Soulskin

As a value investor, I prioritize valuation above almost everything else. But more often than not, there is a company that may not seem cheap, but it can still require investment. One of these possibilities, in my opinion, is just that Alexandria Real Estate Equity Company (New York Stock Exchange: Is), a real estate investment trust that focuses on markets where the medical, pharmaceutical, and biopharmaceutical industries represent a major source of economic activity. By capitalizing on this area, the company has achieved rapid growth recently. Unfortunately, stocks, while not expensive, aren’t cheap either. Compared to other REITs, you can even consider the units to be expensive.

My overall history with the company is somewhat mixed. Since my last article on the company, where I rated it a “buy,” shares are actually down 0.4%. This pales in comparison to the 11.2% increase it saw Standard & Poor’s 500 (SP500). For context, this article was published in January of this year. On the other hand, since the first rise condition In the company back in October 2023, shares rose 27.6%. This is marginally higher than the 23.8% increase seen by the broader market over the same time period.

Although I acknowledge that the stock is relatively expensive compared to what’s out there, I think this premium probably makes sense to buy. The company has little leverage compared to other companies out there. Additionally, he shows no signs of stopping the growth spurt. Although the market has been down in business lately, I see continued growth should push the stock higher. For this reason, I think my decision to keep it at a ‘buy’ rating earlier this year still makes sense.

Keep believing

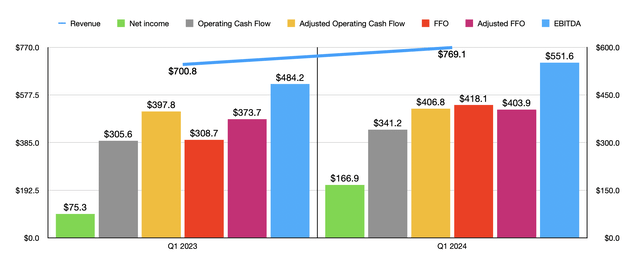

Since I wrote about Alexandria Properties shares in January, we’ve seen some additional data emerge about the business. The most recent data covers the first quarter of fiscal 2024. During that period, revenue was $769.1 million. This is 9.7% more than the $700.8 million generated just one year ago. Only a small portion of that growth, about $7.9 million, came from properties the company previously owned. This appears to have been largely driven by rising rents. Meanwhile, most of the growth, totaling $55.1 million, came from acquired properties. Notably, another $5.3 million in revenue growth came from tenants redeeming previously owned properties. But in the grand scheme of things, this is only a small piece of the overall pie.

Author – SEC EDGAR data

In conclusion, things are going well. Operating cash flow was able to grow from $305.6 million in the first quarter of 2023 to $341.2 million in the first quarter of 2024. If we adjust for changes in working capital, the increase was more modest, from $397.8 million to $406.8 million. There are, of course, other profitability metrics that investors should pay attention to. One of these is FFO, or funds from operations. This metric jumped from $308.7 million to $418.1 million. On an adjusted basis, it managed to rise from $373.7 million to $403.9 million.

Author – SEC EDGAR data

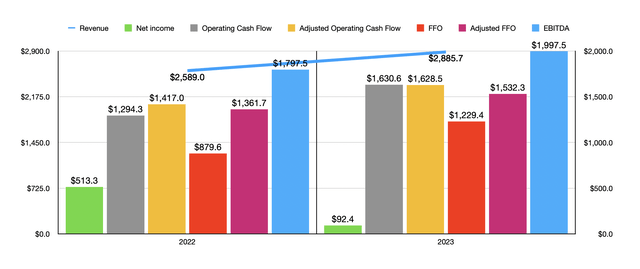

When I wrote my previous article on the business, we only had data through the third quarter of 2023. So it might be helpful to understand how the company finished fiscal year 2023 and how that compares to results from 2022. In the chart above, you can see that exactly. Revenue of $2.89 billion beat the $2.59 billion generated one year earlier. Naturally, the company’s profits increased during this time period as well. Each cash flow metric saw fairly attractive growth year over year.

When it comes to the full fiscal year 2024, management has provided a great deal of guidance. We don’t know yet what revenue should look like. However, FFO per share is expected to be around $9.55 at the midpoint of guidance. This means FFO is approximately $1.64 billion. This represents a 33.6% increase from the $1.23 billion generated one year ago. On an adjusted basis, it should be about $9.47 per share. That should be about $1.63 billion, a 6.3% increase from the $1.53 billion generated one year ago. Other profitability metrics are up in the air, as management has not provided guidance for them. But if we expand those at the same rate that adjusted FFO should rise, we expect adjusted operating cash flow of $1.73 billion and total EBITDA of $2.12 billion.

