Justin Sullivan/Getty Images News

Nvidia company (Nasdaq: NVDA) The stock price continues to defy gravity at stretched valuation multiples, but I remain on the sidelines due to three reasons I discuss in this article: slowing revenue growth, intensifying competition from developed companies micro devices (AMD), and extended valuation multiples that assume continued high growth rates for many years.

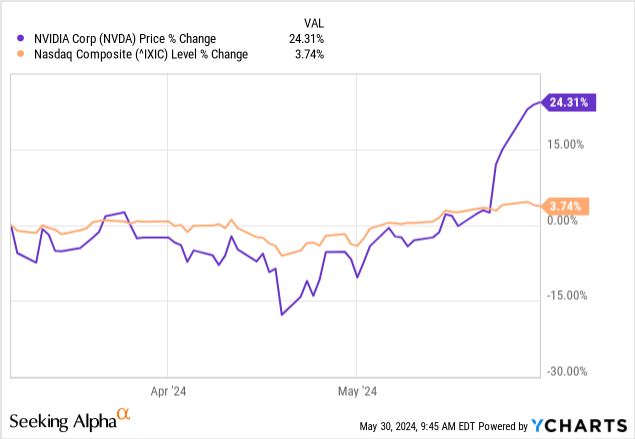

I last reviewed NVDA stock in “Nvidia: Consider a Sell Amid Insider Selling and Extended Valuations,” where I highlighted that most sell-side analysts view the stock favorably, suggesting the boat may be full, and discussed a sell-off. An extensive insider on the stock, discussing the company’s valuation complications, and I recommend reading it. After my article, NVDA’s performance fell 17 percent in seven weeks, underperforming the Nasdaq (COMP:IND) during that period, but then recovered and outperformed the index significantly, especially Since its last earnings release, which I’ll review in the next section.

Nvidia’s growth is slowing down

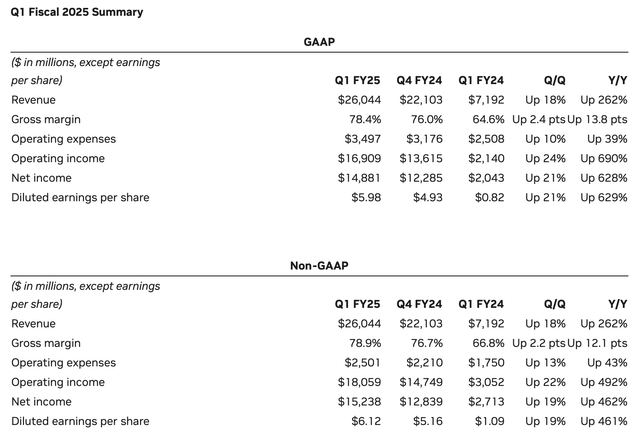

On May 22, Nvidia announced its first-quarter fiscal 2025 financial results, and the company blew away consensus estimates on all fronts from the bottom line to the bottom line as well as guidance for the following quarter. The following table shows Nvidia’s GAAP and non-GAAP results for the first quarter of the year, compared to the most recent quarter and the same quarter last year.

Nvidia Investor Relations

I won’t rehash the company’s results, except to highlight two key points, followed by a substantive comment from Microsoft that I’ll discuss later in the article.

First, Nvidia’s revenue guidance of $28.0 billion for the second quarter of fiscal 2025 represents a sharp deceleration in the company’s revenue growth rate, both on a quarterly basis from 18% in Q1 to 8% in Q2, and on an annual basis. – On an annual basis, from 262% in the first quarter to 107% in the second quarter. Although the year-over-year growth rate remains high, I stress that the growth rate is declining, and I expect it to continue to decline over the coming quarters due to the two reasons I discussed in the competition section of my previous article and the material comment from Microsoft that I will discuss later in This article.

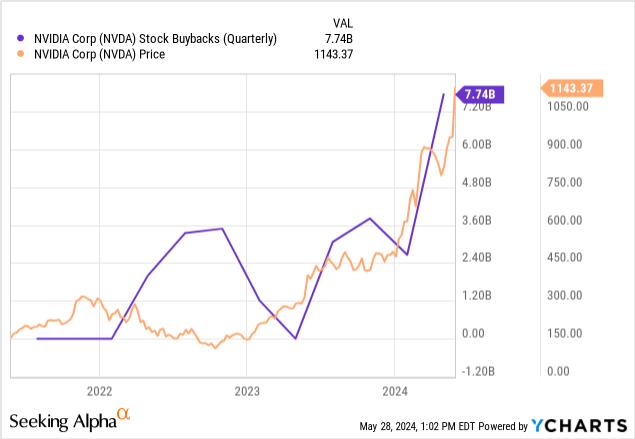

Second, Nvidia repurchased $7.74 billion of its stock, according to a cash flow statement included in the earnings release, representing the largest amount of stock repurchases the company has ever made despite the stock trading near its all-time high throughout the first quarter. :

Before continuing, please review the competition section of my previous article, in which I speculated that AMD MI300X accelerators “could upend the status quo and lure potential customers away from Nvidia’s offerings.”

