenue of $1.19 billion also beat estimates by $70 million, up more than 20% year over year. Q1 daily daily units reached 422 million, an increase of 39 million, an increase of 10% year-on-year.

Time spent watching Spotlight content increased more than 125% year over year. Snapchat+ subscribers more than tripled year-over-year to more than 9 million subscribers in the first quarter. The number of small/medium advertisers increased by 85% year over year.

For the second quarter, Snap reported revenue of $1.225 billion to $1.255 billion, versus the consensus estimate of $1.21 billion, suggesting year-over-year sales growth of 15% to 18%. Given the range of sales forecasts, Snap expects adjusted EBITDA to be between $15 million and $45 million in the second quarter.

Daily active users continue to grow

Daily user units (investor.snap.com)

Snap reported 422 million DAU in its latest quarterly earnings announcement. While DAU growth has stagnated in Europe and North America, the number of DAUs globally continues to rise and should continue to increase. There are more than five billion Internet users around the world make this clear Snap has a penetration rate of only 7.9% globally. Also, we could see accelerated growth in North America and Europe as the company moves forward.

Snap – the favorite platform of “youth”.

Snap is unique because it is the social media platform of choice among young people, who are early adopters and can become Snap users for life, meaning the number of daily active users could skyrocket. Interestingly, Snapchat up to 90% Of the population aged 13 to 24 years and 75% of the population aged 13 to 34 years in more than 25 countries. This dynamic suggests that we could see continued growth in developed markets and globally as more people connect to the Internet and become Snap users.

Snap – is becoming increasingly profitable

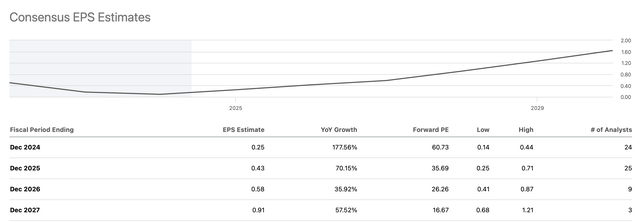

Earnings per share estimates (seekingalpha.com)

Snap’s profitability is improving faster than expected. Consensus estimates call for EPS of $0.25 this year and $0.43 next year. However, given Snap’s tendency to outperform, Snap could achieve EPS closer to higher estimates in the coming years.

Snap has missed EPS estimates in just a year One of the last twenty Quarters. Moreover, while TTM’s EPS estimates were at -$0.08, Snap brought in 11 cents more instead, demonstrating a significantly outperformance of expectations that could continue in the coming quarters.

My forecast is that Snap has the potential to earn about $0.35 to $0.40 this year and $0.60 to $0.70 next year. This indicates that despite the current stock price around $15Snap stock could trade at just 20-25 times next year’s EPS expectations, making it an exceptionally affordable investment for a company poised for significant growth.

What’s more, Snap is not only growing revenue — it generated about $4.6 billion last year — but it also has the potential to grow sales to about $5.5 billion this year and roughly $6 to $6.5 billion in 2025.

Given Snap’s current low valuation, trading at just 4x forward sales, and its enormous growth potential, Snap presents a compelling investment opportunity. In fact, Snap appears to be an affordable option compared to Meta (META), which now trades at about 7 times forward sales, making it an attractive prospect for investors.

Snap’s AI capabilities

Snapchat users Now I have Artificial intelligence chatbot. My AI can answer many questions (trivia and otherwise), advise on the perfect gift for your girlfriend/boyfriend, help plan a weekend trip, or suggest what to make for dinner or eat for lunch. Furthermore, Snap can leverage AI to improve customer experience, increase ad spend, and improve efficiency, leading to increased profitability in the coming years.

One of the only alternatives that still exists

Snap is one of the only massive social networking platforms still standing outside of Meta’s social media “monopoly.” This dynamic makes Snap a highly valuable company, and its value could rise significantly from its current low 25 billion dollars evaluation. Furthermore, as Snap’s profits grow, it may become a takeover target for a tech giant that may want to increase its social media/networking presence.

Bottom line: Snap is a strong buy here

Snap is often underrated and undervalued in the market. Snap went through a difficult phase as advertising spending declined due to rising interest rates and a slow economic period. However, growth is picking up, things are picking up, and Snap’s sales could rise significantly. The social media platform continues to grow, especially among young people. Furthermore, Snap has become increasingly more profitable, recently making another strong earnings announcement. Snap is relatively cheap, has great potential in AI, and could become a takeover target. Snap’s profitability should strengthen, causing the stock price to rise significantly in the coming years.

Where could Snap’s stock price be in the future:

| year | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

| Revenue b | $5.4 | $6.4 | $7.3 | $8.1 | $9 | $9.9 | $11 |

| Revenue growth | 17% | 18% | 14% | 11% | 11% | 10% | 10% |

| Earnings per share | $0.35 | $0.65 | $0.85 | $1.10 | $1.38 | $1.65 | $1.95 |

| Earnings per share growth | 288% | 86% | 31% | 29% | 25% | 20% | 18% |

| Forward price to earnings | 30 | 31 | 32 | 33 | 32 | 31 | 30 |

| Share price | $20 | $27 | $35 | $45 | $53 | $61 | $69 |

Source: The Financial Prophet

I slightly increased my long-term EPS estimates from My previous analysis Due to improved Snap core setup, increased AI capabilities, and other variables. Given its current low price around $15Snap stock has the potential to rise significantly with relatively modest increases in sales, earnings growth, and multiple expansions in the coming years. Therefore, Snap may be an undervalued investment opportunity and an excellent contender to buy and hold over the next decade.

Sudden risks

Snap faces many risks despite my bullish thesis. We should take into account the potential impact of an economic slowdown and potential declines in advertising spending. Snap is particularly vulnerable to declining ad spending, and a higher interest rate for a more comprehensive system could hurt Snap’s bottom line. Snap also faces competition from Meta, TikTok, and other social media platforms/networks. Snap must also keep its users growing and should work to expand its average revenue per user (ARPU), especially in secondary markets where it has growth potential. Snap also risks posting worse or slower-than-expected profitability and slower-than-expected revenue growth. Investors should examine these and other risks before investing in Snap.