RHJ

introduction

the Cameco Company (New York Stock Exchange: CCJ) (TSX:CCO:CA) has become a gift that keeps on giving.

I started covering this Canadian uranium mine in November 2022. Since then, I’ve written five Bullish articles, the most recent of which was Titled “The Golden Age of Uranium: Positioning with Kamiko” On February 14th.

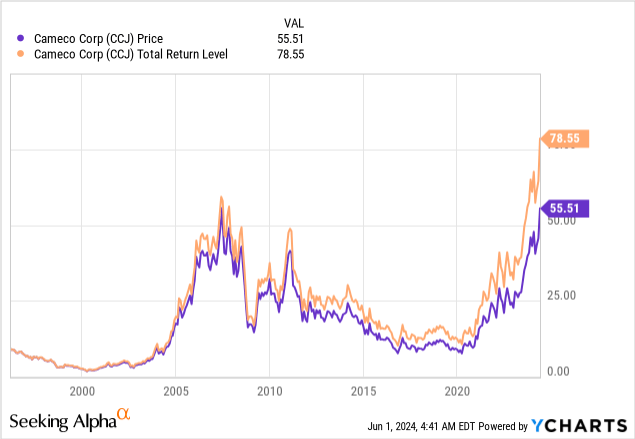

Since then, shares have risen another 32%, giving the company a market value of more than $24 billion. Over the past 12 months, shares are up 99%.

Even excluding dividends, New York-listed stocks are now back to their all-time high of July 2007.

As it turns out, the bull case for uranium is getting stronger, fueled by ongoing supply issues, geopolitical decisions, and the continued acceleration of artificial intelligence applications that will require a lot of additional energy.

In this article, we’ll discuss all of this as I update my CCJ Taurus case.

So lets get to it!

The uranium bull market continues

On May 26, The Atlantic wrote an interesting article about the return of nuclear power to the United States.

Essentially, the United States may not have a choice if it wants to push for 2050 climate goals, as “conventional” renewables in their own right.It will almost certainly not be enough.“

Another issue is land and resource use.

According to the article, nuclear energy can generate the same amount of energy as solar and wind energy using 1/30 of the Earth.

Better yet, nuclear reactors can be built everywhere, no matter how bright the sun or how strong the wind.

