Broadstone Net Lease: Higher interest rates for a longer period which keeps the stock undervalued

Emark

As interest rates remain high for longer, there is one industry that has continued to be punished: real estate. In fact, we may not see a drop in interest rates for another 3 to 6 months, which could mean REIT stock prices may remain… a little. However, despite the many macroeconomic impacts Fears In the REIT space from an office space perspective, Broadstone Net Lease (New York Stock Exchange: BNL) shines brightly, alleviating those concerns – given its specific real estate focus, balance sheet composition and performance. The specific focus that allays fears is industrial focus. Why industrial? Think – warehouse space for large consumer-focused companies (e.g. Amazon)Amzn), Goal (TGT), etc.).

BNL is a diversified real estate investment trust managed by a single tenant. The concentration of industries amounts to 54.2% of its total portfolio, but it also shows diversification with participation in restaurants (14.2%), healthcare (13.4%), and retail (11.9%), with its lowest concentration being offices (6.3%).

Broadstone portfolio page

Not only is risk reduced, with its lowest concentration in office space, on a per-tenant basis, but all tenants lease less than 5% of the total available space. The largest tenant is industrial client, Roskam Foods, with 4.2% of the portfolio. Therefore, it is not too dependent on one industry, nor one tenant.

In addition, BNL is very strategic regarding the type of buildings and tenants it has. With industry as its largest focus, for example, BNL says: “We look for industrial properties that are located in close proximity to major transportation routes such as airports, ports, railways, major highways or interstate highways.” This makes perfect sense, because that’s what tenants or their end users want – speed. How quickly can the product be picked up, stored and then shipped? This is what BNL likes to be in – a desirable location to satisfy the need for speed.

So, it’s time to see if the REIT industry is a great space to invest in right now, but specifically if BNL is a great stock to buy at current prices and hold for the long term. We will do this by looking at the balance sheet and financial performance.

balance sheet

BNL’s balance sheet following its recent quarterly earnings release is very interesting. Total assets increased slightly compared to the end of the year, but liabilities decreased.

The specific areas where commitments decreased were a $17 million decrease in credit facilities. In a high interest rate environment, this is a good thing, because it means that interest expenses may reach a plateau, which we will see further in the financial performance section.

Within footnotes 10-Q, BNL’s debt maturity schedule is split between unsecured and secured. The unsecured term loans mature in 2026-2029 at variable rates of approximately 6.00%-6.60%. When prices fall, these prices will fall with them. The unsecured term loans mature in 2027-2031 and are fixed, with the highest interest rate at 5.19% (maturity in 2029). The interest rate on the 2031 unsecured bonds is 2.60%, which is well below the market and, fortunately for them, the longest form of the maturity schedule. Secured mortgages, fairly insignificant overall at $78 million (insignificant because unsecured term loans are over $1.7 billion), with an interest rate of 3.6%-4.9%, maturing 2025-2028.

Overall, BNL’s debt schedule looks appropriately managed, with unsecured term loans being linked to a short-term variable interest rate, which is smart if rates start to turn south and anything fixed is at a low rate as well, with the highest being a fixed rate. Interest rate 5.19%

Lease real estate assets are down about $190 million since the end of the year, and you can see that’s more likely from the sale of 39 properties this quarter, as part of the simplification of their healthcare focus. Therefore, BNL used a portion of the proceeds to acquire properties worth $40 million, but the remainder was converted to cash and cash equivalents.

After evaluating the balance sheet, it appears that BNL should be set up for further acquisitions, given its credit facilities are down from year-end and cash and cash equivalents amount to more than US$221.7 million, up from US$19.5 million at year-end. Therefore, I expect an active market for NBB over the next 6 to 12 months. The recent properties were acquired at an average capitalization rate of 8%, which I’m sure NBB wouldn’t want to go much lower than that.

In conclusion, on the balance sheet, BNL has room to expand in time, but can still earn a high rate on the idle cash of its balance sheet. After that, BNL’s financial performance came to the fore.

