Luca Lorenzelli

JustEat overview and investment thesis

JustEat is an online food delivery marketplace that operates across four markets, which can be segmented into:

-

Northern Europe, UK and Ireland: JustEat is one of the largest companies in these markets With a clear path to profitability. This is where they will direct most of their investments.

-

North America: JustEat has been reducing its investments and prioritizing profitability in this market due to intense competition, although it has a strong foothold through its acquisition of GrubHub in 2020. Currently, the company is exploring the possibility of a partial or complete sale of Grubhub.

-

Southern Europe and ANZ (Australia and New Zealand): JustEat is also reducing its investments in these markets where it has not yet been able to significantly establish its presence. These markets represent only a relatively small portion of its total gross sales. As of 1Q24, they are It closed its operations in New Zealand.

Management has made significant efforts to downsize its operations to focus on markets where it has a stronger presence and shows a clear path to profitability. This has led to improvements in total EBITDA and operating cash flow as they move toward sustainable, profitable growth. In my opinion, their decisions were correct in reducing their losses in markets where they do not have strong competitive positions. Furthermore, I think they spread too thin in the past. However, I still have concerns about the management’s ability to re-accelerate growth in Northern Europe and the UK/Ireland, which I will delve into later. As of now, I classify the company as a held company.

Discussing the results of the first quarter of 2024

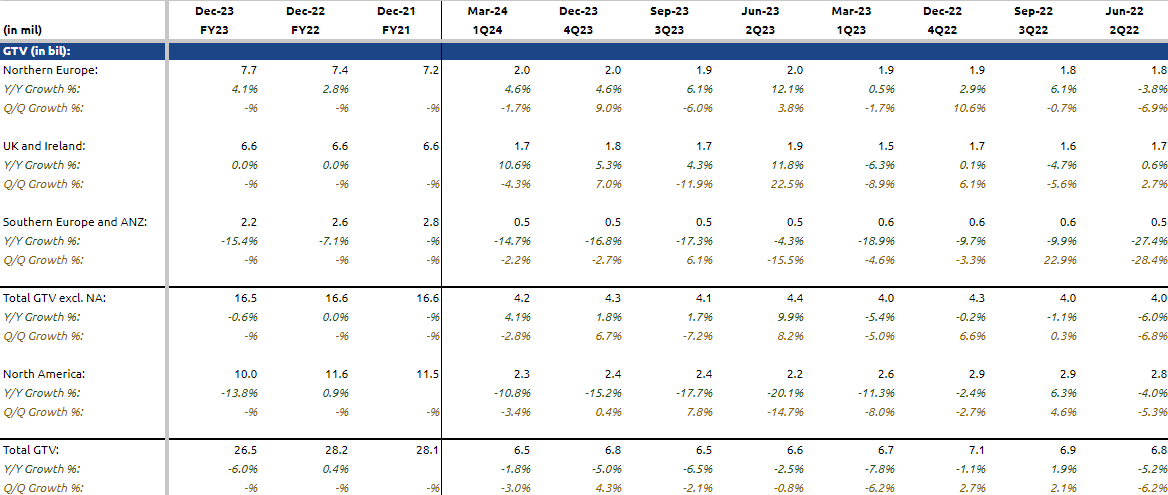

GTV growth by markets Growth ranking by markets

In 1Q24, total TSR revenue, excluding North America, grew 4.1% year over year to $4.2 billion, representing the fifth consecutive quarter of year over year growth since 1Q23. Growth was primarily driven by growth of 4.6% and 10.6% in Northern Europe, the UK and Ireland respectively, partially offset by a decline of 14.7% year-on-year in Southern Europe and ANZ (Australia and New Zealand).

