Evening pictures

Generational market peaks like 1929, the Nifty Fifty of the 1970s, and the tech bubble of 2000 are often characterized by a combination of blue-chip stocks with parabolic charts and irrationally excessive return expectations. In today’s market, there are 7 great stocks, and to a lesser extent grade, large-cap value-weighted indices such as the S&P 500 (spy(and Nasdaq 100)QQQ), seems to have reached its peak. Although not very popular, there is great wisdom in investing in attractive value investments found in less popular sectors and asset classes where investors are not flocking regularly. Specifically, small-capitalization stocks, value stocks, international stocks, emerging market stocks, and commodity stocks, as well as commodities and money markets, provide better return profiles than 7-weighted index ETFs or ETFs like SPY and QQQ.

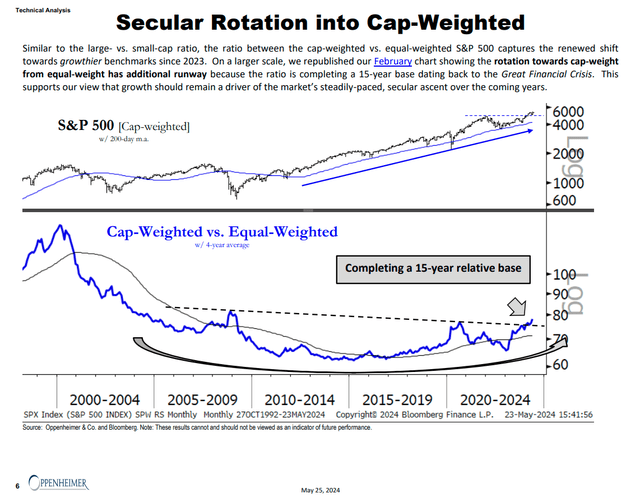

The chart below, drawn by OPCO’s Ari Wald, shows that the relative performance is equal The S&P 500 weighted index rises against the market cap-weighted index. This kind of new leadership, outside of mega-cap stocks and cap-weighted indexes, should emerge and continue in the years ahead.

Improving equal weight versus maximum weight for the S&P 500 Relative Strength Index (Openhiemer & Co. Ari Wald)

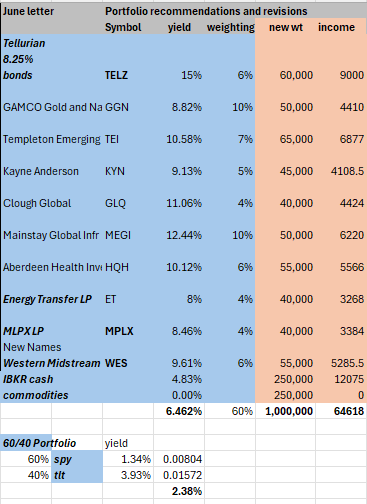

Moreover, the chronic decline in interest rates and inflation, which began in 1981, almost ended in 2020 with inflation and higher interest rates. Investment strategies, such as a 60/40 equity-bond allocation, no longer provide the compelling returns they did in 1981 and in the decades since. Thus, we see the wisdom in allocating 25% cash, 25% commodities, 25% stocks, and 25% bonds to retirement assets and retirement income over the 60/40 strategy popular at the heart of many financial plans and investment portfolios.

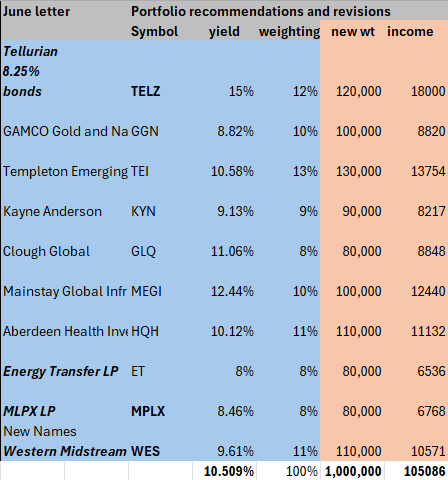

We applied our unconventional investment view to the income portfolio and created a portfolio of stocks and bonds with a 10.5% return and moderate risk. This unconventional portfolio invests in high-yield closed-end funds that trade at a discount to net asset value (NAV), Master Limited Partnerships, and high-yield bonds. Depending on the individual and their risk tolerance, a portfolio like this could be a 50% core stocks and bond allocation in a 25/25/25/25 portfolio. By adding a 25% allocation to a 4.83% money market fund and a 25% allocation to non-yielding commodities, our hypothetical 25/25/25/25 portfolio would yield Yield 6.46% and enjoys more flexibility and inflation protection compared to a hypothetical 60/40 portfolio – 60% SPY and 40% TLT – which would yield 2.376%.

Portfolio Weighting and Portfolio Returns 10.5% (Income Growth Advisors)

Below is a 25/25/25/25 portfolio with 25% allocated to Interactive Brokers Money Market yielding 4.83% and 25% to commodities that yield nothing. At the bottom of the chart, we have calculated the return of SPY and TLT in a 60%-40% allocation to represent the 60/40 portfolio return for comparison purposes.

