Editorial by Julia Dorian/iStock via Getty Images

Note: All amounts discussed are in Canadian dollars and the share price refers to the TSX share price and not the OTC price.

Boston Pizza Royalties Income Fund (TSX:BPF.UN:CA) earns 4% royalties on Total sales of Boston Pizza franchisees in the equity pool. It also makes another 1.5% of distribution income due to its ownership stake in this instead Simple structure. the Financial reports Also provide (less robust) details about this fund and its relationship to income sources.

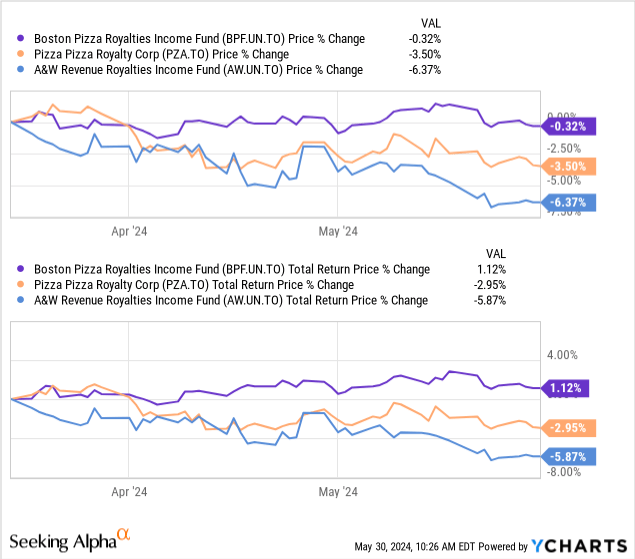

We were neutral on this fund when we covered it in March of this year and the price has been fairly flat since then.

On a total return basis, it has stayed afloat and outperformed the other two top players we cover, Pizza Pizza Royalty Corp (TSX:PZA:CA)) and the A&W Royalty Income Fund (TSX:AW.UN:CA). Returning to Boston Pizza, our rating was based on the expectation of a slowdown in growth and even potential sales and thus lower distributable cash flow in the event of a recession. What happened was benevolent immigration policies (we use it very loosely here) in her country of origin, which increased demand. Being a highly profitable company, its bottom line was not a slave to fluctuations in expenses bought by inflation either. Its 8% yield was attractive, but we liked it at just under $15.

We think the yield is attractive even if we assume a very low growth rate and focus on dividends only. Intuitively, we feel like this is almost here, but we can probably get it for a bit cheaper. We are keeping this on hold and increasing the Buy For Less price to $15.00 to account for the growth we have seen since our last update.

Source: Boston Pizza: ROE of 8.5% sounds attractive

We’ll review the Q1 numbers next to see if we need to raise our purchase price, since the price hasn’t reached us.

First quarter-2024

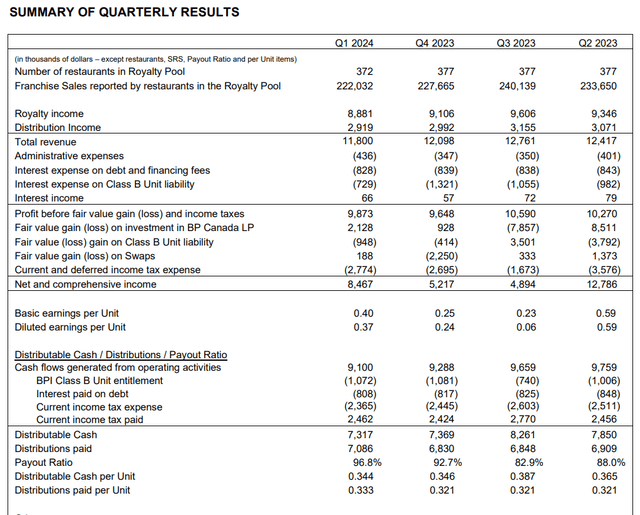

This was not a good quarter for Boston Pizza. We saw slight declines in all relevant metrics compared to the first quarter of 2023. Total franchise sales decreased 1%. Same store sales decreased 1% and cash flow from operating activities decreased 1.3%. Interestingly, distributable cash flow increased by about 1.8% overall Interest paid Debts decreased by about 10%. We will note here that this was the difference in interest paid and not in the interest expense itself. The latter was actually higher than one might expect with a slightly larger debt load and higher interest rates. The bottom line here was that key metrics were lower, but timing factors on cash movement, boosted distributable cash flow. Naturally, this will reverse in the other direction in a quarter or two, so it’s important to pay attention to major fundamental changes and not be alarmed by the higher distributable cash flow seen.

