VV shots

Gap Company (New York Stock Exchange: GPS) is one of the largest fashion retailers in the United States. The company has more than 2,500 directly managed stores and 1,000 stores operated by licensees.

This article discusses the company’s results and profits for the first quarter of 2024 communicate. The company reported comparable sales growth of 3%, nearly 600 basis points of operating margin expansion, to EPS of $0.41, compared to a loss last year. More importantly, the company showed a significant rebound in profit margin and improvement in comparable sales across all of its brands. The market liked the results, with the stock rising nearly 30% the day after the release.

Since this is my first time writing about The Gap, I am also providing my assessment of the positive and negative characteristics of the company. The Gap is a company with great potential, undergoing a successful turnaround, with a lot of brand equity and investment In growing those brands. At the same time, it is a company that has faced TAM limitations in the past and has struggled to grow for more than a decade.

Finally, I evaluate the company’s stock as an opportunity. Despite some positive characteristics of the company compared to its peers, its valuation is high for a clothing retailer that has shown limits to growth. For this reason, the stock is not an opportunity and I value it as a hold.

Positive results for the first quarter of 2024

Gap’s earnings were received very favorably by the market, with the stock jumping 30% in one day. The reason behind the excitement is that the company has been able to deliver revenue and margin growth across all of its brands.

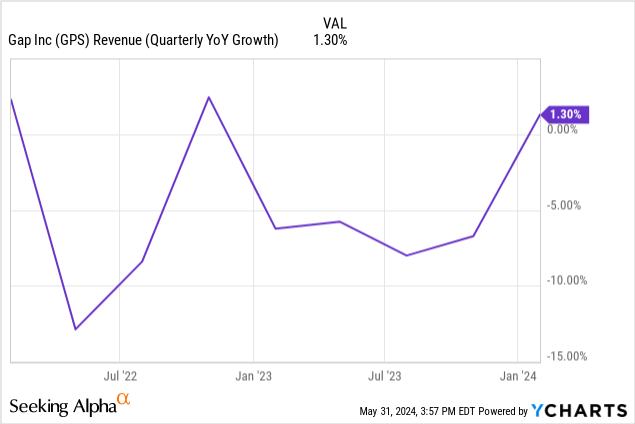

On an aggregate level, the company recorded revenues of $3.4 billion, showing a similar growth rate of 3%. This is the second straight quarter of revenue growth after nearly two years of consistent revenue losses (chart below ends in 4Q23).

Importantly, the company recorded similar growth across all brands. In particular, Banana Republic and Athleta reported revenue growth, driven by high-single-digit declines in 4Q23.

Another important data point is the cost increase posted by the company. Gross margins expanded by approximately 400 basis points, with 300 basis points coming from merchandise (about two-thirds of which was due to lower costs) and another 100 basis points coming from occupancy leverage. SG&A benefited another 140 basis points. The company manages merchandise properly, with inventories down 15% year-on-year and sales increasing, meaning high inventory turnover.

Finally, the company updated its guidance for FY24 from flat sales to growing sales with higher margins. We will deal with this separately in the evaluation section.

Duran story

The Gap is going through a major transformation, trying to recapture its glory days from the late 1990s and early 2000s. Here, I cover this process as well as some introduction to the company’s history and current operations.

King of retail: The Gap is one of the largest clothing retailers in the United States and perhaps the largest retailer of brand-name clothing (the largest being general retailers like Walmart or TJ Maxx).

Brand portfolio: The Gap participates in four different branded clothing marketplaces. GAP (the brand) serves young adult customers with trendy basics; Old Navy serves the whole family with value-priced products; Banana Republic offers a luxurious and aspirational lifestyle to young consumers; Finally, Athleta operates in the women’s sportswear market.

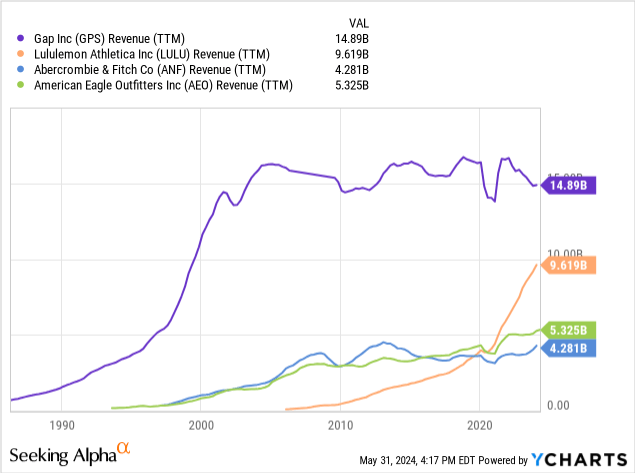

I have reached the limit: As can be seen from the revenue chart above, the company reached its ceiling in the early 2000s, at about $16 billion in sales, which it has not been able to surpass since then, despite having four large brands. Many retailers face this problem at some point due to the complexities of large supply chain management and because fashion requires a certain segmentation to attract customers, which limits the company’s potential.

US saturation, international opportunity: The company seems to cover the US market well, as there are about 2,500 stores between the US and Canada. However, international markets are less covered today, with only 1,000 stores operated by licensees. International sales account for just 13% of revenue in fiscal 2023.

New CEO: After repeated failures in the post-pandemic market, The Gap replaced its CEO in early 2023. The company brought in the CEO of Mattel, which had found success by revitalizing the Barbie brand after it had lost its cultural relevance. The new CEO brought a strategy focused on more disciplined operations, higher marketing expenditures, and a revamped culture.

