Editorial by Patrick Hatt/iStock via Getty Images

Note: All amounts discussed are in Canadian dollars and reference is made to the stock being traded on the Toronto Stock Exchange.

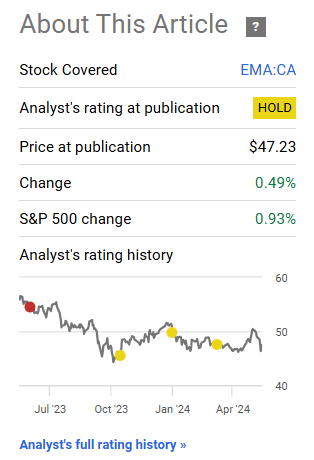

Emira Incorporated (Imrav, tsx:ima:ca) hasn’t gone anywhere since our last review of Company Fourth quarter 2023 results.

Seeking alpha

We gave it a Hold rating, which in other words means we were neutral on its prospects. Its US operations resulted in lower earnings per share numbers, and the company missed analysts’ expectations by a moderate margin. Buoyed by recent interest rate hikes at the time, management was confident Emera would deliver growth in “2024 and beyond.” Even the analysts were on the same page, more or less. Its exorbitant 90% payout ratio didn’t provide any breathing room for earnings numbers, and its 6x net debt to EBITDA had the rating agencies in a tizzy. Well almost.

Q4 2024 presentation

At 15X earnings, with a 6% dividend yield, the stock looked cheap, but there was a real risk of the dividend exceeding earnings. We have set the probability of a dividend cut over the next 12 months at 50-75% and summarized our forecasts.

So, after all said and done, you’re looking at a P/E of 17.75X (we assumed $2.70 in underlying earnings) and a dividend yield of 4.16%. The market will most likely break this low at that time, near $40.00 per share. We are maintaining our hold rating due to the risks described and will become more positive following the dividend cut.

Source: “Emera: Dividend cut likely to yield 6% yield.”

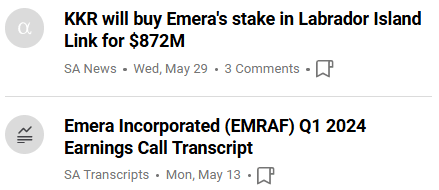

Emera’s first-quarter earnings were released earlier this month, and recently we’ve all heard about the company selling one of its assets.

Seeking alpha

We will cover both of these events next.

First quarter-2024

The first quarter was definitely a big miss by all accounts. Adjusted earnings per share were 76 cents per share, about 8% below consensus estimates. Both Tampa Electric and Nova Scotia Power performed well below expectations. The main hurdles were caused by milder-than-expected weather and some additional hits from a regulatory delay. There were some other factors as well.

- Decreased earnings at Nova Scotia Power (“NSPI”) due to increased operational and operational costs focused on reliability and customer experience, as well as a one-time regulatory disallowance;

- lower contributions from marketing and trading at Emera Energy Services (“EES”), which had a strong performance in the first quarter of last year;

- higher corporate costs due to market losses associated with long-term compensation hedging;

Source: EMA press release for the first quarter of 2024.

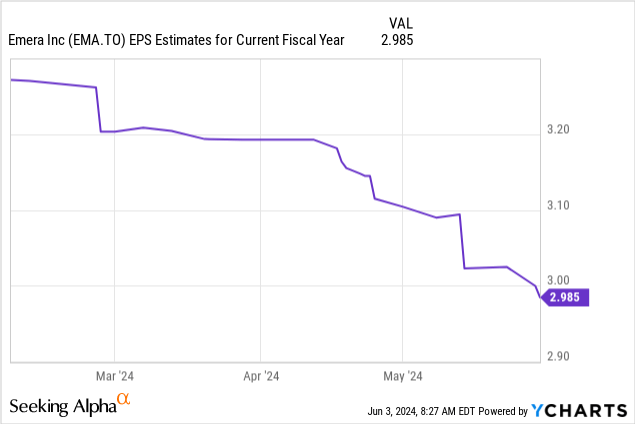

Analysts always try to set up an approach that’s easy for management, and you can see how far they went to help this quarter. We started the year with healthy estimates of $3.28 EPS, and we’re now at $2,985.

