Halbergman/E+ via Getty Images

It’s been a very tough year for small- and mid-cap stocks that have nothing to do with AI, but perhaps one of the most challenging stories we’ve seen this year is Peloton (Nasdaq:bton). The exercise bike maker keeps at it Dealing with weaker demand after a temporary pandemic-era boom, which led to multiple rounds of layoffs and leadership changes.

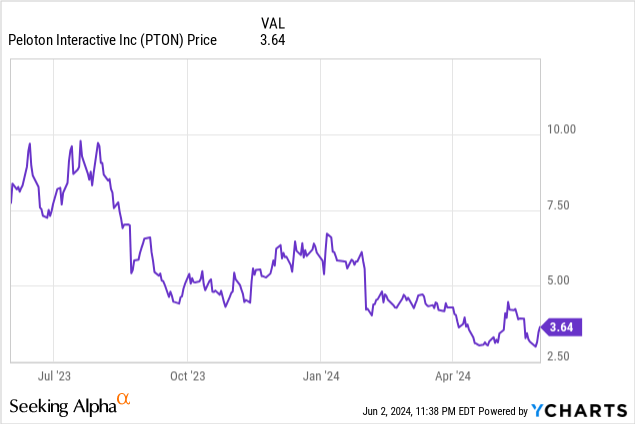

Year-to-date, Peloton shares are down nearly 40%. Although I certainly think this stock is not a safe long-term investment, it’s worth noting that it’s not everyone Bad news for Peloton: In fact, there are some bright spots to note for investors considering a switch in the short term.

I last wrote a neutral opinion on Peloton in February, when the stock was still trading in the low-$4 range. A lot has happened since then, including the company Fiscal third quarter (March quarter) earnings release, completed refinancing, and CEO shake-up.

While Peloton has certainly been a source of investor criticism over the past few years, it’s helpful to take a more balanced look at this company to understand where opportunities may lie. Overall, I wouldn’t recommend Peloton as a forever, “sleep at night” stock: but active traders who want to profit from short-term volatility have near-term catalysts to fall back on.

The bright side of Peloton

There are a surprising number of positives to note about Peloton, and we’ll go over them all here.

First important update: Peloton recently closed a major refinancing deal. Liquidity has been a major concern for Peloton investors as the company deals with the fallout from falling demand. In late May, the company announced a major refinancing to shore up its liquidity. The refinancing consists of $1.35 billion in drawn cash, $1 billion of a 5-year term loan, and $350 million of convertible debt securities due in 2029. The longer maturity here gives Peloton plenty of breathing room to try to revive growth across its product lines. . The company also secured a new $100 million undrawn revolving credit facility to further enhance liquidity. The company also noted that it was able to buy back $800 million of its existing convertible debt At a discounted price.

Secondly, the company has a number of avenues for revenue growth, which include:

- Relaunch of Tread+: In the third quarter, the company relaunched its Tread+ product line, the latest version of the Tread product that had not been updated in three years.

- Growth in rents. The rent/lease model is gaining steam as more and more people shy away from dropping thousands of dollars on a Peloton machine. In the third quarter, the company reported that rental revenue rose 10% year-over-year and, also more importantly, Lease purchases (people who end up buying a Peloton after renting it) have exceeded expectations. In my view, the rental business is quite progressive for Peloton, increasing accessibility by offering a “try before you buy” option.

- Life deal. Also last month, the company announced it would place Peloton devices in 800 Hyatt hotels. All of these hotels will have a Peloton bike, and some will also offer a Peloton Row. This deal paves the way for additional large-scale installations in gyms, hotels or other institutions.

And while we should never base a bullish case on an entire company on the possibility of an acquisition, we can’t forget that the private equity buyout rumors in May could continue to serve as a floor for Peloton’s stock price.

However, there are still risks

This being said: We won’t turn a blind eye to Peloton’s risks, either.

Organic trends continue to be challenging for the company. The silver lining here is that the company has had sequential growth in the number of Connected Fitness subscribers.

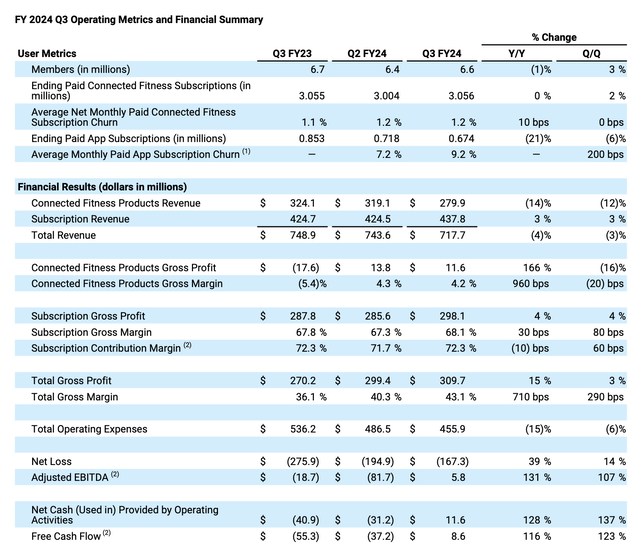

Highlights of Peloton Q3 (Peloton’s third-quarter earnings announcement)

As shown in the image above, the company ended its latest quarter with 3.06 million Connected Fitness subscribers, up 52,000 sequentially from Q2. However, the company points out that the change is still an issue, especially for App+ memberships after old pricing ends and price increases begin. In its third-quarter shareholder letter, the company also lowered its full-year outlook for memberships, citing lower trends:

We are lowering our full-year forecast for the end of paid connected fitness subscriptions by 30K, or 1%, at the guidance midpoint to 2.97 million. Connected Fitness paid subscription guidance reflects an updated forecast for device sales based on current demand trends and forecasts of seasonally low demand. The fourth quarter is typically the most challenging quarter for us to grow, due to lower overall seasonal additions as we enter the warmer months of the spring and summer. We also expect a seasonal increase in average net monthly paid connected fitness subscriptions in Q4, due in part to seasonally high subscription cessation rates that we expect to decline in early fiscal 2025.

We are also lowering our forecast for paid app subscriptions to end by 150K, or 19%, at the guidance midpoint to 605K. Paid app subscription guidance reflects lower total additions due to expectations that Q3 trends will continue into Q4. “We are maintaining our disciplined approach to app media spend as we evaluate our app tiers and pricing and optimize our path to paid app subscriptions.”

The resulting impact on full-year revenue was $25 million, or 1% of annual revenue. Although the reduction does not appear to be significant, Paid subscription memberships are the backbone of Peloton’s future, especially in a world where more demand is driven by rentals.

Operationally, the company is also in difficult shape with CEO Barry McCarthy exiting in May, after just two years in the business. The other side of this coin is that McCarthy’s exit also coincides with a major layoff of 15% of its workforce — covering 400 jobs, expected to generate $200 million in annual opex savings (or roughly 7-8% of annual revenue in at that time). current operating rate). Continuity may be lost as the company is still searching for its permanent CEO and with a significant portion of its workforce exiting, but ultimately if Peloton succeeds in reviving growth, it will do so as a leaner, more efficient company.

Main sockets

With Peloton, we have to deal with the good and the bad; In my view, not enough attention has been paid to the company’s growth prospects, especially with regard to the rental business and increasing institutional adoption by companies like Hyatt. While I’m not advocating a long-term hold here, I do think there is rescue value beyond what investors are giving Peloton right now.