Strategy progress: The reason for the jump in the stock after the first quarter results of 2024 is likely due to the market assigning a higher probability to the company that is actually working on this new strategy. As mentioned earlier, the improvement in trading (higher gross margins, lower inventories) and improvements in SG&A leverage are very positive.

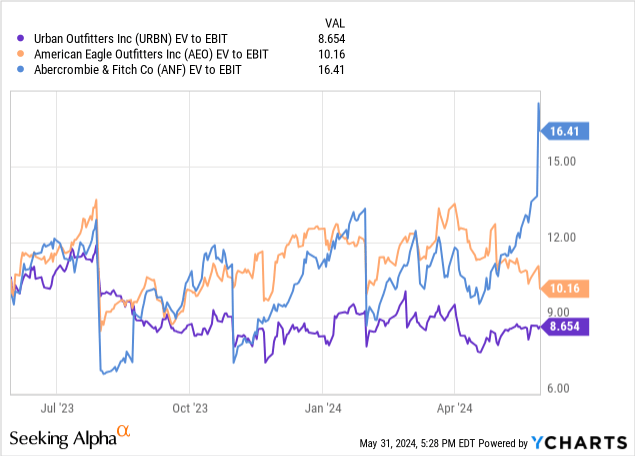

Intangible investments: One of the things I love most about The Gap’s new strategy is the focus on intangibles and brand building. This is something that is relatively absent in calls from other fast fashion retailers like Abercrombie (ANF), American Eagle (AEO), or Urban Outfitters (URBN). Last year, the company hired its first creative director (Zac Posen). She has also invested in several heavy-hitting campaigns, including as supermodel Taylor Hill for Banana Republic; top-tier athletes Simone Biles, Katie Ledecky, and dozens of others from Athleta; GAP’s Linen Moves campaign (which reached nearly 1.5 million views on YouTube, which is unusual for a brand campaign); And smaller campaigns for the Old Navy.

The importance of creativity: The Gap can have a more defensible position than other retailers (such as the stores mentioned above) by having a more fashion-forward assortment. The brand has been known for promoting many styles in the past and building a strong follower base through creative advertising. In contrast, other retailers tend to be more passive, and follow trends. This ends with the delivery of their products.

Controllable leverage: My last point relates to the company’s balance sheet. The Gap closed the quarter with $1.5 billion in cash. The company also has a very attractive $1.5 billion senior notes, earning a low fixed interest rate of 3.75%, maturing in 2029 and 2031.

evaluation

Now is the time to evaluate The Gap, comparing its business characteristics to its asking price for its stock. I will start by listing the positive and negative attributes of the company.

On the positive side, I’d put the company’s strong balance sheet, sheer scale, diversification in terms of brand and pricing, successful strategy (so far), and high focus on intangibles (versus other retailers).

As for the negatives, I include the company’s past challenges to penetrating its TAM, which likely indicates market saturation. I also mention that The Gap is an apparel retailer, a competitive category where trends must be matched annually for the company to perform profitably. Apparel is also a discretionary category, meaning it stagnates more. This means that despite The Gap’s positive characteristics, the company faces a relatively restricted and volatile market.

Considering the valuation, at Friday’s market close, GAP recorded a market capitalization of $11.1 billion ($29 by 383 million diluted shares). The company’s EV is essentially the same, since cash is offset by preferred bonds.

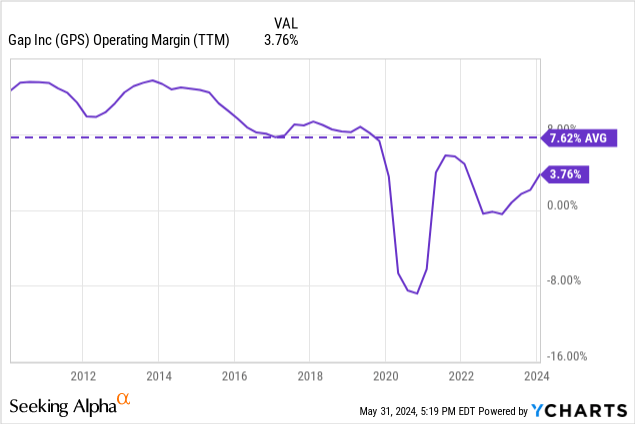

We can compare this to the company’s guidance for FY24. Guidance is relatively conservative on the top line, where the company expects slight growth (maybe 1/2%). It’s much less conservative on its bottom line, seeing operating income expand 45% to $879 million from $606 million last year. This increase is driven by the benefit of higher gross margins through a stable SG&A base. Guidance operating income indicates an operating margin of 5.7%, which is below Q1 levels (6.1%) but within the level the company was operating at before the pandemic. Finally, applying a 28% tax rate results in a NOPAT of $660 million for the year.

So, at current prices and using management’s guidance as a neutral to optimistic outlook, The Gap trades at an EV/NOPAT multiple of approximately 17x. In general, for a company that is growing (The Gap is not and has TAM constraints) and with a defensible business (The Gap operates in a very competitive market), I think a 15x multiple is fair. In this case, the company does not meet the requirements and has a higher multiple. After today’s rise, the company is among the most expensive of big-box retailers (based on our calculations above, The Gap has an EV/EBIT multiple for FY24 guidance of 12.6x).

Conclusion

The Gap delivered very good results in the first quarter of 2024. These results showed that the company’s turnaround strategy is working, and that its investments are paying off.

I like The Gap as a large, diverse clothing retail store. In particular, I like that the company focuses on intangible assets much more than direct competitors.

However, I also think the company’s valuation is a bit overvalued now, leaving little upside opportunity and more risk if it fails to deliver growth or higher margins over time. For this reason, I believe that The Gap stock is not an opportunity at this point and is a hold.