Bixora/iStock via Getty Images

introduction

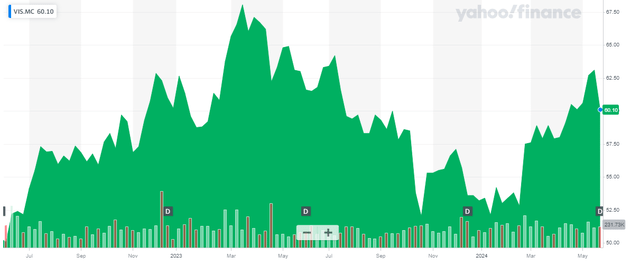

It’s been several years since I last looked at Viscofan ( OTC:VSCFF ), the Spanish company and leading producer of meat product packaging. As the demand for Viscovan products is relatively high High and stable, the company is trading at an excellent valuation, and in this article I wanted to take a closer look at whether or not it makes sense to start a long position in the Spanish company as I was not optimistic in 2019. The stock price is currently up about 40% over the five-year period past.

Yahoo Finance

Viscofan is a Spanish company and its most liquid listing is in Madrid where the ticker symbol is VIS, and the average daily volume is around 46,000 shares. The current market capitalization is approximately 2.75 billion euros. I will use the euro as the base currency throughout this article.

Look to 2023 – tax benefits saved the day

Before discussing the recently published Q1 results, I wanted to take a look at the company’s financial results in 2023 as that will provide greater context and a platform for the company to build upon.

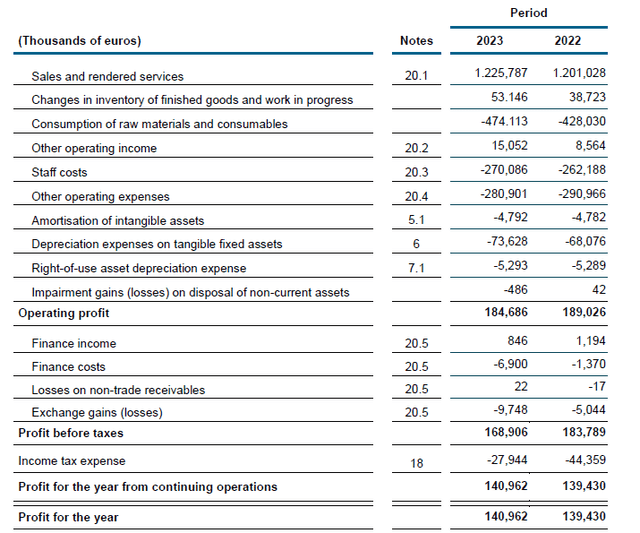

Total revenues in 2023 amounted to EUR 1.23 billion, an increase of approximately 2% compared to EUR 1.2 billion in 2022, while there was a further improvement of EUR 14.4 million in the value of inventory of finished goods and work in progress. Unfortunately, the income statement clearly shows that cost of goods sold increased by €46 million while employee costs increased by 3% or approximately €8 million as well. While some other operating expenses decreased, this was not enough for Viscofan to report an increase in its operating profit.

Vescovan Investor Relations

Furthermore, Viscofan’s financing expenses also increased, and as the income statement above shows, net financing expenses rose from EUR 0.2 million to approximately EUR 6 million. This is somewhat surprising given that the company has a very good cash position and we hope that Viscofan can keep its net financial expenses within a reasonable range in the future.

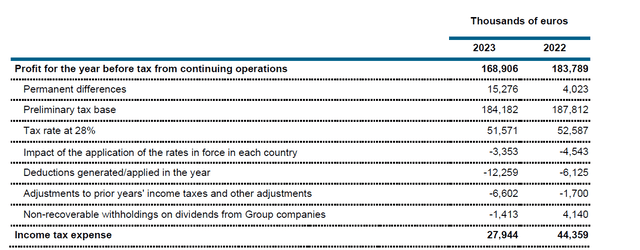

Pre-tax income fell by approximately 8%, but fortunately the Spanish company received a much lower tax bill allowing it to record a 1% higher net profit of approximately €141 million, which works out to €3.05 per share. As the image below shows, the company was able to obtain higher deductions while the adjustment to the previous year’s income tax increased by approximately 5 million euros. This reduced overall tax pressure, resulting in an average tax rate of 16.5% compared to 24% in FY2022.