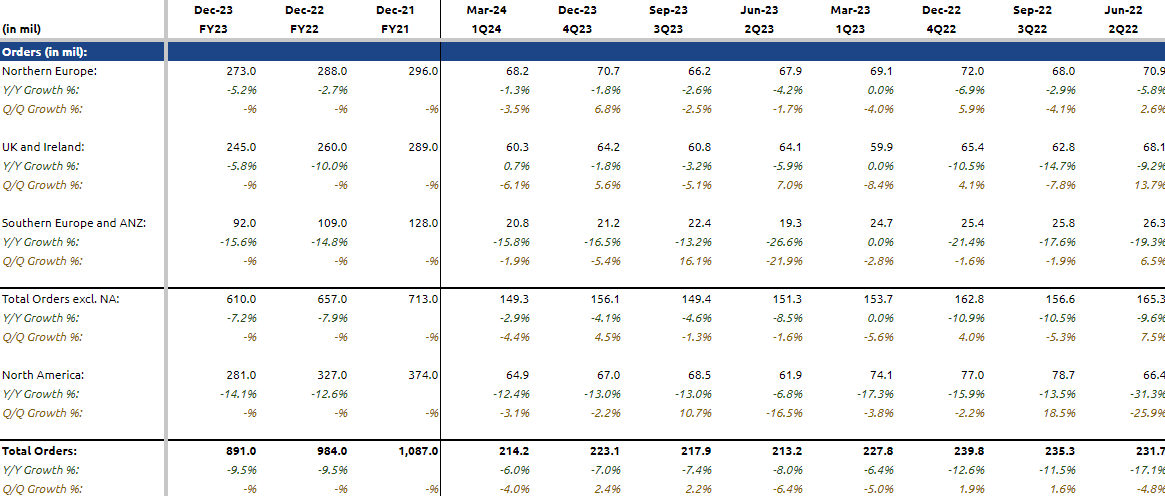

Based on its Q1 2024 earnings call, growth in these markets was driven by JustEat’s UK grocery business, which is currently rolling out to existing customers, and price hikes implemented by merchants to offset rising inflation. This resulted in higher revenues for the company, which was offset by lower growth in Southern Europe and ANZ as they reduced their investments. It was not revealed whether there was a recovery in growth in the core restaurant business. But if we observe the results of the first quarter of 2024, the growth of orders in Northern Europe decreased by 1.3% year-on-year, and growth in the United Kingdom and Ireland increased by 0.7% year-on-year.

Given that restaurant is its core business, this means that the majority of GTV’s gains in Northern Europe were driven by higher prices. Meanwhile, for the UK and Ireland, there may be a slight rebound in demand growth from the restaurant business. From my perspective, this is a concern as I would have preferred to see growth driven by orders as this would lead to more sustainable growth in the long term, and this also demonstrates its ability to attract more consumers to its platform. This is something to watch for investors.

Meanwhile, the decline in GTV’s growth in Southern Europe and ANZ is due to their lower investments and the closure of their operations in New Zealand. Management explained during the first quarter 2024 earnings call that New Zealand is a very small market, and since it does not have a strong presence, it does not make sense to continue operating the business. As a result, they made a conscious decision to put profitability first and reduce cash burn, resulting in lower TSR growth. JustEat has a significant presence in Australia and will continue to operate there. But overall, management attributed the overall market decline to lower investments, citing its efforts to focus on markets in Northern Europe, the UK and Ireland, where they are more established.

Turning to North America, growth continues to decline as total gross loans fell 10.8% year over year to $2.3 billion, marking the sixth consecutive quarter of declining growth. Likewise, management has deliberately reduced its investments. To understand this logic, competition is fierce in the US with prominent players such as DoorDash (DASH) and Ubereats (UBER), which hold 67% and 23% of the US market share, respectively, while Grubhub (JustEat’s US food delivery platform) has taken over. in 2020) owns only a meager 8% (plus, if you’re interested, I also covered DoorDash extensively in my last article). Like any other industry, companies with a dominant market share tend to engage in a winner-take-all market. It is very difficult for Grubhub to compete and replicate DoorDash’s delivery infrastructure, scale, network effects, and brand recognition. Furthermore, Grubhub is losing market share to DoorDash as well. Therefore, management has stepped back from this market, focusing instead on directing its resources to areas where it has a stronger foothold and shows a clear path to profitability. Additionally, management planned to withdraw from the market as it is currently exploring a partial or fall sale of Grubhub.

