josefkubes

For many years, HP Inc. (New York Stock Exchange: HPQ), the hardware segment of the formerly consolidated HP which has since been split into HP Inc. And HP Enterprise (HPE), a forgotten stock. Investors avoided the company because of it Slow growth, lagging results in PCs, and a long-term decline in the printing business, HP’s cash cow.

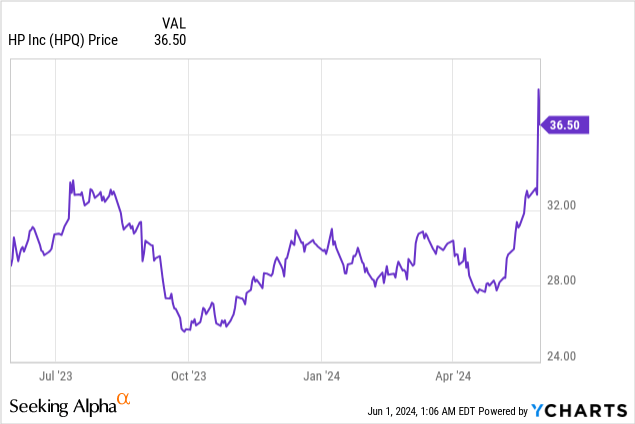

Moving forward to this year, that story may no longer be true. HP enjoyed one of its best one-day gains in recent memory after reporting very strong Q2 results and citing tailwinds from artificial intelligence, pushing the stock’s year-to-date gains above 20% immediately. Despite this rally, I think there is still a lot of upside.

Myriad growth stimulants against the backdrop of muted evaluation

I last wrote a bullish note on HP in April, when… The stock was still trading in the high $29 range. Now, despite my ~25% gain since then, I’m still flat rising About HP’s outlook for the remainder of the year.

In short: The company appears poised to get back into growth mode again. Investors typically view HP as an old technology company waiting out its printing business. And yes, this is probably the ultimate reality: with remote work, distributed/hybrid teams, as well as environmental awareness – we don’t print things the way we used to. But in the second quarter, HP gave us hope The surprising strength in the personal computer market may reduce the company’s historical reliance on its printing business to deliver results.

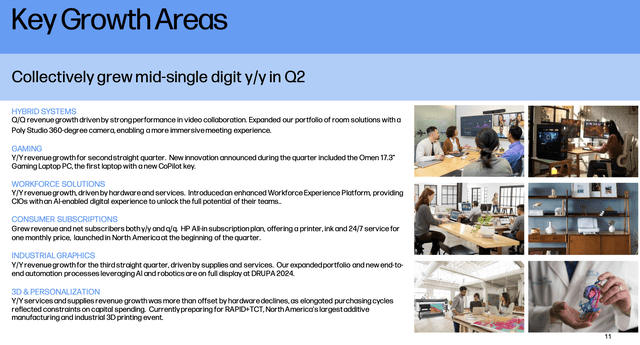

Although revenue was down -1% year-over-year in Q2 (we’ll review the latest results in the next section), the company noted a number of areas where the company is growing its revenue by mid/high single digits:

HP growth areas (HP Inc. Q2 Shareholder Group)

Gaming, print subscriptions, and enterprise office devices are the highlights here. But above all, the company notes that demand for AI — from consumers and enterprises alike — could lead to a “super cycle” of PC refreshes that will benefit HP this year and next.

Here’s my full long-term case for HP:

- A wide variety of products, especially in the field of computers. HP manufactures a number of products across the desktop and laptop space. It has a rich enterprise business and has products across a wide range of price points. This long-standing reputation for quality among different customer segments makes HP a solid brand.

- High-margin printing business; New subscription form. While it’s certainly no longer growing, it’s worth noting that HP has a very high marginal stream of recurring revenue from its printing supplies business. The company’s new print subscription offering may help reduce customer traffic in this area.

- Strong shareholder return programs and consistent cash flow. HP has long been a “cash cow” that has been active in returning capital to shareholders through buybacks and dividends. HP’s dividend yield is competitive even in today’s high interest rate environment, making it a solid stock to hold as it seeks to re-evaluate its P/E multiple.

Stay here for the long haul and stick with HP’s post-earnings results.

Download Q2

Let’s now review HP’s latest quarterly results in more detail. We’ll start with the bad news part first, where we print:

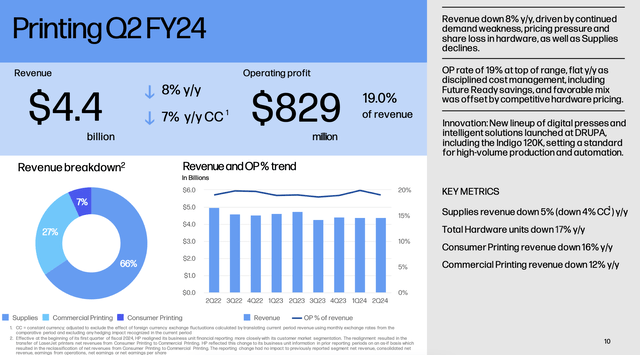

Print results for HP Inc (HP Inc. Q2 Shareholder Group)

Printing revenues of $4.4 billion declined -8% y/y (-7% y/y on a constant currency basis, as a stronger dollar remains a drag for HP). Unfortunately, this slowed by three points versus -5% y/y in the first quarter. Management cited weak demand in both Europe and China as the main driver. Also unfortunate is the fact that operating margins of 19.0% in this segment, while flat year over year, also declined by 90 basis points versus a margin of 19.9% in the first quarter.

