Photos by Adam Gault/OJO via Getty Images

Introduction and thesis

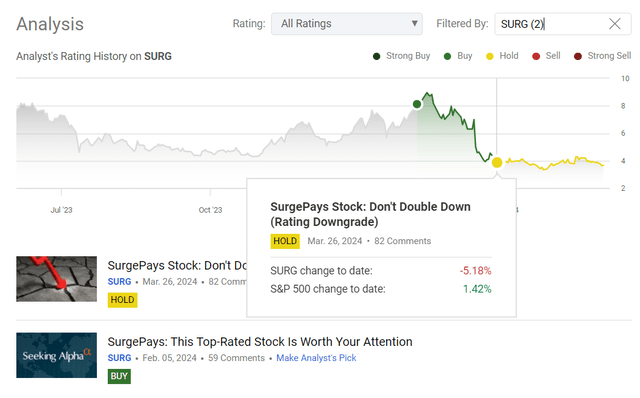

Coverage has begun Serge Bayes Company (Nasdaq: Surg) stock with a “buy” rating back in February 2024. At that time, I underestimated the risk of ACP financing, which eventually materialized relatively quickly, so I had to revise my rating: In March, I downgraded SURG to “Hold” and since then, the stock is down more than 15% while the broad market continues to rally.

Seeking Alpha, my coverage of SURG stock

I would like to thank one of our Seeking Alpha readers – TMT Investor – whose comment described SURG very succinctly – SurgePays turns out to be a “radioactive” stock so to speak because a large portion of its revenue was (and still is) dependent on a policy decision that has not yet been made as of a few weeks ago past. Therefore, the market gives the stock Fair discount on its evaluation. On the other hand, after a lightning drop of tens of percent in just a few weeks, SURG’s current stock price looks relatively reasonable in my opinion (in other words, the “radioactivity” is starting to decline a bit).

I think SURG should be viewed as an option (i.e. a derivative instrument) – until the ACP funding is passed on, its value may trend downward, like the value of an option eroding over time. However, when/if the long-awaited catalyst occurs, we will likely see a massive price rise, supported by the “cheapness” I believe in the second outcome of events – which is why SURG remains in our model portfolio (for a very small allocation). But to be realistic, I can’t upgrade the stock to ‘buy’ this time. It’s still a “hold”.

Why do I think so?

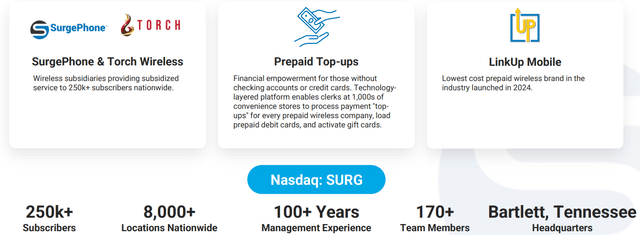

SurgePays, Inc. It is now a technology and communications company with a market capitalization of $72 million that provides mobile broadband services. The company specializes in providing financial and telecommunications products to underserved populations through convenience stores. SurgePays operates a technology platform that enables sellers in thousands of convenience stores to offer mobile and prepaid financial products to low-income, underbanked and underserved consumers.