In all of this, the “loss” in the first quarter was just 7 cents. So there’s that slow grind that plays a big role. This is likely to be a major blow to Emera’s plans to try to keep earnings in place. Declining earnings also pushes the stock price down, and it’s this same stock price that feeds into the cost of Emera’s stock when it makes its ATM offerings throughout the year. Issuing a stock at $60 has a different effect than issuing it at less than $47. You can sense the urgency to get asset sales done quickly, as the credit agencies were likely viewing these results with great interest. We heard about those on the Q1 2024 conference call.

And if I can finish the asset sale program from what I remember, the asset sale program is sized to be 15% of your capital plan of approximately $9 billion. As you’re encouraged by this process, and have clarity by the end of Q2, I wonder if you could update us on how you see the scale of this program, as well as the number of asset sales you’re doing now.

Scott Balfour

Scott again, so when we talked on the fourth quarter call, we shared that we’re running a couple of processes with this to make sure that we’re successful with at least one that will meet this goal in terms of the capital financing program as you described. But to the extent that we can succeed at both and meet value expectations, we will implement both. Hopefully, as I said, we will have clarity on all of this by the end of June.

Source: Transcript of the EMA Q1 2024 conference call.

We cleared up a big deal quickly.

Emera Inc. announced (Emera), an international energy and services company, and KKR, a leading global investment firm, announced that they have entered into a definitive agreement whereby KKR will acquire Emera’s indirect minority interest in Labrador Island Link (LIL). The deal is valued at C$1.19 billion, consisting of C$957 million in cash and C$235 million to assume Emera’s commitment to fund the remaining initial capital investment.

Source: EMA press release.

It is difficult to model these sales for the impact of EPS. But to the extent you sell assets to pay off debt, you will always have dilution per share. Here, you can expect about 7-10 cents per share during the first year compared to the baseline numbers. We don’t think this has been designed yet in expectations.

Expectations and judgement

There’s this second big sale pending. Most expect it to be New Mexico Gas, and the price will likely be higher than what they got for LIL. The estimates we’ve seen are closer to $2.0 billion. Once again, we are looking at a second round of earnings relief. After all said and done, we’re looking at 2024 EPS, just short of dividends. This will happen despite both deals closing in the latter part of the year. The run rate should be well below the dividend and the payout ratio should remain above 100% in 2024 and 2025.

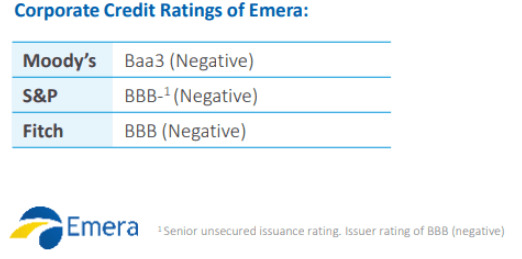

It will be interesting to see how credit ratings view this whole setup. Asset sales must ensure that there is no reversion to a lower rating. Debt metrics should return to their comfort zone. However, the payout ratio will still be really weird. Most utilities aim to keep this ratio below 80%, and we will not reach this percentage at any time during this decade if management aims to grow at the current rate. Even with a freeze, you are looking at 2028-2029, assuming everything goes well.

Rating agencies are a little more lenient on this matter, because they realize that dividends help recruit investors and allow for the issuance of shares. If you ignore the dividend aspect, Emera doesn’t look very cheap. There was the illusion of “cheapness” if you look at the P/E ratio in 2023. But that was created by loading on the debt side and pushing debt to EBITDA above 6.0X. As Emera breaks this down, the real earnings power after deleveraging is highlighted. The stock trades at about 17 times earnings after those asset sales.

The threat of a dividend cut is fairly high. We will continue to avoid Emera Incorporated shares until we get them at a multiple of less than 14X. A dividend cut would also help realign cash flow and payments. This isn’t too harsh, considering we get high-quality companies at 10X multiples with much lower debt levels. We rate Emera Incorporated’s stock as Neutral/Hold at the moment.

Please note that this is not financial advice. It may seem so, it seems so, but surprisingly it is not so. Investors are expected to conduct their due diligence and consult with a professional who knows their objectives and limitations.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.