Printing still provided two-thirds of the company’s consolidated operating profit in the second quarter. This is the main risk for HP: that this cash cow dries up and makes HP less profitable overall. However, we note that printing companies will start to become easier to print, and the company’s growth in print-as-a-service subscription offerings may help stem the bleeding. Ultimately, we’re not counting on HP being able to get its printing business back into growth mode: the best we can hope for here is a flat-rate business that can still deliver healthy operating profits quarter after quarter, and HP can run this business on autopilot As a subscription offering without investing a lot of extra expenses or R&D into it.

Despite the weakness in printing, HP’s management believes it has gained market share. According to CEO Enrique Lloris’ comments on the second quarter earnings call:

The pricing environment remains consumer competitive as trade pressure intensifies. We continued to make progress on pricing and share supply gains with revenue results as expected. We achieved a printing operating profit of 19%, in line with our guidance.

We have once again demonstrated disciplined cost management, improved mix and the benefits of the strong innovations we have brought to the market. Our focus in the printing business remains on regaining profitable share and we are making progress.

We’ve increased quarterly share in home and office. More importantly, we gained share year over year and sequentially in large tanks and commercial ink. We have also achieved growth in key growth areas such as consumer services. We have seen growth in revenue and subscriber numbers through Instant Ink and our new comprehensive plans.”

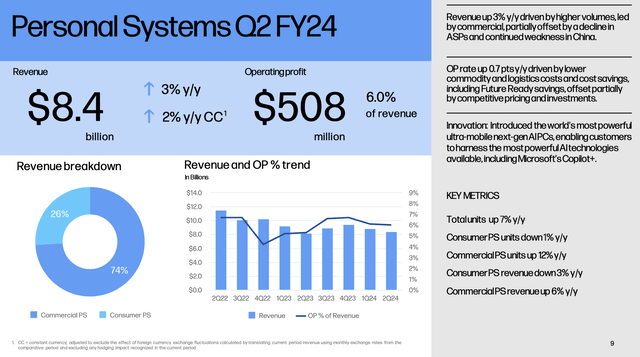

However, on the personal systems/PC side of the business, we have seen very positive news Personal Systems returned to 3% year-over-year revenue growth, Compared to a decrease of -4% on an annual basis in the first quarter.

PC results for HP Inc (HP Inc. Q2 Shareholder Group)

The company noted a rebound in corporate demand as one of the key drivers here, which was partially offset by overall weakness in China. Also noteworthy is the fact that unit sales grew 7% year over year, also accelerating versus 5% growth in the first quarter. HP is flexing its ability to attract customers at all price points here.

The company also noted the successful launch of new AI-equipped PCs, including the latest high-end HP Omen offering. Furthermore, PC segment profitability increased, with operating margins of 6.0% up 60 basis points year over year driven by commodity costs and lower logistics/fulfillment expenses.

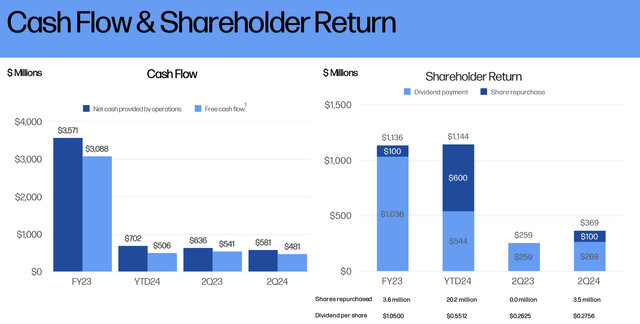

We also note that HP continues to generate strong cash flow, with free cash flow of $481 million this quarter at levels that are more than enough to cover the $309 million spent on dividends and buybacks during the quarter:

HP FCF (HP Inc. Q2 Shareholder Group)

Evaluation and main takeaways

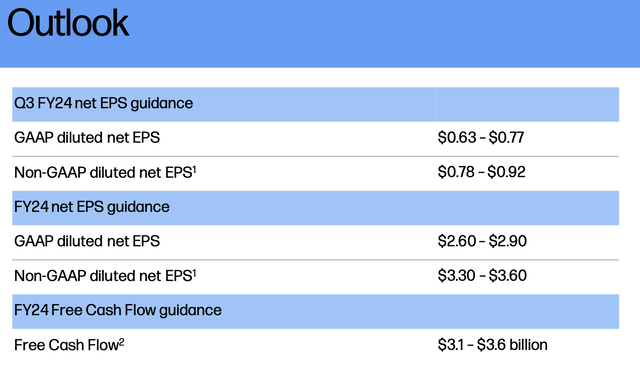

For the year, HP has tightened its earnings forecast to $3.30-$3.60 in EPS, from a previous wider range of $3.25-$3.65 that had the same midpoint of $3.45.

HP forecast (HP Q2 Shareholder Group)

We note that even at a post-earnings share price of around $36, HP is still trading at a very cheap price P/E ratio 10.4x. Given the growth drivers under HP’s hood from its AI PC refresh, as well as the attractive 3% yield the stock has right now, I’d say investors still have plenty of incentive to dive in.