com. jxfzsy

The US 10-year bond rate at 4.5% is considered neutral, even if inflation falls (as the real yield should be higher).

We note that the 10-year Treasury yield (US10Y) is at risk of rising towards 5%. As long as monthly readings of 0.3% (or higher) for the Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) are printed. But the latest core PCE deflator came in at 0.2% per month. Triggering these measures could eventually prompt the Fed to cut. So, where are we now with respect to the 10-year bond yield?

First, note our theory that the 2000s provided a correct vision of a “neutral middle environment.” That decade saw an average US inflation rate of about 2.5%, coincided with an average Federal Reserve funds rate of 3%, and an average 10-year Treasury yield of about 4.5%. See more here.

And so if we are In order to achieve a smooth landing and contain inflation, the funds interest rate should not be less than 3%. This determines the final floor. It is possible to raise this minimum, say in the 4% area, if some weaknesses in inflation persist. All of this is important to determine where the 10-year return could go.

Our analysis of the first decade of this year suggests that the 10-year equilibrium yield is around 4.5%, and this actually brings the funds rate down to 3%. A higher funds rate could easily pressure 10-year notes above 4.5%. Essentially, the current 10-year yield does not necessarily represent stark value, even if inflation falls.

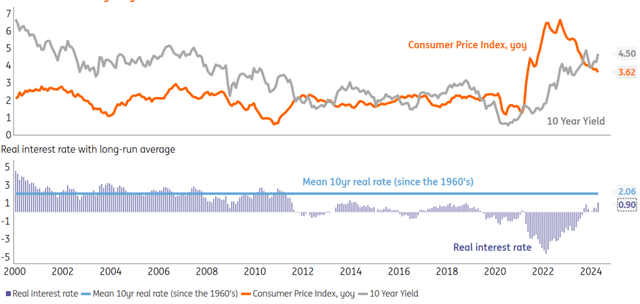

The real 10-year interest rate in the United States is still only 1%. The neutral level is 2%. A lower CPI does not necessarily mean lower revenues…

Source: ING estimates, Macrobond

A lower interest rate could push the bearish limit into the 4% region on the 10-year bond

In addition, we note that the average ten-year real return since the 1960s has been around 2%. It is now around 1% (based on printed inflation rates). Assuming a return to “normal rates” (which we do), we should look for a real interest rate of 2% over the 10-year period. See chart above.

If inflation falls by 1%, this will result in a real rate of 2%. However, this leaves the 10-year Treasury yield unchanged. This is important, because it highlights the fact that the 10-year Treasury yield does not necessarily have a good reason to fall simply based on the idea of lower inflation.

But here’s why the 10-year Treasury yield might fall:

Interest rate cuts usually coincide with a decline in longer-term bond yields. See here for more; It shows that significant falls are typical before and after the first cut. Accordingly, if the Fed begins to taper in the coming months, a move to 4% (or lower) for the 10-year Treasury yield would not be unusual.

In fact, we are calling for such an upward movement. It will bring with it a rationale for asset managers to take tactically long positions at an early stage (before the first cut), and for liability managers to either issue or lock in interest rates at a later stage (after the first few cuts). However, we believe that this window will be short (no more than a few months), and will end before the Fed completes its interest rate cutting cycle.

Ultimately, 5% is the 10-year level that is still being debated

However, a 10-year Treasury yield at 4% (or lower) is not an equilibrium outcome, as lowering interest rates would coincide with the building of a positive yield curve. The 2000s-style normal (average) curve would include a premium of 150 basis points in the 10-year yield.

This quickly brings the 10-year rate back to 4.5%. If the funds rate fails to return to 3%, say the lows of 4%, we can quickly see a case for a 5% 10-year yield. Financial pressure factor / issuance pressure We can also reach the 5% level, even from the 3% minimum funds.

Bottom line, the 4.5% 10-year bond yield we see today is neither high nor low. It’s a bang on what we consider neutral. Balance is a big word, but it’s here in our opinion. Even if inflation falls, the 10-year real yield is too low to simply decline accordingly.

The key element is lower interest rates, as this usually leads to lower longer term interest rates. We will reach 4% over the 10 years as the Fed rate cut discount tightens and the Fed begins cutting.

But this goes beyond the negative side. So, barring a systemic collapse, don’t expect to stay there. Add to that additional financial factors and a 5% rate seems fairer (above normal), after the early stages of interest rate cuts.

Hence, the more natural outcome over the medium term is for the 10-year bond yield to tend to stabilize near 5% rather than 4%.

Content Disclaimer

This publication has been prepared by ING for information purposes only without regard to a particular user’s means, financial situation or investment objectives. The information does not constitute an investment recommendation, nor is it investment, legal or tax advice or an offer or solicitation to buy or sell any financial instrument. Read more

Original post

Editor’s note: The summary points for this article were selected by Seeking Alpha editors.