Vescovan Investor Relations

Readers are cautioned that the reduced amount of income taxes will likely be a one-time item and the total tax pressure will continue to fluctuate slightly.

In the previous article I was also focusing on Viscofan’s cash flow performance because this is what will ultimately allow the company to invest in additional growth.

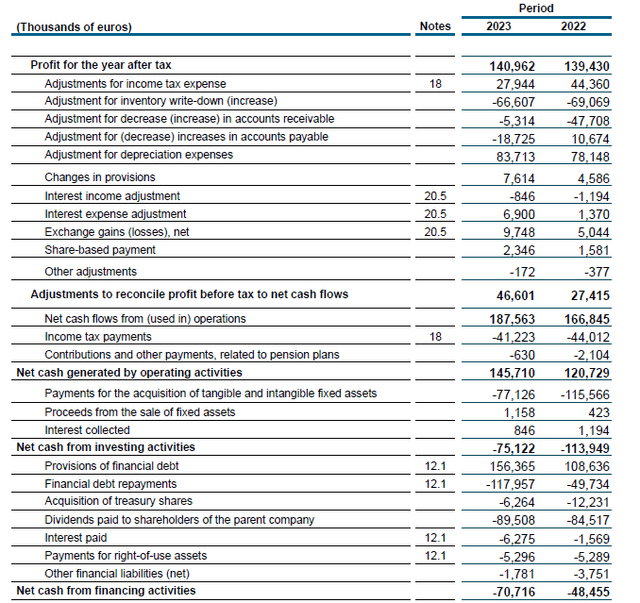

Looking at the cash flow statement for 2024, Viscofan reported a total operating cash flow of around €146 million, but this includes an investment of €86 million in working capital position while also including the payment of taxes of €41.2 million although the €28 million Only euros were due based on the 2023 income statement On the other hand, we must also deduct 6.3 million euros from interest payments and 5.3 million euros from lease payments. This results in an adjusted operating cash flow of approximately €239 million after interest income is added to the cash pile.

Vescovan Investor Relations

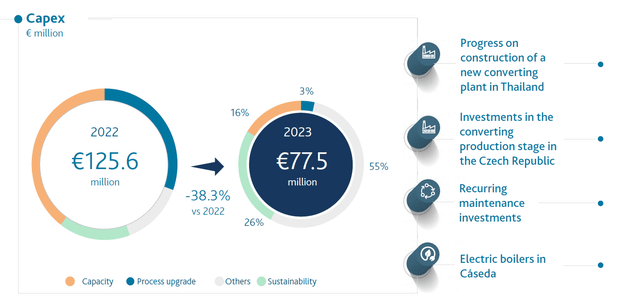

Total capital expenditures amounted to approximately €77 million, resulting in an underlying free cash flow result of approximately €162 million. The split of over 46.2 million shares results in free cash flow of approximately €3.5 per share.

As the image below shows, approximately 16% of total capital expenditure was spent on capacity expansion; This is approximately €12.5 million which means underlying sustainable free cash flow increases by approximately 27 cents per share (at €3.77 per share).

Vescovan Investor Relations

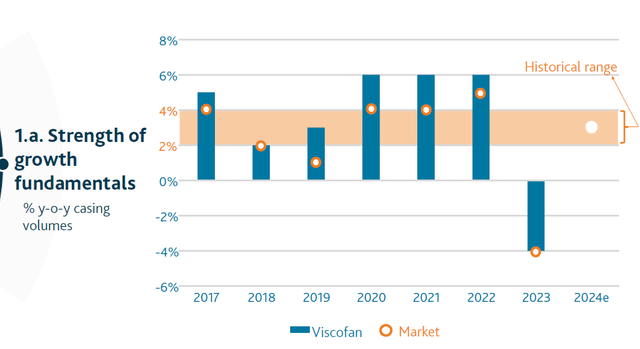

The capacity expansion comes at an opportune time, as the company expects the packaging market to return to growth after contracting by 4% in 2023.

