milan2099/E+ via Getty Images

Investment thesis

My previous bearish call about Apple company (Nasdaq: Apple) continued well until the company announced its record $100+ billion buyback plan. The market has embraced it wonderfully Optimism The stock has risen about 11% since then. However, to me, this buyback suggests that the company likely can’t offer shareholders anything beyond that. Apple was known for its ability to create “blue oceans” during the Steve Jobs era, but currently the company appears to be struggling to differentiate and create new, multi-billion dollar industries. Product sales continue to decline across all offerings, with competition intensifying and the heavily promoted Vision Pro not being as successful as I expected in 2017. My previous articles.

It also seems to me that the company is still out of the AI race. While other expanders pump billions In artificial intelligence Data Centers Apple’s response has been to introduce a new iPad Pro to a market where competition is rapidly intensifying. Even the stock’s biggest fan, Warren Buffett, has aggressively trimmed his stake in AAPL. I get it, especially since my valuation analysis indicates that the stock is currently overvalued by about 30%, which is a great selling opportunity. Overall, I downgraded AAPL to ‘Strong Sell’.

Recent developments

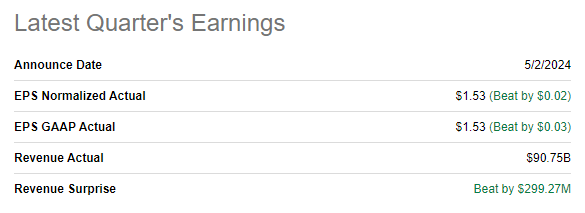

Apple released its most recent quarterly earnings on May 2, when the company beat consensus estimates. Although year-over-year revenue declined 4.3%, adjusted earnings per share expanded by 1 cent.

Seeking alpha

The market reacted to the earnings release with great optimism due to the announcement of a $100 billion stock repurchase plan as well as a stock repurchase plan during the earnings call. Aside from this information, I think there are no longer reasons for optimism. The fiscal second quarter showed double-digit year-over-year revenue declines in three out of five categories.

The most recent AAPL 10-Q report

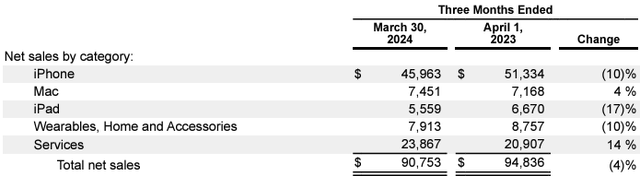

In absolute terms, the services sector was again the only business line with strong growth, at nearly $3 billion. At less than $300 million year-over-year, revenue growth in Macs looks minimal compared to total quarterly revenue. The company continues to exert its pricing power in services thanks to its tremendous brand name and customer loyalty. The most recent subscription fee increases were introduced in late October 2023, and are relatively recent. Despite Apple’s strong brand loyalty, I doubt subscription fees can increase anytime soon without undermining customer sentiment. Therefore, momentum in services revenues will likely start to ease.

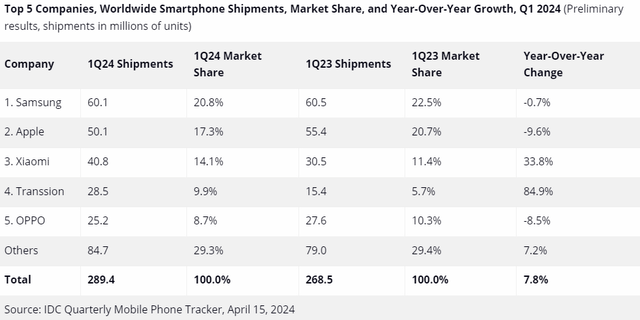

Apple generates more than half of its revenue from the iPhone. This revenue stream has been struggling over the past quarters. According to IDC, Apple’s market share shrank significantly during the first quarter of the year on an annual basis. Market share fell from 20.7% to 17.3% year-on-year, the worst performance among the top five vendors.