Financial performance

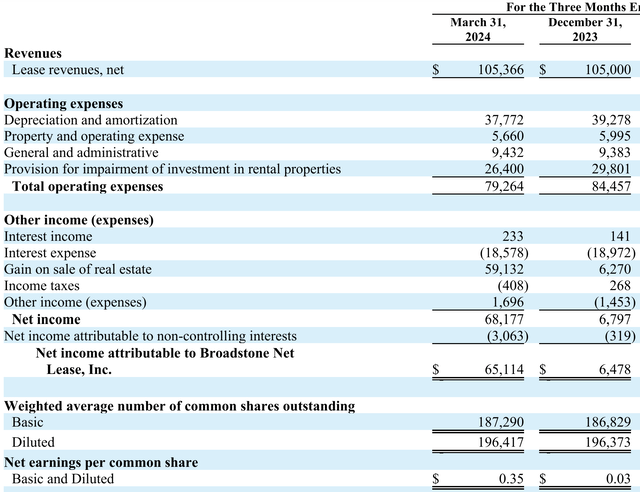

Echoing similar comments I made regarding the balance sheet, revenue for Q1 2024 remained fairly flat/consistent with Q4 2023, at $105 million.

However, here are the bright spots:

- Expenses decreased by $5 million

- Interest income amounts to $90,000

- Interest expense decreased by $400,000

- Gains from the sale of real estate amount to $53 million from the previously discussed health care simplification.

Broadstone Net Lease Earnings Release

Adjusted funds from operations ended at $0.36, which is just one cent higher than the basic and diluted EPS you see above. AFFO was also $0.36 in the prior quarter and $0.35 in the quarter before that. Therefore, AFFO growth is fairly low at the moment. This did not prevent management from increasing its quarterly dividend from $0.28 to $0.285; Which is still covered by funds from operations at $0.36.

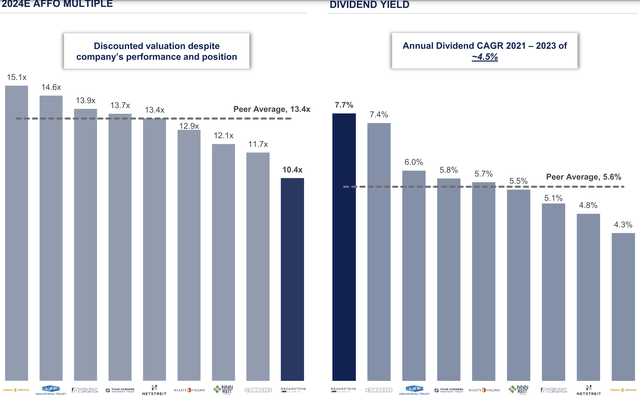

From a valuation perspective, BNL trades at a 10.5x forward AFFO ratio, based on forward guidance from management ($1.41-$1.43) and a stock price of $14.96 (May 28 closing price).

Broadstone Net Lease Q4 event presentation

My 10.5x calculation closely matches the management presentation you see above. Management compared BNL with its competitors, including Realty Income (O), which has been a darling among dividend investors, and BNL shows they have the largest value appreciation based on this metric. Among BNL’s peers for AFFO: Realty Income (O) has 12.9x, Agree Realty Corp (ADC) has 13.9x and even WP Carey (WPC) has 11.7x; One might say that BNL is undervalued compared to its peers.

In conclusion, given BNL’s strong balance sheet, being highly liquid, combined with its diversification, we believe the company can be demonstrated to be undervalued in current market conditions versus its competitors. BNL appears to have upside from here, given the liquidity and room to expand its operations following the healthcare simplification sales it achieved last quarter. However, risk factors could include if interest rates remain higher for a longer period, such as in 2026 and 2027, when a significant portion of its loans come due. Furthermore, if we fall into a recession and consumers cut back on spending, which reduces companies’ need for industrial warehouse space, as goods will not move as quickly as they are now, this could pose a risk to BNL. It’s worth noting that the dividend is safe and covered by AFFO, and we’ll likely see another dividend increase later this year, as BNL typically increases its dividend twice a year. Therefore, income investors should keep an eye on BNL.

At current prices, I would be a buyer of BNL. Of course, I recommend doing your own research, as I am not an advisor. Thank you for reading, I look forward to your comments.