Vescovan Investor Relations

2024 has started slow, but the goals for the entire year have remained the same

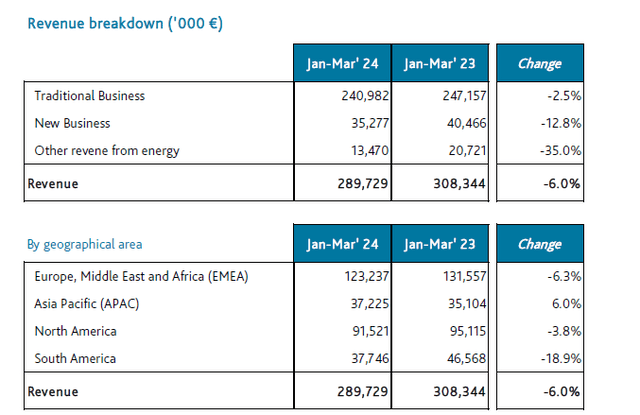

Although the company reported a 6% decline in revenue in the first quarter of the current fiscal year, it is important to realize that a large portion of the revenue decline is related to lower energy sales. In fiscal 2023, approximately 7% of Viscofan’s revenue was generated from the sale of electric power from its cogeneration facility (which generates more power than Viscofan needs). As the image below shows, approximately 40% of the difference in revenue was due to lower revenue from energy sales, while the traditional business shrank by “only” 2.5%.

Vescovan Investor Relations

Net income in the first quarter of 2024 was just €31.6 million, or just 68 cents per share. This is certainly a little lower than I expected, but the company reiterated its guidance for the full year.

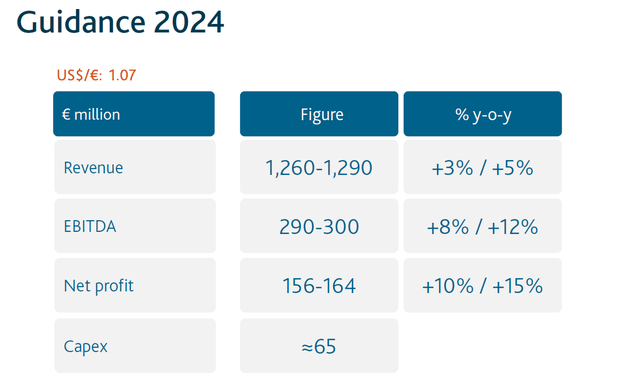

For the current fiscal year, Viscofan expects total revenues of around €1.275 billion and EBITDA of €290-300 million. This should result in a net profit of around €160 million (midpoint of €156-164 million guidance).

Vescovan Investor Relations

I’m also pleased to see the lower capex guidance as this is well below depreciation and amortisation, although it still includes some growth investments as Viscovan is currently building a new cellulose and collagen film conversion plant in Thailand which should begin operations by 2018 End of this year.

We know that the total amount of depreciation is about 84 million euros per year. Assuming a fixed lease payment schedule of €5 million per year and using capex guidance of €65 million, net free cash flow would be approximately €14 million higher than reported net income.

Investment thesis

This means that based on current guidance for fiscal year 2024, Viscofan will report earnings per share of around €3.45 per share while its net free cash flow result should be €3.75 per share. Assuming approximately €10 million of full-year capex will be spent on growth initiatives such as the new factory in Thailand, the sustainable free cash flow result is likely to be higher by 21-22 cents per share and closer to €4 per share.

At the current share price of around €60, Viscofan trades at around 17 times its expected net earnings, while its sustainable free cash flow yield is around 6%. Looking at the EV/EBITDA multiple, Viscofan currently trades at around 10 times expected EBITDA for the year. Fellow author Gold Panda identifies Viskase ( OTCPK:VKSC ) as a competitor to Viscofan, but given its extremely low market cap and lack of scale, I’d rather stick with the larger company in this space.

The new factory in Thailand should have a positive impact on Viscofan’s results in 2025, and analyst estimates call for an EBITDA increase of 8% which is likely to boost the sustainable free cash flow result to above €4 per share.

Viscofan has a pretty boring business model, but its performance is largely consistent and lower volumes in 2023 are likely just a temporary bump as the company expects the packaging market to return to its historical growth rate of 2-4% per year.

I currently have no position in Viscofan but might be interested in a long position on weakness.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.