Shootout: Microsoft partners with AMD

Last week, Microsoft (MSFT) held its annual developer conference, and in a pre-conference analyst briefing, Scott Guthrie, executive vice president of Microsoft’s Cloud and AI group, described AMD MI300X accelerators as… “The most cost-effective GPU currently available for Azure OpenAI.”

The above comment supports my argument that the AMD MI300X poses a material competitive threat to Nvidia’s dominance in data centers. Furthermore, AMD issued a press release discussing its growing partnership with Microsoft and outlining the competitive challenge it poses to Nvidia. The most important takeaway from the long press release is that Microsoft is now using AMD’s MI300X accelerators to run Azure Open AI ChatGPT 3.5 and 4, “which are some of the most demanding AI workloads in the world,” and because I can already see the “but CODA!” Replies at the bottom of this article Let me also point out that the AMD ROCm software is used to run the new Microsoft Azure ND MI300X virtual machines that customers are using like Hugging Face.

With that material commentary in mind, let’s review Nvidia’s valuation multiples.

Nvidia’s valuation continues to stretch

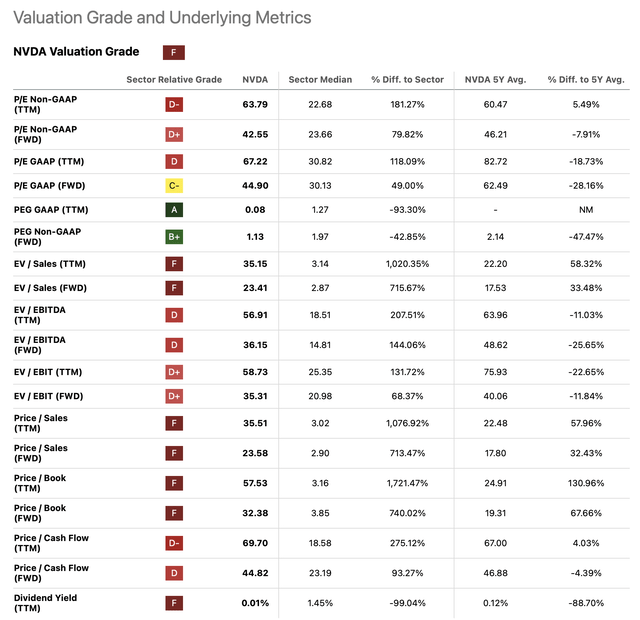

Seeking Alpha does an excellent job of summarizing the valuation metrics for all companies, and I’ve included a table of valuation metrics for Nvidia below:

Find Alpha Premium Tool

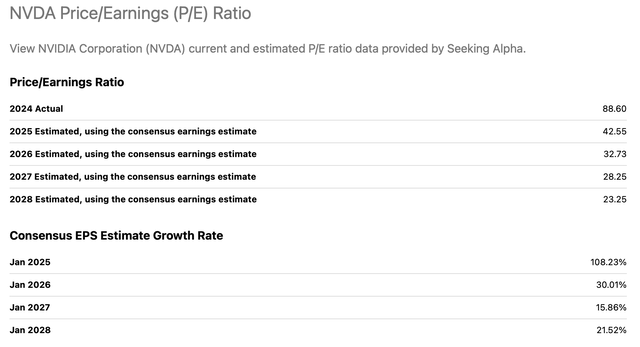

Almost all of Nvidia’s valuation multiples continue to be stretched on a historical and forward-looking basis, but as the following table shows, sell-side analysts expect the company’s valuation multiples to decline rapidly over the coming years. if Growth rate assumptions met:

Find Alpha Premium Tool

The main takeaway from the above tables is that the growth rates indicated by consensus forecasts fall sharply from 108% in FY2025 to 30% in FY2026. This poses a material risk to those shorting Nvidia stock. Management’s comments on a recent earnings call regarding demand for existing H200 and upcoming Blackwell platform chips suggest there is room for growth estimates to increase over the next few quarters (emphasis added):

While the display holds on the H100, we’re still tight on the H200. Meanwhile, Blackwell is in full production. We are working to roll out our system and cloud partners for global availability later this year. Demand for the H200 and Blackwell far exceeds supply We expect demand to exceed supply well next year.

However, having pointed out this risk, I will closely monitor the relative market shares of Nvidia, AMD, and other players to better understand and forecast growth trajectories for all players in the industry beyond the next two years. Given the comments from Microsoft, my view is that material downside risk exists in the growth assumptions included in Nvidia’s forecasts beyond FY2026.

I actively participate in the comments under my articles because I want to engage with readers to speed up feedback loops and directly address any interruptions in discourse as quickly as possible. If you agree or disagree with me, feel free to share your thoughts below this article. I look forward to learning from you.

Bottom line

Nvidia’s technology leadership continues with the Blackwell platform for next-generation chips, but as Microsoft’s comments point out, the AMD MI300X is a cost-effective alternative, the latter fact not yet appreciated by market participants. Although the outperformance of Nvidia’s stock price may continue in the coming weeks, I would caution investors not to chase the stock because competitive analysis suggests a close gap between Nvidia and its competitors. I continue to evaluate Nvidia stock He sellsI will update my analysis in upcoming articles.