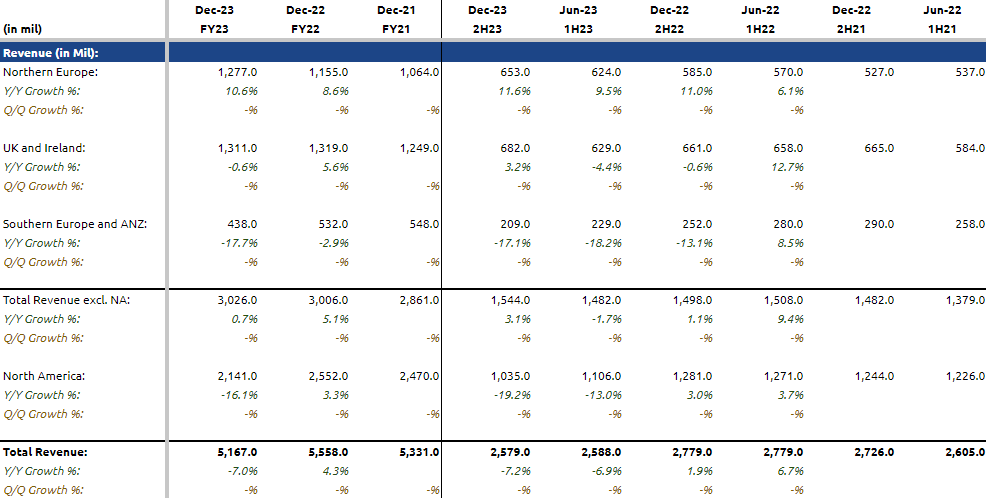

Total revenue

Note that the company only announces its annual and semi-annual financial statements.

As of its latest H2 2023 results, its total revenue, excluding North America, rose 3.1% to $1.5 billion. Likewise, this was driven by 11.6% year-on-year and 3.2% year-on-year growth in Northern Europe, the UK and Ireland, respectively, which has been compensated. 17% YoY decline in Southern Europe and ANZ. Its revenues in North America fell by 19.2% year over year to $1.03 billion. For fiscal 2023, total revenues, excluding North America, increased only 0.3% year over year, and North America revenues decreased 16% year over year.

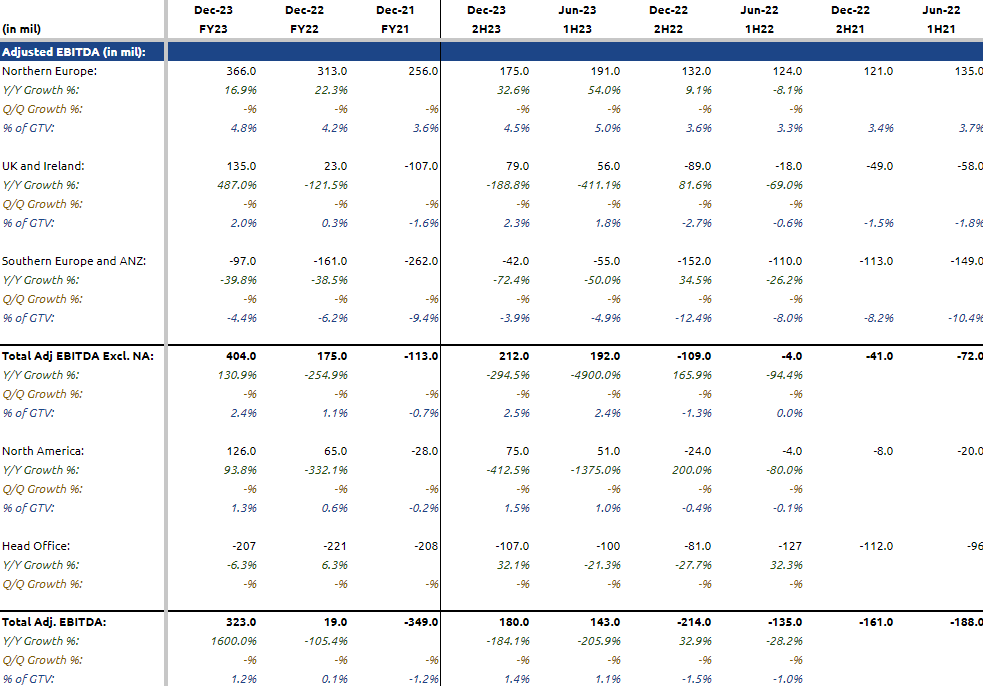

Adjusted EBITDA

Turning to adjusted EBITDA, on a full-year basis, total EBITDA, excluding North America, rose 130% year-over-year to $404 million, and EBITDA margin was EBITDA (% of total total) 2.4% compared to 1.1% in FY22 and -0.7%. In FY21. This was primarily driven by improvements in regions, most notably the UK and Ireland, which increased EBITDA by 487% YoY, followed by improvement in Northern Europe (+16.9% YoY) and Southern Europe. Europe and ANZ (+39.8% y/y). ). Meanwhile, North America EBITDA rose 94% year over year to $126 million, and EBITDA margin is 1.3%, compared to 0.6% last quarter.

Due to reduced investments in Southern Europe, Australia and North America, and the closure of its operations in New Zealand, total adjusted EBITDA, including North America, improved significantly by 1,600% year-on-year, and gross EBITDA margin increased The rate goes from 0.1% in FY22 to 1.2% from FY2023.