This year-on-year growth should be driven by several factors. Some of this growth should come from acquisitions. Management expects to spend between $250 million and $750 million on these specific activities. This will be largely funded through asset sales of between $900 million and $1.90 billion. But the greatest growth should be attributed to the construction of new properties. The administration pegs this amount at between $1.95 billion and $2.55 billion for this year. All of this should lead to increased debt compared to what the company had at the end of 2023 of about $900 million.

Author – SEC EDGAR data

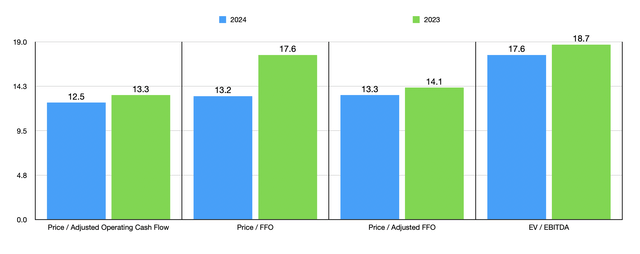

If we use these estimates to value the company, the shares don’t look particularly expensive. But it doesn’t look cheap either. In the chart above, you can see exactly what I mean. I then decided to compare the company to five similar companies as shown in the table below. This table looks at only two of the four evaluation metrics. But the overall data is telling. On a price to operating cash flow basis and on a compounded value to EBITDA basis, four of the five companies are cheaper than our filter.

| a company | Price/operating cash flow | Value added/EBITDA |

| Alexandria Real Estate Equities | 13.3 | 18.7 |

| Boston Properties (BXP) | 7.7 | 15.4 |

| Vornado Realty Trust (VNO) | 7.8 | 16.8 |

| Kilroy Real Estate Company (KRC) | 6.7 | 11.9 |

| Cousins Incorporated (CUZ) Properties | 9.7 | 12.2 |

| SL Green Realty (SLG) | 21.7 | 33.2 |

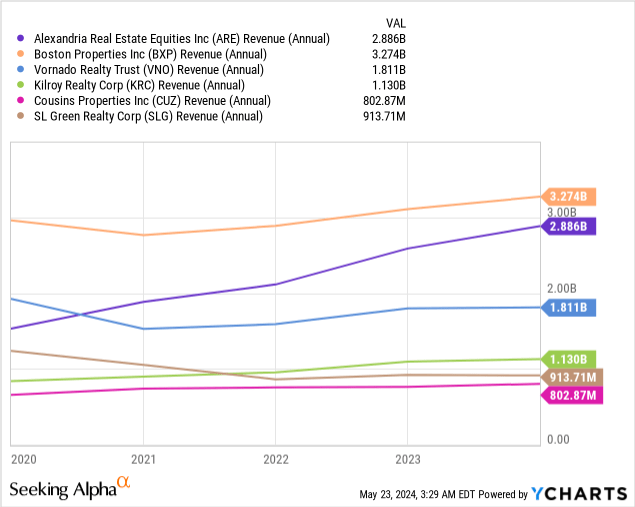

With numbers like these, you might be wondering why I’m still bullish on Alexandria Real Estate stocks. If anything, this kind of price discrepancy would typically warrant a “Hold” rating. However, part of my optimism stems from the fact that management has done a great job growing the company recently. In the chart below, you can see the revenues over the past five years compared to the revenues generated by the same five companies you decided to compare them to. Certainly, Alexandria Real Estate Company outperformed its competitors.

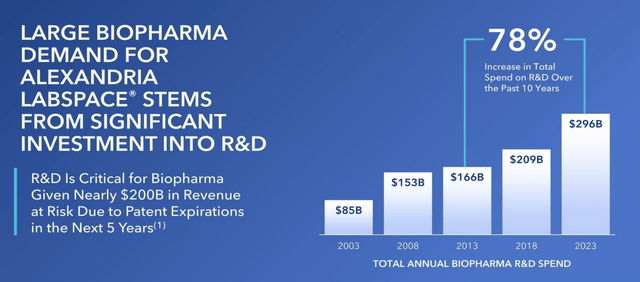

Of course, just because revenues have grown quickly in the past doesn’t mean they will continue to do so. However, I would argue that there is reason to believe that it will continue for the foreseeable future. As management noted in a presentation to investors when they announced financial results for the first quarter of this year, global spending on biopharmaceutical R&D totaled $296 billion. This represents a 78% increase compared to the $166 billion spent ten years ago in 2013. This results in an annual growth rate of about 6%. From 2019 to 2023 as a whole, global spending on biopharma R&D, as well as all other aspects of the life sciences market, exceeded $2.1 trillion.