25/25/25/25 portfolio with 10.5% basis (Income Growth Advisors, LLC)

Portfolio investment with a return of 10.5%

- TELZ is the TELORY Baby Bond series. The bonds mature on November 30, 2028, at $25 per bond and have a coupon of 8.25%. The bonds are trading at $13.90 each and have a current yield of 14.83%. Tellurian Inc. is a distressed liquefied natural gas project developer seeking to finance a 27.6 million tons per year natural gas liquefaction facility near Lake Charles, Louisiana. The company’s principals have been involved in the construction of 78% of LNG production facilities in the U.S. The Tellurian project is one of the few projects fully licensed by the Department of Energy and FERC, making it the only major LNG project not hampered by the Biden LNG shutdown. With a nearly 4-year head start versus a greenfield LNG plant and an investment of approximately $1 billion, Driftwood is positioned to secure financing as global energy markets embrace LNG as a transition fuel to address climate, economic and energy security concerns. Last week’s news of its planned sale of its Haynesville properties should it eliminate the more problematic debt associated with Tellurian’s survival, the company will need to announce more transactions such as an HOA for Aethon Energy Management LLC (Aethon) to acquire 2 MPTA LNG. Aethon, a large Louisiana exploration and production company partly owned by EIG Partners, a large international energy investor, is the type of partner Tellurian will need to finance Driftwood. We think these bonds are risky, but they could be a big winner if Tellurian is successful in financing them or if the company is sold.

- The Jamco Gold, Natural Resources and Income Fund (GGN) is a closed-end gold and natural resources fund that writes call options against its positions to add income to its portfolio. The fund yields 8.8% and has a discount to NAV of 1.5%. Historically, the Fund has been positively associated with positive movements in gold prices.

- The Templeton Emerging Markets Income (TEI) Fund is a closed-end mutual fund that invests primarily in the sovereign debt of emerging market countries around the world. The yield is 10.49% and we expect emerging markets to tend to perform well in the coming years as US stock markets consolidate.

- Kayne Anderson (KYN) is an MLP-oriented energy infrastructure closed-end fund that yields 8.89% and has a 14.9% discount to NAV. This fund uses leverage which enhances its return, but can also result in significant downside as occurred during the coronavirus crash in March 2020. We were aggressive buyers of KYN stock in the spring of 2020, and wrote about the rare opportunity in KYN stock in March 2020 in Searching for Alpha.

- Clough Global (GLQ) is a closed-end fund that trades at a 16.75% discount to NAV with a yield of 11.03%. GLQ is an attractively priced way to invest in many of the large-cap technology stocks we’ve written about with less risk. Microsoft, Amazon and Alphabet are the three largest funds in positions and represent 17% of the portfolio. The distributions are more likely to be capital gains than interest income, which some tax-sensitive investors may not like.

- Mainstay CBRE Global Infrastructure (MEGI) is a closed-end fund with a 12.9% discount to NAV and a yield of 11.5%. The company invests in global infrastructure properties typically associated with businesses with perpetual cash flow, but uses leverage that can cause a problem in significant market declines.

- Abrdn Healthcare Investors (HQH) AKA Telka Healthcare Investors is a closed-end fund that trades at a 12.75% discount to NAV with a yield of 14.25%. The fund invests in biotechnology, medical device, pharmaceutical, and free cash flow generating companies with smaller caps. HQH owns Amgen, Regeneron, and Gilead Pharmaceuticals, which represent about 20% of its portfolio.

- Energy Transfer LP (ET) is a leading master limited partnership yielding 8.18%. It owns energy infrastructure assets in the United States including more than 20,000 acres of natural gas pipelines. ET is rumored to be a potential suitor for Driftwood LNG because its Lake Charles LNG facility has been affected by Biden’s pause and Energy Transfer would be well-positioned to move cheap natural gas from the Permian Basin to Driftwood. MLPs pay distributions, not dividends, so they cannot be owned in retirement plans and require a K-1 to be filed every year.

- MPLX LP (MPLX) is a subsidiary of Marathon Oil’s Master Limited Partnership. It yields 8.36% and also requires filing a K-1 annually to distribute the tax benefits. MPLX manages energy infrastructure and logistics assets in two sectors, logistics and warehousing, and assembly and processing. Marathon Oil was purchased last week by ConocoPhillips.

- Western Midstream Partners, LP (WES) is a master limited partnership focused on natural gas and has a yield of 9.38%. Bond expert Bill Gross has cited WES as an attractive income idea, and we like the focus on natural gas – the cleanest of the three fossil fuels that will be needed over the next few decades.

Risks:

- Closed-end funds may use leverage, which may result in a margin call at the fund level in extreme market conditions.

- The liquidity of some mutual funds makes buying and selling large positions expensive, as large purchases or sales may move the central fund’s target price.

- TELZ are high yield bonds. The underlying company, Tellurian Inc., may go into bankruptcy, although we feel its assets significantly exceed its liabilities and would likely be sold before filing for bankruptcy.

Conclusion:

The benefit of higher inflation is the high-yielding investment opportunities now available. The ability to invest $1 million and generate approximately $100,000 per year in income is very compelling after a decade where money markets and bank deposits were virtually zero. For non-traditional investors contemplating retirement, select closed-end funds, master limited partnerships, and some distressed corporate bonds can provide attractive income-generating investments that can help achieve retirement planning goals.

Unfortunately, the liquidity of this portfolio is limited such that institutional investors cannot take advantage of these specific opportunities at any scale; However, this letter demonstrates the benefit of non-traditional income opportunities and investing in securities on the road less traveled. Whether this approach makes “all the difference” depends on understanding the details of each security.