SURG’s infrared materials

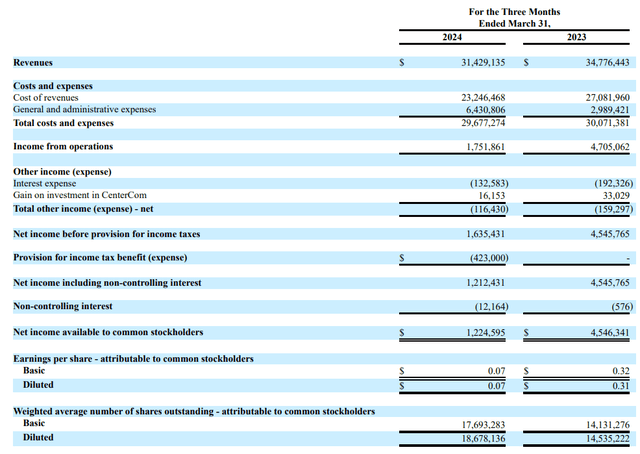

In the first quarter of fiscal 2024, SurgePays reported a 9.6% year-over-year sales decline. Cost of goods sold decreased approximately 15% compared to the previous year, so gross margin increased to 26% (from 21% last year). However, due to a 115% year-over-year increase in general and administrative costs, SURG’s EBITDA fell by 63% (more than 2.5x), resulting in a 3.7x decline in net income and a 4.4x decline in profitability stock (due to an increase in outstanding shares by 28.5% year-on-year).

SURG Income Statement, 10-Q

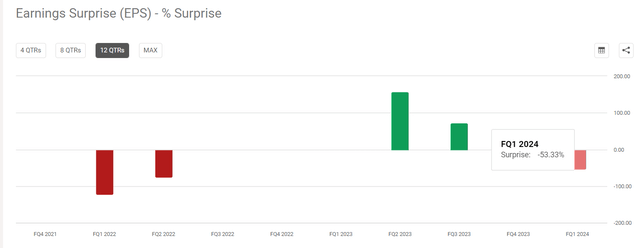

Overall, SURG would have been able to beat consensus EPS expectations had it not been for the abnormally high general and administrative expenses and rapid growth in the number of shares outstanding, with sales actually being 24.3% better than expected, but unfortunately we saw this time miss EPS.

Seeking alpha

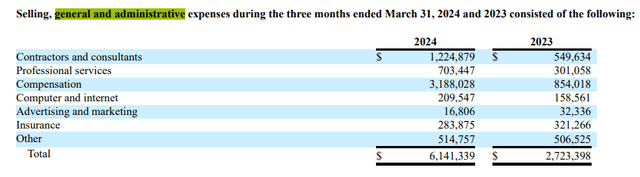

If we take a closer look at the G&A structure, we see that expenses increased mainly in the areas of “Contractors and Consultants” and “Compensation”.

SURG’s 10-Q, Author’s Notes

The first item included the costs of overhauling the financial platform “to enable the transition from the legacy VeriFone terminal to a tablet-based transaction in the markets, as well as the costs of advisory services specifically in the area of investment relations” to identify opportunities. To increase our shareholder value.”

I have minimal concerns about this type of expense. However, the second item, “Compensation,” includes a one-time non-cash component of stock compensation for the CEO and CFO of $1,359,931, according to their employment agreements. In addition, there were 2024-related bonus accruals totaling $382,500, according to the 10-Q. I don’t quite understand this self-compensation approach here.

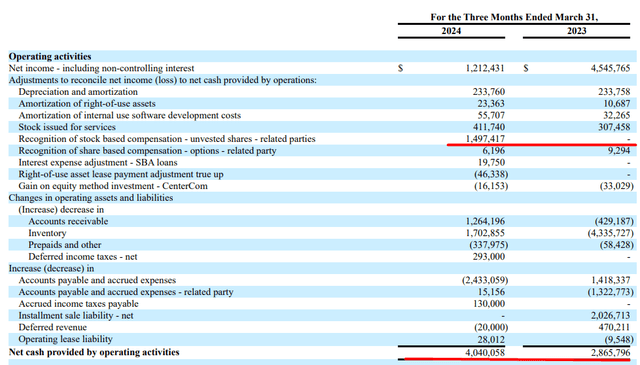

The increase in management compensation expense caused SURG’s operating cash flow in the first quarter to increase approximately 41% year over year. However, if we exclude this one-time item, CFO is down approximately 11.3% year over year for the same period:

SURG Cash Flow Statement, Author’s Notes

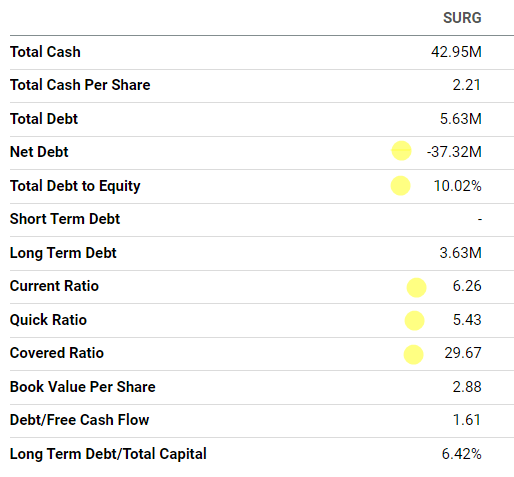

Regarding liquidity and solvency, the company seems to have no obvious problems in my opinion: with a negative net debt of -$34 million, a debt-to-equity ratio at around 0.1, and a current ratio of over 6, SURG’s financial position looks solid.

Seeking Alpha, Sorg, Author Notes

The good liquidity position on the company’s balance sheet is in many ways due to the growth in current assets – namely the cash balance of $42.9 million (about 61% of total market capitalization), which grew by almost three-fold on a quarterly basis. This growth is due to a lack of capital expenditures in the first quarter of fiscal 2024 and is primarily due to “proceeds from shares issued in cash” and “proceeds from the exercise of common stock warrants.” Management appears to have benefited from rising stock prices and improved the balance sheet by diluting equity.

Overall, I don’t see any unhealthy skews in working capital changes. Therefore, in my opinion, the significant increase in liquid funds on the company’s balance sheet should be enough to cover operating expenses for at least six and a half quarters (based on Q1 FY2024 as a reference). SURG’s balance sheet and liquidity seem to be in pretty good shape as of today, from what I can see.

However, balance sheet strength is not the most important thing that investors should pay attention to.

As I understand it, the third-party consultants whose salaries helped boost G&A in the first quarter likely prompted SURG’s management to spend more time on the recent earnings call on the topic of “The Future With and Without ACP Funding,” — here’s how CEO Brian explained COX VISION SURG:

I would like to stress this point, our business plan never included the word ACP.

Keep in mind that if ACP is not funded, millions of existing ACP customers left in the lurch will be looking for a new prepaid wireless carrier to replace their subsidized service. Our plan is to leverage our relationship with our existing ACP base to turn them into value, low-cost plans, while offering aggressive promotions to convenience stores and wireless merchants, who represent front-line access for those who use all other ACP carriers.

We believe this will give us the upper hand in converting many more ACP customers into LinkUp Mobile customers. In any scenario, we believe we have the team, products and distribution to deliver very significant success, regardless of how the ACP financing situation evolves.

The Affordable Calling Program (ACP), which provided monthly internet discounts of $30 to $75 to 23 million households, was SURG’s main revenue source for a long time. April was the last month participants received the full discount, and the remaining funds will be exhausted after a smaller $14 benefit was offered in May, according to Broadbandbreakfast. On May 9, 2024, the Senate passed the FFA reauthorization package without including an amendment to ACP funding—so the most likely outcome of events is that SURG revenues will actually have to manage without budget support for an extended period.

When management says that without ACP, a company will simply begin converting its ACP base to lower-cost value plans, what it really means is that operational expenses will likely increase significantly and revenues will likely not decline 50-60% right away in Best of luck. This is exactly what I think you should prepare for – the business recession has already begun.

However, the good news is that Wall Street is already preparing for the worst: SURG is expected to generate a loss per share through the remainder of fiscal 2024, and revenue is expected to decline 40.5% for fiscal 2024, which is a significant number. The turning point is expected to come in fiscal 2025, according to consensus, when sales are expected to grow more than 10% thanks to the low base and EPS is expected to return to positive territory at $0.34 (which is less than half the adjusted figure). For the fiscal year 2023).