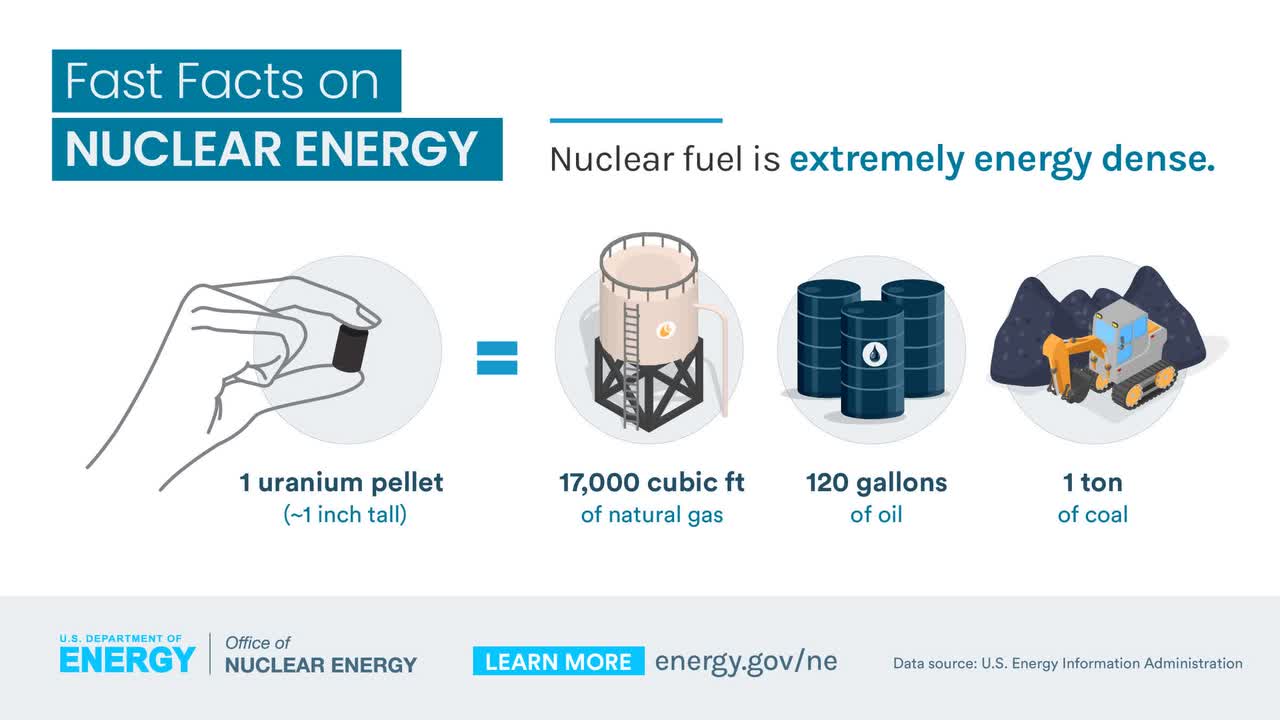

In my previous Cameco article, I highlighted these benefits as well, explaining that one small grain of uranium produces the equivalent energy of one ton of coal, 120 gallons of oil, and 17,000 cubic feet of natural gas.

Energy Information Administration

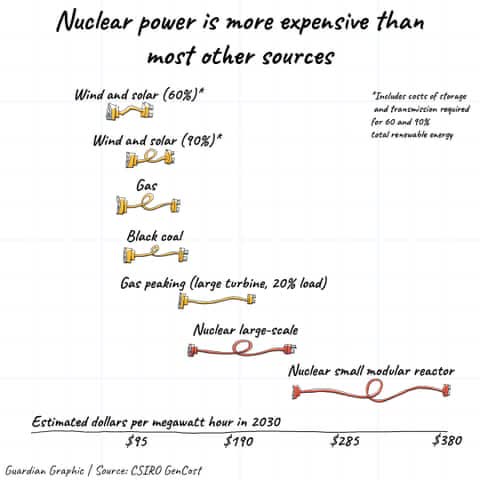

The problem is that nuclear power is expensive, at least initially because of the high construction costs.

According to The Guardian, nuclear energy is more expensive than renewables, gas and coal. This includes storage and transportation expenses needed to support renewable energy.

Watchman

The good news is that targeted government spending and creativity make nuclear power more attractive.

Back to the Atlantic:

The president signed the climate bill, Inflation reduction lawGenerous tax breaks included It could reduce the cost of the nuclear project by 30 to 50 percentand the Bipartisan Infrastructure Act It included $2.5 billion To finance the construction of two new reactors using original designs. Meanwhile, the Department of Energy is exploring various options for permanent storage of nuclear waste. Investing in building a local uranium supply chainAnd helping companies pass the process of obtaining approval for reactor designs. -Atlantic Ocean (emphasis added)

In other words, the United States is getting serious about nuclear energy, which couldn’t come at a better time, with energy requirements increasing dramatically!

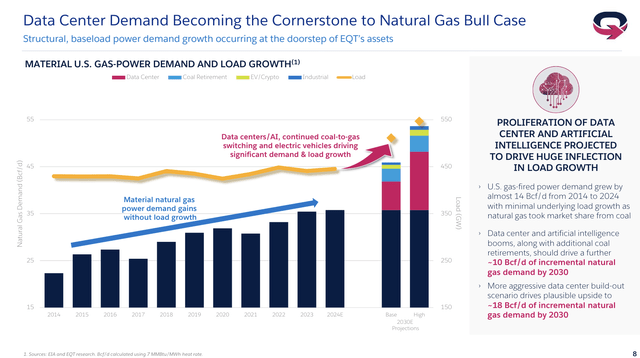

On May 28, I wrote an article focusing on the natural gas bull trend, which is being fueled by the AI boom.

- Between 2014 and 2024, demand for gas-fired power rose by about 14 billion cubic feet per day, with almost no baseload growth, primarily dependent on the shift from coal to natural gas.