IDC

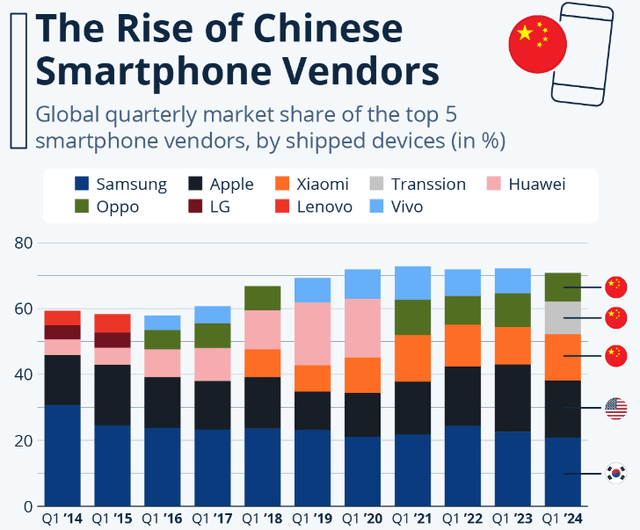

Global smartphone leader Samsung ( OTCPK:SSNLF ) also showed a decline in its market share in the first quarter as Chinese manufacturers gained momentum. Competition in smartphones is heating up quickly, with Apple even offering 20% discounts on iPhones in China. This huge discount helped demonstrate the recovery of iPhone sales in China. To me, this indicates Apple’s failure to differentiate itself from competitors. This is a warning sign because Apple has traditionally been at the forefront of the premium smartphone segment, meaning differentiation has been key to charging premium prices.

Statista

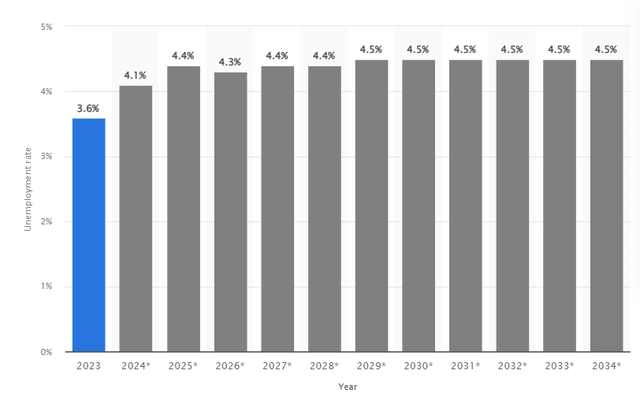

With interest rates likely to remain higher for longer, there is a risk that discretionary spending will be weak. Furthermore, unemployment rates in the United States are expected to grow for two years in a row. This also doesn’t add optimism to discretionary spending and will likely lengthen iPhone replacement cycles.

Statista

The smartphone industry isn’t the only one where Apple is suffering from rapidly increasing competition from Chinese vendors. According to Statista, Apple’s tablet market share deteriorated significantly on a quarter-over-quarter basis in the first quarter, from about 41% to 32%. Meanwhile, Huawei’s tablet market share expanded from 7.6% to 9.4%. Apple recently unveiled a new iPad Pro with a powerful M4 chip suitable for cutting-edge AI applications, which could help differentiate and regain market share. However, intensifying competition in tablets also poses a risk to Apple investors.

The Apple Vision Pro has not been a huge success, as I predicted in one of my previous articles about the company. According to Ming-Chi Kuo of TF International Securities, Apple has lowered its annual forecast for headphones to between 400,000 and 450,000 units, down from the original forecast of 800,000. The product has been aggressively promoted, and such a reduction in forecasts represents a major disappointment.

Finally, all of Apple’s secular challenges seem clear to one of the greatest investors in history, Warren Buffett. Mr. Buffett has been reducing Berkshire’s ( BRK.B ) stake in Apple significantly in recent quarters, which is also a red flag for investors, in my opinion. Berkshire’s stake in Apple is still huge, but reducing its stake for two consecutive quarters is a big trend.

Rating update

The stock is lagging the broader market, which is fair considering all the fundamental challenges AAPL faces. The stock price is up about 9% over the past 12 months, compared to a 26% rise in the S&P 500. On a year-to-date basis, Apple has remained roughly flat, while the broader market has gained about 11%.