Alexandria Real Estate Equities

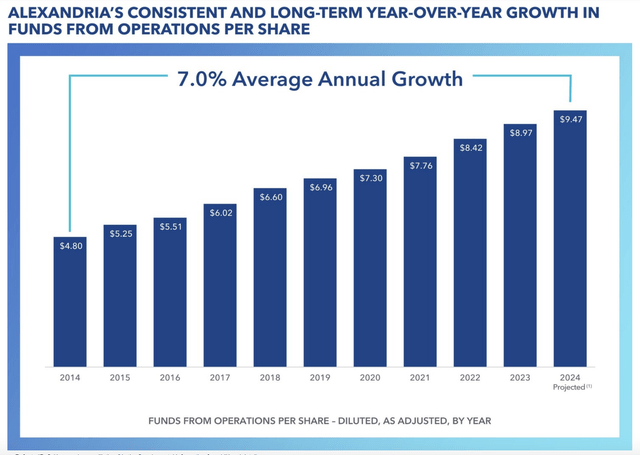

Of course, revenue growth isn’t the only thing that matters. In fact, I would argue that what’s even more important is increasing the company’s earnings per share. Fortunately, management makes this simple. As the first image below shows, from 2014 through an estimated 2024, the annual adjusted FFO growth rate per share increased by about 7%. This number is expected to be a little slower, reaching about 5.6% this year compared to last year. But this is still a respectable increase in my opinion.

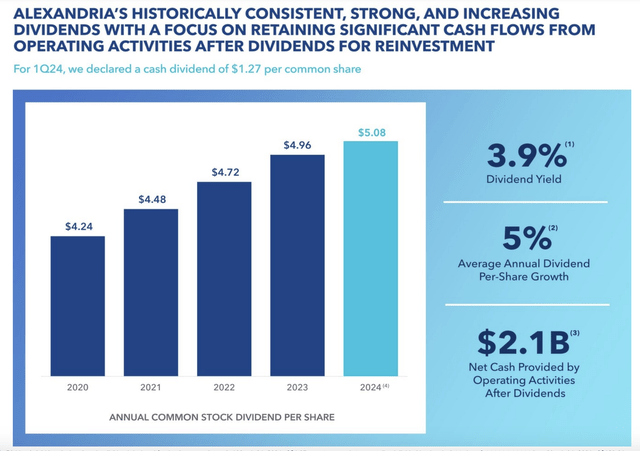

As the second image below shows, the company has recently raised its dividend per share on an ongoing basis. So management has a good track record of creating growth in stock value and returning capital to investors.

Alexandria Real Estate Equities

Alexandria Real Estate Equities

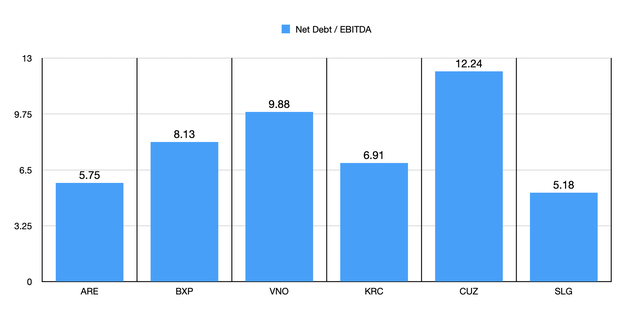

You would think that a company that pays a respectable dividend and is experiencing this kind of rapid expansion would also be laden with debt. But this is not the issue. As shown in the chart below, the company’s net leverage ratio, using 2023 results, is 5.75. Only one of the five companies I compared it to had a lower leverage ratio. So, in addition to having a better growth record and an interesting market to operate in, Alexandria Real Estate stock is less risky from a leverage perspective than four of the five companies I’m comparing it to.

Author – SEC EDGAR data

Away

In my opinion, Alexandria Real Estate stock is certainly not a value investment. Instead, I would describe it as a GARP (Growth at a Reasonable Price) candidate. The company’s performance is very good, and I see no reason to believe that this trend will change in the near term. One day, growth prospects will slow. But until that happens, given how the stock is currently priced, I would argue that the organization should definitely be considered for investors who want a high-quality business and aren’t afraid to pay a bit of a premium for it.