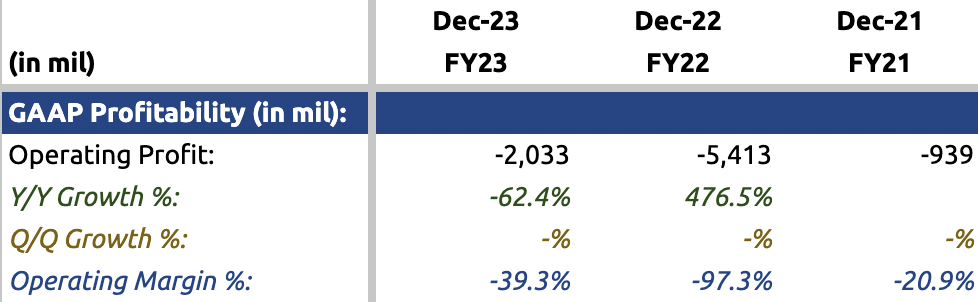

Profitability

However, in terms of GAAP profitability, the company’s operating margin for FY23 is still at negative 39.3%, and there is still a long way to go to achieve profitability.

I have the impression that management has spread itself too thin in the past by operating in too many markets at the same time, and that it lacks the experience necessary to compete with its competitors. Ultimately, this strategy backfired as the competition was so intense, it was not profitable to keep going. Additionally, while the presence of EBITDA makes it easier for management to attract buyers for its Grubhub business, there may be other factors that may hinder a sale, which include the value of the stock market as a whole, and buyers’ concerns about whether Competition in the US also makes it difficult for management to sell the company at a fair multiple because that could raise more questions about Grubhub’s ability to deliver profitable growth over the long term.

Balance sheet and operating cash flow

Net debt Foldable belts Foldable belts

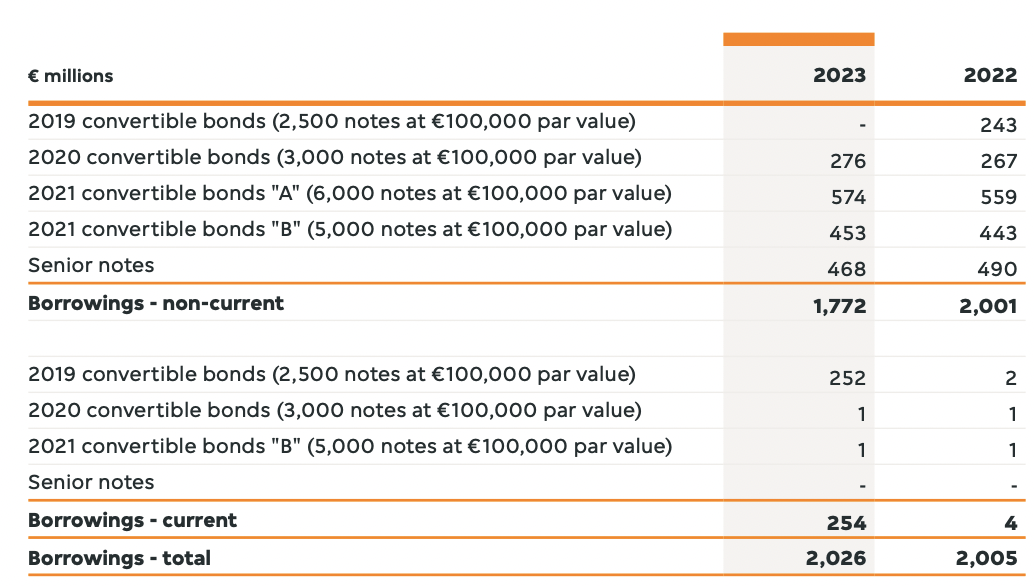

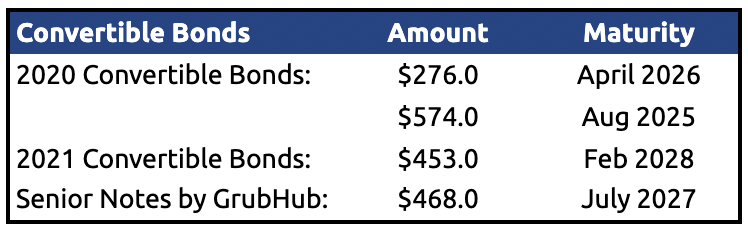

While JustEat is currently unprofitable, assessing whether they have a strong balance sheet is important. As of fiscal 2023, the company has total debt of $2.36 billion, including convertible notes and lease obligations, and total cash of $1.72 billion, resulting in net debt of $705 million. According to its FY23 annual report, $254 million of the 2019 convertible notes have already been repaid in cash in January 2024, with the next payment of $574 million due in August 2025, which the company has sufficient funds to repay.