- AI alone could drive another 10 Bcf of increased demand by 2030!

- The most optimistic estimates point to growth of 18 billion cubic feet per day by 2030 – from AI alone…

EQT Company

However, in addition to strong demand, supply is under pressure.

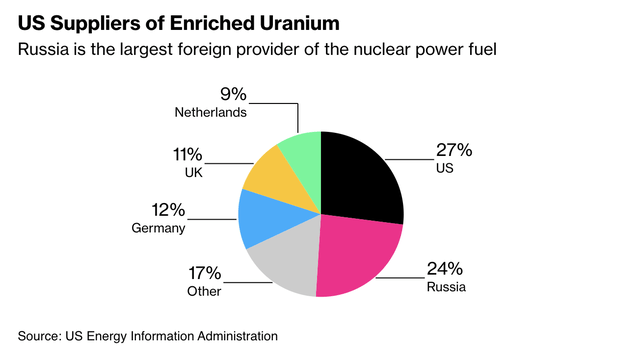

On May 16, it was reported that President Biden signed legislation to ban the import of enriched uranium from Russia.

This is important, because Russia is America’s largest foreign source of uranium, supplying about a quarter of the uranium to its reactors.

Cutting that supply could raise uranium prices by 20%, according to Jonathan Haines, president of nuclear fuel market research firm UxC. – Bloomberg

Bloomberg

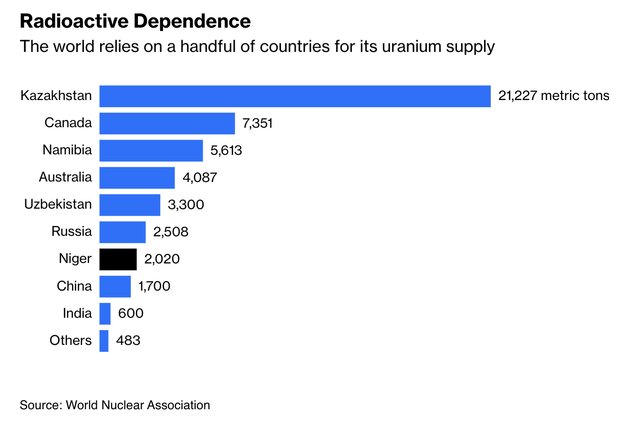

Now, the possibility is increasing that Russia will use its influence to pressure Western nuclear energy in general.

After all, global supply depends heavily on countries like Kazakhstan, which has strong ties with Russia.

Bloomberg

All of this bodes well for uranium prices and supplies from Western producers.

This is where Cameco comes into play.

Cameco continues to fire on all cylinders

Cameco is one of those companies that is in the right place at the right time with the right product.

As supply risks arise from production challenges and increasing geopolitical uncertainty, utilities are evaluating their nuclear fuel supply chains. As a trusted commercial supplier with nuclear fuel assets in geopolitically stable jurisdictions, we focus on working with our customers to secure long-term commitments that will support the long-term operation of our production capacity, while helping to eliminate their nuclear risks. Fuel supply chains. – Kamiko (emphasis added)

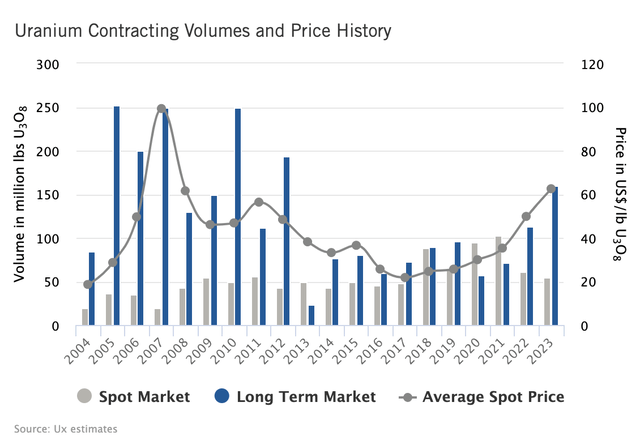

Using the Cameco data below, we see that U3O8 prices nearly tripled between 2017 and 2023 when uranium trioxide (a compound of uranium) prices jumped from $20 to $60.

