Evening pictures

For the fiscal year ending March 31, 2024, Tokyo Electron Co., Ltd. (OTCPK:TOELY) (“TEL”) reported consolidated net sales of 1,830.5 billion yen (US$16.6 billion), reflecting a decrease from the prior year’s net sales of 2,553.3 billion. yen. . Despite this reduction, the company maintained strong profitability. Employment Income for the same period was JPY422.1 billion (US$3.8 billion), reflecting a strong operating margin of 23%.

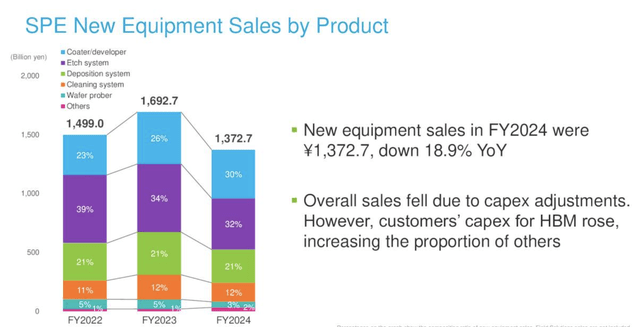

Tokyo Electron is a leading semiconductor equipment company with leading market share in several process equipment segments, third only to ASML Holding NV (ASML) and Applied Materials, Inc. (AMAT) in terms of global revenue. TEL’s revenues by the fiscal year ending March are shown in Chart 1.

Although Etch’s system sales percentage declined in FY24, it still maintained a dominant 55% share of Dielectric Etch (ahead of Lam Research Corporation (LRCX) by 29%), according to the Information Network report titled Global Semiconductor Equipment: Markets, Market Shares and Market Forecast.

Although TEL led the buffer drilling market in CY 2023, it lost 611 basis points to LRCX. TEL hopes to regain its share in 2025 by introducing cooling technology equipment capable of producing memory channel slots in advanced 3D NAND devices with an array of more than 400 layers.

However, TEL neglected to mention in its press release that LRCX already had the cooling technology technology, which is why it was dominating the NAND drilling business. According to Lam CEO, Timothy Archer:

“In etching, Lam uses high aspect ratio cryogenic etching to enhance memory hole formation productivity. Today, we are approaching 1,000 Cryo Etch chambers in our high-volume installed manufacturing base. In partnership with our customers, we are harnessing the potential of the enormous amount of data coming from this installed base “To rapidly improve technology and cost at each successive layer transition in NAND.”

phone

Chart 1

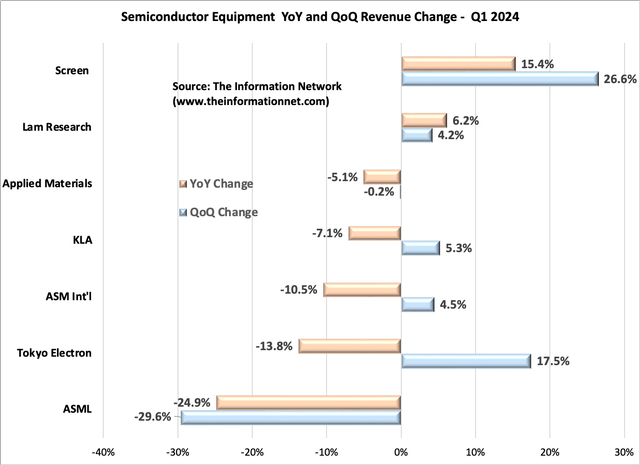

Chart 2 compares quarterly and quarterly revenues for the top 7 companies reported in Q1 2027. Not only were TEL revenues down 18.9% year over year in FY2024, but for Q1 FY2024 (Q4 2024), revenues decreased 13.8% year over year but increased 17.4% quarter over quarter.

In fact, TEL showed the second-largest quarter-on-quarter growth (for Japan’s Screen Holdings) in the first quarter of 2024, and the largest rebound spread among the seven companies comparing growth year-over-year versus quarter-over-quarter. The two Japanese companies showed the largest quarter-on-quarter growth among the Big Seven companies.

Information Network

Chart 2

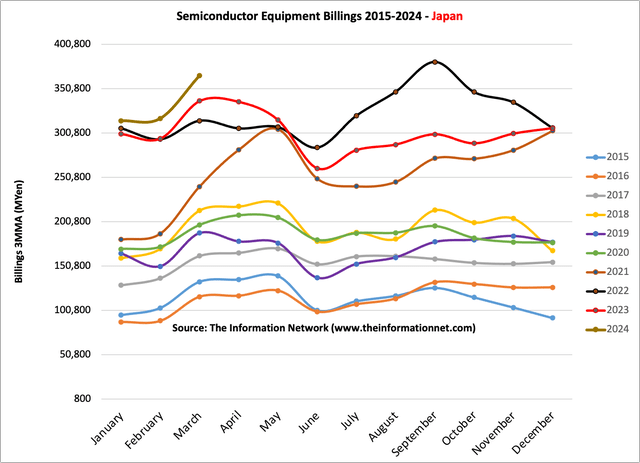

Chart 3 shows the revenue growth of all Japanese equipment companies and correlation with Chart 2 in which the two Japanese companies showed the greatest growth.

Information Network

Chart 3

Comparison of growth by equipment type

In comparing revenues by major equipment type, TEL, AMAT and LRCX compete with each other in two segments – drilling and sedimentation.

In the drilling equipment sector, where I combine isolation drilling and conductive drilling:

- Tokyo Electron announced a market share of 28% in the Cyprus year 2023.

- LRCX, which has a strong share in both sectors, accounted for a 39% share, while…

- AMAT holds a 22% stake.

