Mikulas1

Barrick Gold stock outperformed

Barrick Gold Company (New York Stock Exchange: Gold) Investors finally felt vindicated. Since GOLD’s last bullish update in March 2024, GOLD stock has significantly outperformed the S&P 500 (SPX) (SPY).). I reminded GOLD investors that strong price realizations are expected to support buying sentiment, underscoring my conviction that “GOLD pessimism will not last forever.”

So, I’m not surprised by gold’s relative outperformance, with underlying gold futures rallying towards a new high in early April 2024. Although buying momentum has stalled since then, strong central bank buying demand and China’s reallocation towards the gold thesis A shiny spot would enhance the potential upside. go ahead. Moreover, with interest rates likely to be peaked by the Fed, it lends credence to a more favorable macro backdrop for further reassessment of the valuation of hard-hit leading gold miners like Barrick Gold.

Barrick Gold should do better the other half

Barrick Gold’s first-quarter earnings release in early May 2024 underscored the gold miner’s improving execution as Barrick Gold’s performance exceeded Wall Street estimates. While gold production declined by 12,000 ounces year over year, Barrick Gold expects production to increase in the second half as it completes “planned maintenance at its Nevada gold mines.” Accordingly, Barrick Gold’s upbeat production guidance suggests a higher production weight (54%) in the second half, which could indicate a “strong end to the year.” Therefore, investors should carefully monitor Barrick Gold’s production cadence from Q3 as the gold miner looks to achieve its fiscal 2024 gold production guidance of between 3.9 million and 4.3 million ounces.

In addition, Barrick Gold also expects more robust copper (HG1:COM) production in the medium term. Long-term growth in copper demand supports “the global transition to renewable energy, highlighting the critical importance of the metal in greening the global grid.” As a result, Barrick Gold stressed the importance of its efforts in identifying “expanding its copper portfolio as a strategic priority following the merger with Randgold five years ago.”

Despite this, copper is still a relatively small portfolio currently. Barrick Gold’s “globally significant organic copper growth project” at its Lumwana copper mine is only expected to reach first production in 2028. While Barrick Gold is expected to be a long-term copper asset base (with an expected life of over 30 years), the market will likely value Barrick Gold for its gold mining portfolio in the near term.

Barrick Gold expects a further rebound in its gold production in the second half following “production delays at Pueblo Viejo following conveyor rebuilding.” In addition, the gold miner has also made progress on “four key organic growth projects.” Therefore, I think it’s reasonable to expect Barrick Gold’s production to continue to rise, improving its operating leverage and free cash flow profitability.

Inflation headwinds and business challenges have hampered Barrick Gold’s production efforts in recent years. Despite this, management remains confident in some aspects of reducing price levels “to 2021 levels.” However, Barrick Gold also warned that prices of “some commodities remain stubbornly high.” As a result, I believe the market is likely to remain cautious about a sharp reversal in profitability growth at GOLD and its mining sector peers in the near term.

Despite my caution, investors should also evaluate whether gold’s pessimism has been built into its valuation, suggesting that expectations of another revaluation are not unreasonable.

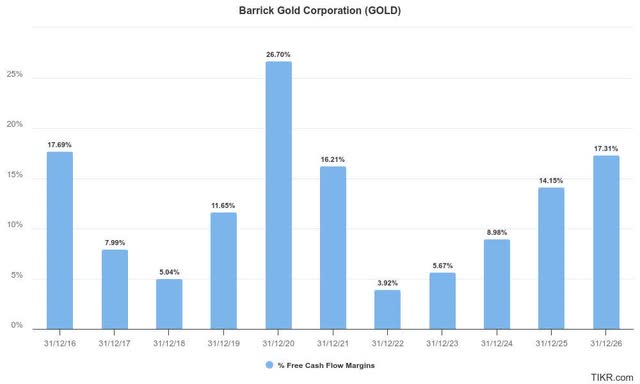

Monitor Barrick Gold’s free cash flow profile

Barrick Gold Free Cash Flow Estimates (Taker)

Being a gold mine, investors should monitor Barrick Gold’s free cash flow dynamics very carefully. As noted above, GOLD’s free cash flow profile tends to be cyclical and rises above previous highs seen in underlying gold futures in 2020. Despite the new highs seen recently in gold futures, the flow profile is not expected to exceed Barrick Gold’s free cash levels from 2021 through fiscal 2026.