Q1-2021 MD&A

The tone was sombre during the conference call as well.

The first quarter of 2024 presented some macroeconomic challenges for the full-service industry, and prevailing economic conditions characterized by rising interest rates and inflationary pressures have impacted consumer behavior, impacting discretionary spending and leading to a cautious approach to dining out.

Source: Boston Pizza Q1 2024 conference call transcript

This may have been influenced by the fact that Boston Pizza got here despite some aggressive marketing and promotional campaigns.

From a marketing standpoint, we kicked off Q1 2024 with our Pasta Tuesday promotion all month long, where guests were able to enjoy pastas every day of the week, starting at $11.99 and Savory Pastas for $15.99 all month long in January.

The promotion was supported by major television, digital and social media channels, along with in-restaurant promotions at participating Boston Pizza restaurants across the country.

Source: Boston Pizza Q1 2024 conference call transcript

Expectations and judgement

Sales continued to slow in April.

But Nick, it’s more to your question regarding the trend over the quarter. So, yes, looking at January, February and March results for the fourth quarter of 2024, same restaurant sales were pretty flat during the quarter. So, the 1% that we ended the quarter at, was pretty consistent throughout the first quarter. There was a bit of a lumpiness from week to week as you would expect where there were certain kind of calendar timing differences driving that, but somewhat from a trend perspective, yes, it was a fairly consistent trend throughout the quarter.

As far as April goes, what I would share there is that there is no kind of dramatic swing up or down. It’s really kind of consistent trends that we’re seeing compared to the first quarter results.

Source: Boston Pizza Q1 2024 conference call transcript

Some other context here is that menu prices on average are definitely higher than they were a year ago. We haven’t gotten an exact figure for this from management but our estimate is that this is closer to 4%. So, when you combine that with a 1% decrease in sales, you can conclude that traffic is down about 5%.