Cameco Company

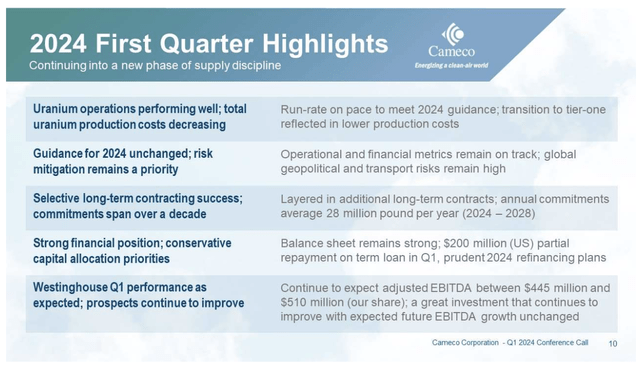

In its Q1 2024 earnings call, the company reiterated what we discussed in the first part of this article, noting that demand for nuclear power is increasing as governments, energy suppliers and industrial consumers recognize it as an important part of the ongoing energy transition.

The miner also noted that national security is a growing driver of growth, as reliance on uranium supplies from unreliable partners could hurt the energy transition.

The war in Ukraine is a good example of this.

- Russia cut off most natural gas exports to Europe in the early stages of the war.

- Sanctions hurt uranium supplies from Russia.

- Russia could retaliate by pressuring partner countries to reduce uranium exports.

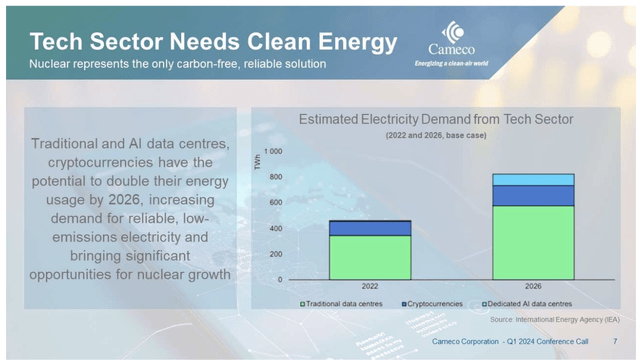

Furthermore, you made an interesting comment regarding artificial intelligence. Not only is AI in general boosting demand for electricity, but it is also causing technology companies to become interested in nuclear energy.

According to Kamiko, some companies are already working to secure agreements to ensure their facilities have access to nuclear energy.

Technology companies and Silicon Valley billionaires have been pouring money into nuclear power for years, arguing that a sustainable energy source is crucial to the green transition. Now they have another incentive to promote: artificial intelligence.

(…) “Basically today in the world, the two limited goods that you see everywhere are intelligence, which we’re trying to work on using AI, and energy,” he told CNBC in 2021 after investing $375 million in Helion Energy. A nuclear fusion startup headed by Altman. Microsoft agreed last year to buy energy from Helion starting in 2028. Oklo, which Altman also heads, focuses on the opposite reaction, fission, which generates energy by splitting an atom; This is done by merging atomic nuclei. -NBC News

I think the interest of technology giants and pioneers in nuclear energy is misunderstood, because these people know exactly how demanding their AI applications are for energy demand and how efficient nuclear energy is.

It is also reliable, which cannot be said about wind and solar energy.

If there’s one thing modern technology applications (or the economy in general) need, it’s reliable, affordable power!

Cameco Company

With that in mind, it helps that Cameco is so reliable and efficient when it comes to uranium production.

During the earnings call, the company noted that 1Q24 results were strong and in line with its annual guidance, supported by the successful transition to Tier 1 cost structures.

So we find it very constructive, given that the average term price is at $77.50 while we haven’t even gotten to the replacement rate yet, that’s a good place for us to be a great place for the current level product. 1 assets and leverage, a great opportunity for us to leverage that value. So we feel very constructive on the underlying market fundamentals. – CCJ 1Q24 earnings call

Overall, the company’s strategy is primarily focused on securing long-term contracts rather than tinkering in the more volatile spot market.