Seeking Alpha, Sorg, Author Notes

The forecast for the next two years means that the current P/E ratio of 3x (TTM) loses all analytical meaning – by the end of this year, this multiple should become strongly negative (about -32x), and by the end of 2025, we will see 10x if nothing changes in Expectations (for this to happen, management really needs to implement its plans to transform the company, which is very difficult). And therein lies the “radioactivity” of SURG and its valuation – the stock is cheap for a reason, and its multiples calculated by TTM tell us absolutely nothing about future growth.

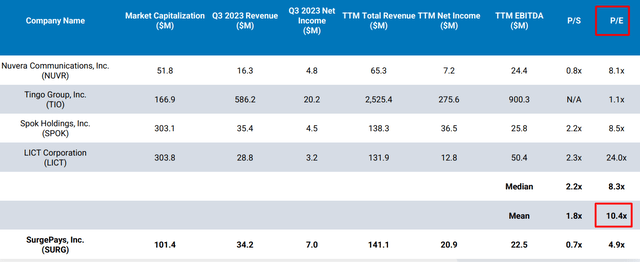

SurgePays need an ACP trigger to fly – but that’s clearly not what I’d recommend betting on. The company is currently fairly valued, assuming management will be able to replace a significant portion of ACP-related revenue over the next two years. With a price-to-earnings ratio of 10x by fiscal 2025, SURG will trade around the average of the companies it compared itself to in IR Materials at the start of 2024.

SURG’s IR, Author’s Notes

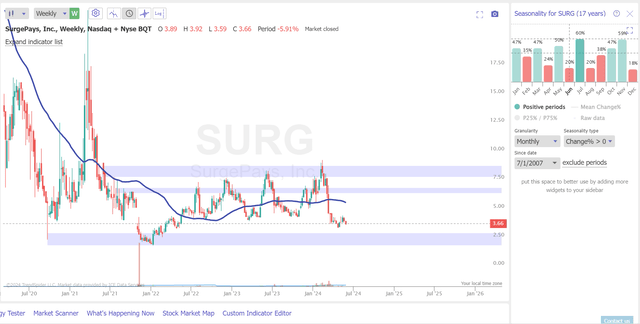

From a technical perspective, I see more downside potential – at least to the strong demand area in the $2-2.8 per share range, which corresponds to a downside potential of about 1/3 the size of today’s stock price. However, seasonal data shows us that June is statistically the most positive month for SURG since 2007.

TrendSpider, Author’s Notes

Who knows: maybe the news background will change soon? I don’t know the answer to this question, but clearly that’s not the reason to buy SURG today.

The upside risk to my results

However, we cannot rule out the possibility of redeeming ACP soon. Judge for yourself: If the program’s funds are not recovered, millions of families may face difficulties in paying their Internet bills, leading to public protests and pressure on politicians. Is this what they will target before the presidential elections? i don’t think so. I believe politicians may exploit the situation to gain voter support, promising to secure additional funding for the ACP if elected, thus changing the narrative for SURG.

When ACP funding is finally approved, I wouldn’t be surprised to see SURG tens of percent higher than current levels – we may even see new local highs. Why? Because in this case, the TTM valuation levels, which now play no role in determining the investment attractiveness of the stock, will begin to play this role – forward-looking metrics based on consensus forecasts will immediately become too pessimistic because they will be based on an assumption that will not have any practical meaning. Anymore. This is currently the most important upside risk to consider, in my opinion.

Judgment

Again, I don’t see any reason to bet on SURG today, as we don’t have any clear indications that ACP funding will go through in the foreseeable future. We continue to hold stocks with a very small allocation in our model portfolio because I think SURG looks fair value today on a forward-looking basis (beyond 2024). But I do not hope for a quick recovery, it would be a miracle, if there is no trigger for it. I’m also confused about management bonuses, which seem out of place against the backdrop of current events. For all these reasons, I have decided not to upgrade SURG to ‘Buy’ but to reaffirm my ‘Hold’ rating today.

Thanks for reading!

Editor’s Note: This article discusses one or more small-cap stocks. Please be aware of the risks associated with these stocks.