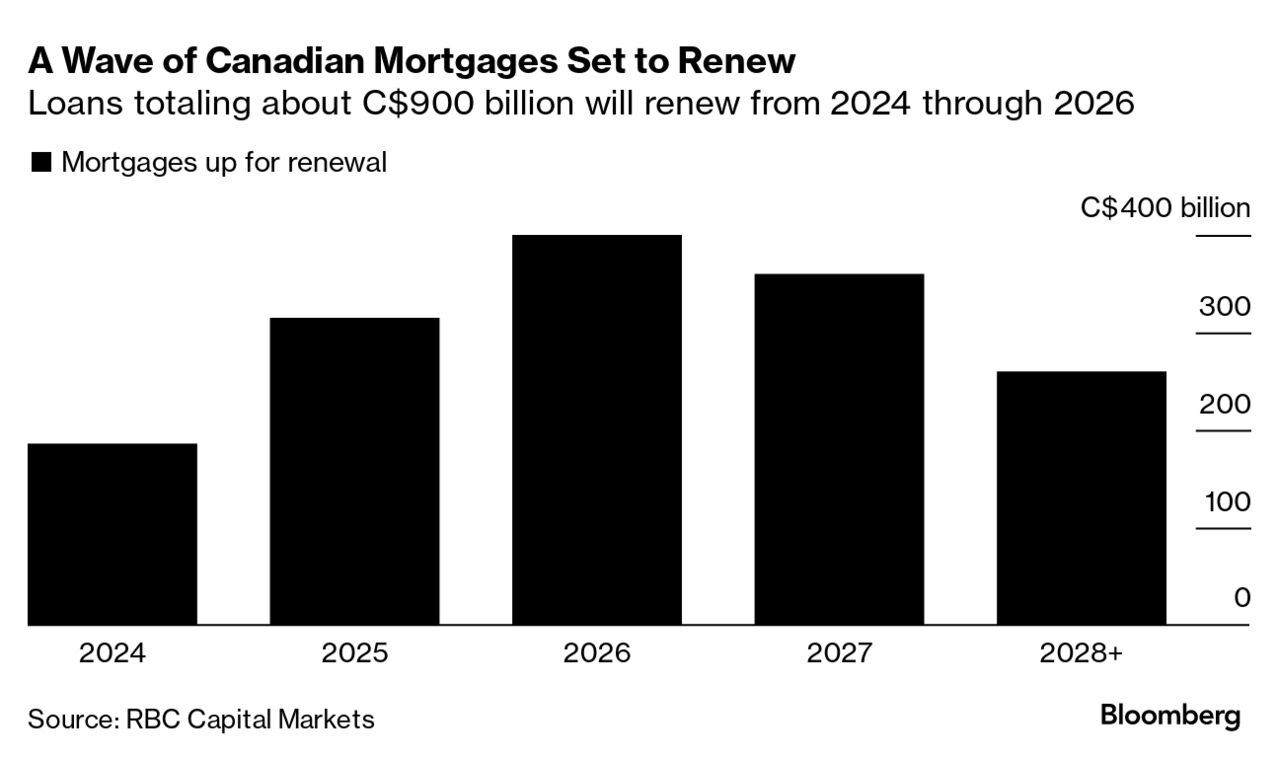

We would be more optimistic here if we were at the end of a recession. The biggest macro issue here, whether we reach official recession criteria or not, is the payment shock with the mortgage reset. This is when Canada’s penchant for 5-year mortgage terms (versus 30 years in the US) will really matter.

RBC/Bloomberg

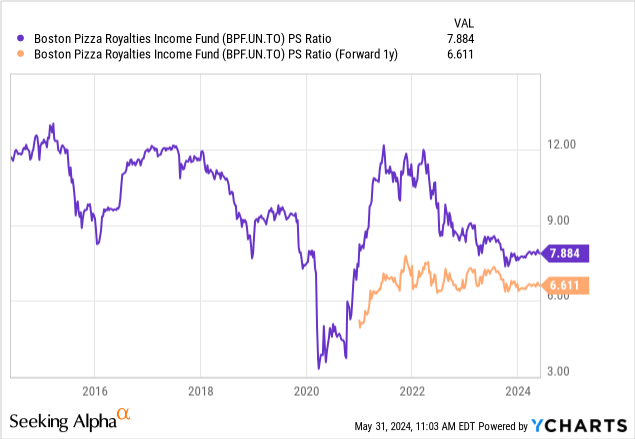

What offsets this pressure, on a marginal level, is the increase in the country’s population due to uncontrolled and (absolutely insane) immigration policies. The rating isn’t the worst we’ve seen either. On a price-to-sales basis, the stock actually looks modest compared to its history. Of course most of this contract is colored using ZIRP so context is key.

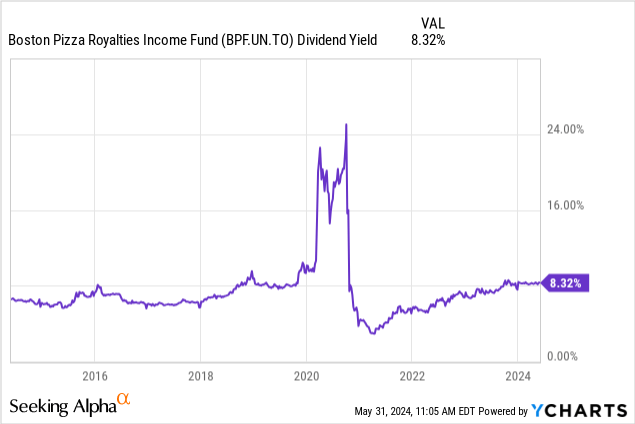

The dividend yield is also looking at the upper end of its decade-long range.

The slightly higher price point compared to the other two Canadian Royal Plays we cover is a weakness that makes us wary. Overall, we think this remains a buy at just under $15.00. We are maintaining our hold rating for the time being.

Please note that this is not financial advice. It may seem so, it seems so, but surprisingly it is not. Investors are expected to conduct their due diligence and consult with a professional who knows their objectives and limitations.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.