Comparing deposition equipment is more complex because it includes several different types of equipment. The two main divisions are PVD and CVD, but CVD is divided into ALD, PECVD, and LPCVD (tubular and non-tubular). AMAT has a dominant share in the PVD market but a negligible share in ALD. TEL is the dominant player in ALD but does not compete in the PVD market.

One sector in which they are all competing is ductless low-pressure chemical vapor deposition (LPCVD). The “tubeless” variant refers to equipment designed for processes that do not use traditional tube furnaces. Instead, these systems often use more advanced chamber designs that can provide better uniformity and control, which is essential for modern semiconductor manufacturing, especially as device geometries continue to shrink.

In the non-tubal cardiovascular disease sector, 2023,

- TEL led the market with a 39% share, slightly ahead of

- LRCX with a 38% stake, and before that

- AMAT with a 23% share.

2024 forecast and the impact of China sales in 2023

Toshiki Kawai, President and CEO of TEL, noted on the company’s Q4 2024 earnings call on May 10, 2024:

“The WFE market size for calendar 2024 is expected to reach $100 billion. We expect investment in high-end DRAM to begin to recover from late 2024, driven by growing demand for DDR5 and HBM, among others.”

To illustrate the expected growth, WFE volume in 2023 was $97.5 billion, a growth of 2.6%. I referenced a March 4, 2024, Seeking Alpha article titled “WFE Applied Materials Market Share to Drop 5% Below ASML in 2023.”

“For 2024, I see a rebound in WFE revenue, which fell by double digits in 2023, but due to withdrawals from 2024, primarily by Chinese semiconductor companies, that recovery will not happen until the second half of 2024.”

Information Network

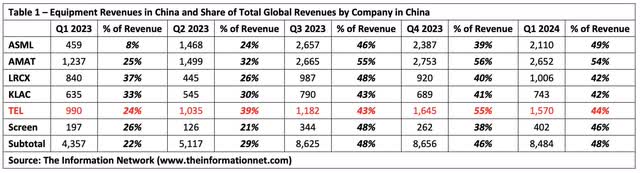

Table 1 shows equipment revenues from China and the percentage of these revenues to total global revenues between the first quarter of 2023 and the first quarter of 2024. In the second half of 2023, revenues doubled compared to the first half of 2023 as Chinese semiconductor companies began stockpiling Foreign equipment in anticipation of more stringent sanctions by the United States. Government. AMAT received the largest percentage of revenue from China. Chinese customer investment in mature nodes was active throughout the year, based on sanctions that limited nodes to above 16nm, as financing to enhance the capacity of mature nodes accelerated.

There is no relationship between the proportion of sales to China and global growth on an annual or quarterly basis.

Investor takeaways

Prospects

In 2025, capital investment in NAND and advanced logic/foundry is expected to fully recover, following the previous recovery in DRAM. The main driver of this growth is the AI server market, which is experiencing an annual growth rate of 31%. In addition, AI technology will be integrated not only into servers but also into computers and smartphones. Servers are expected to grow by 32% year over year; Personal computers are expected to grow by 14%, and smartphones are expected to grow by 15% on an annual basis until 2025.

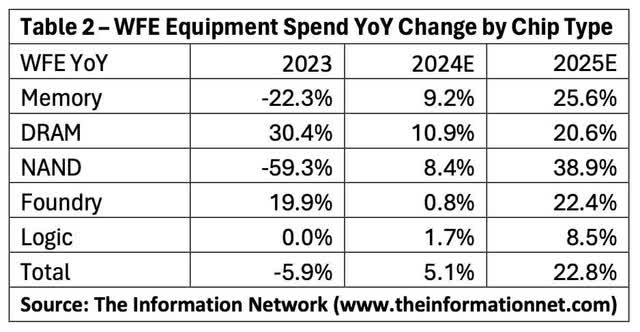

These factors are expected to drive the wafer fabrication equipment (WFE) market to achieve double-digit growth in 2025. Chapter 2 explains the expected change in WFE spending by wafer type.

Information Network

According to TEL’s FY2024 earnings presentation in Chart 4, the big revenues are in the non-memory segments. As shown above in Table 2, in 2025 I expect all WF sectors to show double-digit year-over-year growth except Logic at 8.5%, but this is due to the poor performance of Intel Corporation (INTC), the largest Logic company.

phone

Chart 4

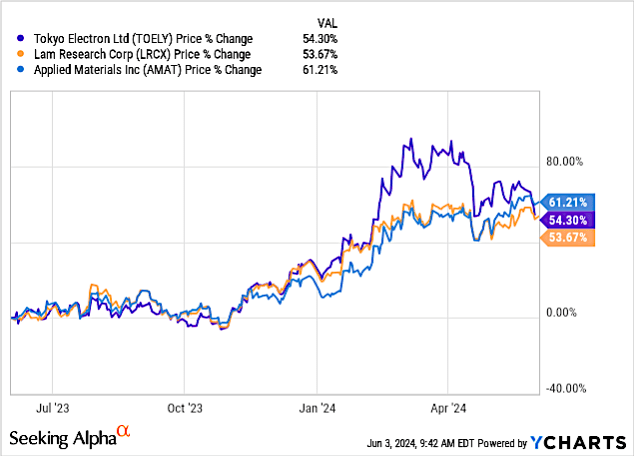

Compare stock prices

On a competitive basis, TEL maintains a dominant share of Dielectric Etch ahead of Lam Research, a 90% share of resistive coatings ordered with ASML Systems, and is the No. 3 company in the global semiconductor industry after AMAT and ASML. The stock price performance compared to competitors AMAT and LRCX is shown in Chart 5.

TEL began to break through to competitors in early February 2024, but in mid-April, Tokyo Electron’s stock price saw a significant decline.

YCharts

Chart 5

TEL is oversold, and I rate the company a Buy.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.