Therefore, I consider the pessimism in GOLD stock over the past year justified, as the company has struggled with challenges in production, inflation, labor and commodity costs. However, with Barrick Gold’s free cash flow growth expected to bottom, could gold be rerated higher based on its valuation assessment?

Gold’s valuation is attractive

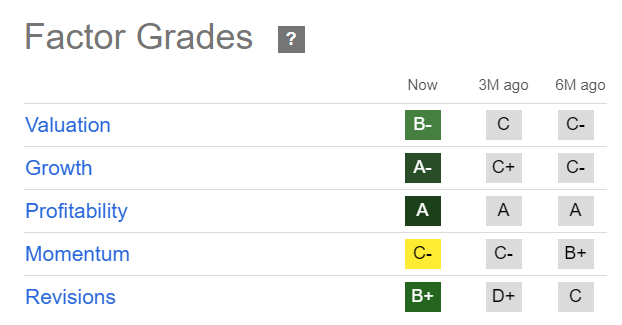

Gold Quantitative Degrees (Searching for Alpha)

GOLD’s rating has improved to ‘B-‘ over the past six months. Barrick Gold’s ability to beat Wall Street estimates has also increased optimism about Barrick Gold’s execution capabilities. As a result, the bifurcation of the GOLD rating (“Growth grade of A-” compared to the rating grade of “B-”) is very distinct, indicating that there is potential for a further reclassification of the rating.

Therefore, I believe Barrick Gold needs to continue to outperform in the second half to justify GOLD’s recent optimism. The market is likely still concerned about adverse inflation dynamics that could hamper its FCF profile.

The H2-weighted production profile also increases potential execution risk to Barrick Gold’s ability to meet FY 2024 production expectations. Furthermore, the rise in copper prices is not expected to be a material driver of near-term valuation, given the current production volume of its asset base.

Should gold stocks be bought, sold, or held?

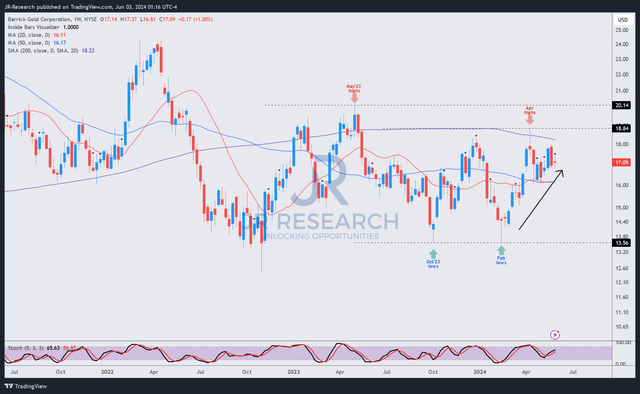

Gold price chart (weekly, average range, dividend rate) (trading offer)

Despite this, the improving buying momentum in gold is expected to continue. Gold’s lack of selling intensity (Momentum Grade “C-“) underscores my confidence in the recent optimism in the market.

Additionally, Barrick Gold has a very strong balance sheet with an adjusted EBITDA leverage ratio of just 0.1x for 2024. Therefore, it should provide significant collateral for potential M&A activity to bolster its investment portfolio. It should also provide income investors with clarity on Barrick Gold’s ability to maintain its 2.3% forward dividend yield, supported by a potentially improving FCF profile.

Gold price action is also approaching a potentially decisive break above the $19 level. This level was retested in April 2024, but the selling intensity quickly faded in May 2024 as it bottomed above $16. Therefore, I believe a strong buy sentiment on the dip would help halt further decline towards the 2023 gold lows and promote a subsequent breakout above the $19 resistance area.

With this in mind, gold investors should continue to hold their positions as they expect a more robust production performance in the second half.

Rating: Keep buying.

IMPORTANT NOTE: Investors are reminded to conduct due diligence and not to rely on the information provided as financial advice. Consider this article to complement your required research. Please always apply independent thinking. Note that the classification is not intended to specify a specific entry/exit time at the time of writing unless otherwise stated.

I want to hear from you

Do you have a constructive comment to improve our thesis? Spotted a critical gap in our view? Did you see something important that we didn’t do? agree or disagree? Comment below to help everyone in the community learn better!