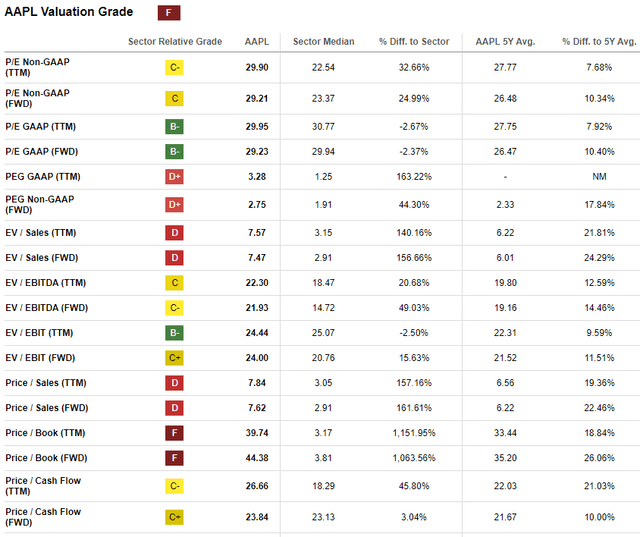

Apple’s valuation ratios are always well above the industry average, but they are fair given the company’s size and profitability. Therefore, it is best to compare current multiples with historical averages. From this perspective, AAPL appears to be overvalued, as its current valuation ratios are higher than the averages of the past five years across the board.

Seeking alpha

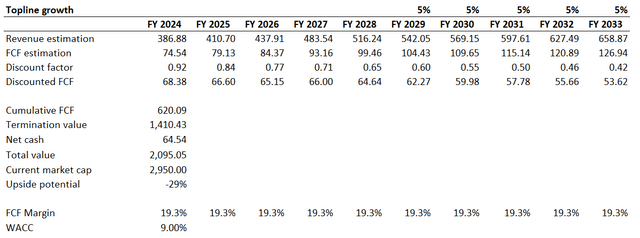

To determine how overvalued I am, I have to simulate a discounted cash flow (DCF) model. The WACC of 9% is close to the level I used previously, and is in line with the range recommended by valueinvesting.io.

Consensus revenue estimates are available for the next five years. With annual revenues of about $400 billion, the company faces a major problem related to the “law of large numbers.” Therefore, I expect a modest 5% CAGR for the years following fiscal 2028. Given all the secular challenges AAPL faces, I do not expect AAPL to expand its 19.3% TTM FCF ex-SBC margin.

Author’s calculations

According to discounted cash flow simulations, the company’s fair value is about $2.1 trillion. This is approximately 30% less than its current market capitalization of just under $3 trillion. Therefore, AAPL is significantly overpriced, based on my assumptions.

Risks to my bearish thesis

Betting against one of the most successful companies of the 21st century is extremely risky. Apple has huge financial resources to hire the best people and the brightest engineers who will be able to deliver an amazing new product. The failure of the Vision Pro indicates a crisis of creativity at Apple, but for one of the world’s biggest companies, there’s always the potential for a great comeback.

As Warren Buffett once said, the stock market is a short-term voting machine. This means that the stock price is highly dependent on headlines and buzzy sentiment. The recent rally following the announcement of the record buyback package proves this theory as earnings analysis suggests there are no reasons to be bullish. However, this buyback-driven rally could continue for a while.

Apple’s upcoming major event called WWDC 2024 could be another positive short-term catalyst for the stock price. The company is expected to unveil the new iOS 18 operating system during the event that will be held next week, and experts expect the company to integrate generative artificial intelligence features into it.

minimum

In conclusion, Apple stock is still a “strong sell” for me, especially after the recent rally. There have been no positive developments except for the standard buyback plan and the introduction of the new iPad into the market, where competition is rapidly intensifying. The secular challenges that Apple faces are clear to me, and even the biggest fan of its stock, the great Warren Buffett, seems to recognize these threats. Furthermore, the stock is significantly overvalued.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.