Free cash flow Operating cash flow

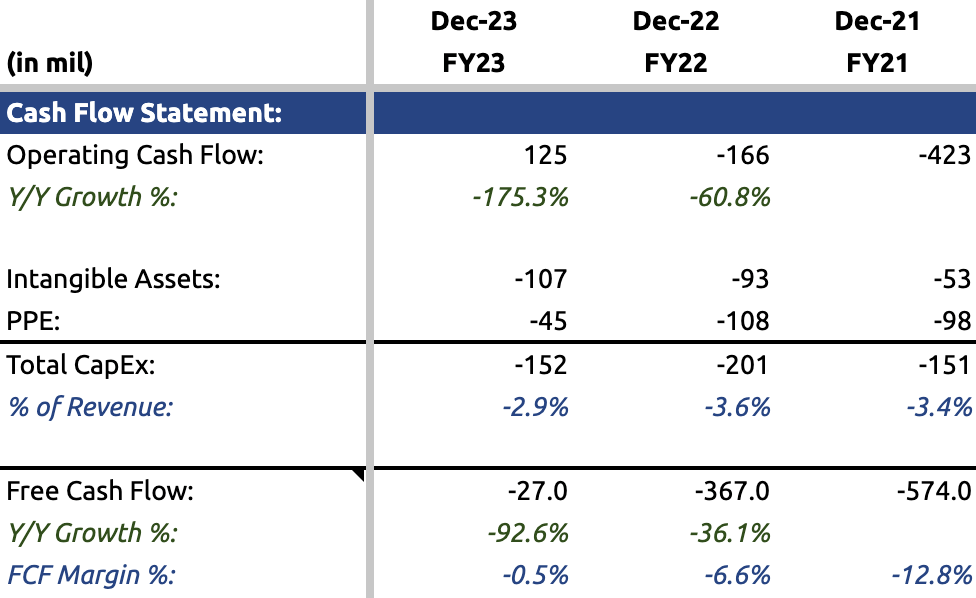

As of fiscal 2023, its free cash flow margin is negative 0.5%, and is slowly approaching a positive free cash flow margin. This was primarily driven by improvements in profitability, as well as lower depreciation and amortization (D&A) and impairment losses, consisting of $599 million of D&A ($567 million in FY22) and $1.5 billion of impairment losses. Value (versus $4 billion in FY2022). Fiscal year 22). This impairment loss resulted from lower expected demand growth and increased market competitiveness, reducing future expected cash flow across its markets, therefore, resulting in a significant impairment loss. I expect lower D&A and impairment, and with the continued improvement in net loss, I believe achieving a positive FCF margin will not be an issue.

evaluation

Peer evaluation

To assess JustEat’s valuation, I compiled a list of competitors operating in a similar industry, namely Doordash, Uber, and Grab. In my opinion, I find it difficult to find a list of similar companies since their peers like Uber and Grab operate in multiple industries, including the ride-hailing and food delivery industry. In addition, I could also try using the restaurant industry average multiple of 1.22x, but this would be inappropriate given the different business models. Hence, I will use DoorDash, Uber, and Grab to conduct my comparative competitive analysis.

At a current EV/sales of 0.6x, JustEat is trading at a significant discount to its peers. In my opinion, the market has probably factored in several risks: (1) in terms of profitability, it has the lowest negative EBIT margin at 39.3%, and there is still a long way to go to achieve GAAP profitability, (2) Uncertainty about management’s ability to re-accelerate its growth in its restaurant businesses in Northern Europe, the UK and Ireland, given the majority of its growth is driven by rising prices and the UK grocery business, and (3) competitors such as Grab and DoorDash have demonstrated clear market leadership, offering their More robust in terms of re-accelerating growth, taking market share away from competitors, and profitability. Therefore, Grab and DoorDash may make a better investment in the long term. In my opinion, I think JustEat’s low rating is justified.

Conclusion

Overall, JustEat has made a wise decision by downsizing its operations and scaling back investments in many markets, focusing on the ones where they are most confident of winning. This resulted in an overall increase in EBITDA across all regions as well as free cash flow, and these improvements are expected to continue in FY25. Furthermore, the company also has a strong balance sheet to contend with. Although there are positives, I still have my concerns regarding management’s ability to drive growth for growth in Northern Europe, the UK and Ireland. Therefore, I classify the company as a held company.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.