Cameco Company

According to the company, this trend has led to a significant increase in annual commitments, averaging about 28 million pounds annually from 2024 to 2028.

In addition, the company’s investment in Westinghouse is paying off.

Last year, Cameco bought a 49% stake in Westinghouse. Brookfield Asset Management bought 51%.

This has allowed Cameco to capitalize on the growing demand for nuclear power as well as Westinghouse’s nuclear plant technologies, products and services.

The company still expects its share of adjusted EBITDA from Westinghouse to be between $445 million and $510 million this year.

Even better, this sector is expected to grow at a CAGR of 6% to 10% over the next five years!

evaluation

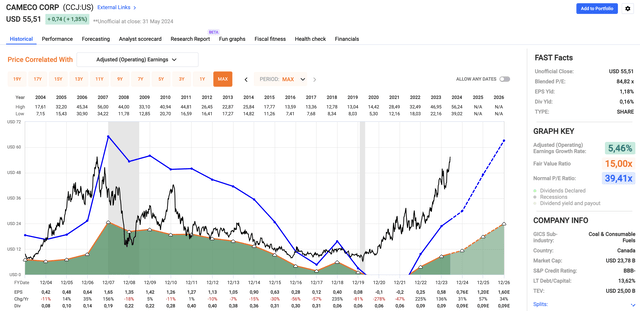

New York-listed CCJ shares are up 29% year to date. Performance for 12 months is 99%.

As a result, CCJ now trades at a blended P/E ratio of 84.8x, which is well above its normal long-term P/E ratio of 39.4x – using the FactSet data in the chart below.

Quick charts

However, the situation is less bad than one might think.

Using the same FactSet data in the chart above again, analysts expect 31% growth in EPS this year, likely followed by 57% and 34% growth in 2025 and 2026, respectively.

While these numbers are subject to change, I expect the company to enjoy double-digit annual growth for a long time.

However, applying a 39x multiple to these numbers, we get a fair share price of $62, which is 12% higher than the current price.

While I will keep He buys Rating, I can’t confirm that the risk/reward is great.

The long-term bull case certainly remains impressive, and I’m sure investors will be willing to pay a premium for that to change.

However, I would not invest aggressively at these levels.

If I was looking for exposure to CCJ, I would buy gradually. If the stock corrects, investors could decline on average. If the stock continues to fly, investors will have a foot in the door.

Regarding my situation, as I wrote in my previous article, I invested in Caterpillar (CAT) to cover mining-related demand. Given strong investments in energy and related stocks, I have not yet expanded my commodity-focused exposure.

Away

Cameco continues to prove its value, with its shares up 32% since my last article.

The uranium market is booming, driven by supply constraints, geopolitical shifts, and increasing energy demand through artificial intelligence applications.

It goes without saying that the return of nuclear power, supported by government support and interest from the technology industry, bodes well for Cameco.

Despite the high P/E ratio, the strong earnings growth outlook justifies the bullish outlook.

However, cautious and gradual investments may be the best solution, given the current valuation.

The bottom line is that Cameco remains a major player in the energy transition, offering reliable and efficient uranium production.

Pros and Cons

Positives:

- Uranium market strength: CCJ benefits from a strong uranium market, driven by supply constraints and high demand from nuclear power.

- Geopolitical support: With geopolitical tensions impacting uranium supplies, CCJ benefits as a reliable commercial supplier.

- Technology industry interest: The growing interest of technology giants in nuclear energy supports its importance in meeting energy requirements.

- Earnings Growth Potential: Analysts expect strong earnings growth for CCJ, which supports its current valuation.

- diversification: Acquiring Westinghouse was a smart move to differentiate the business.

cons:

- High rating: CCJ’s current P/E ratio is well above the normal long-term ratio, meaning negative headlines could hurt its stock price.

- Market volatility: Like the uranium market, CCJ’s stock price is volatile.

- Uncertain regulatory environment: Regulatory changes or shifts in government policies related to nuclear energy can impact CCJ operations and evaluation.