Morsa Images/DigitalVision via Getty Images

Investment work

I recommend a Buy rating for Progyny, Inc. (Nasdaq:PGNY) when I wrote about this in mid-March of this year, as I continued to view the long-term growth outlook as attractive. Based on my current expectations and analysis, I recommend Buy rating. The main update to my hypothesis is that I do not believe that weakness in 1Q24 revenue is indicative of long-term structural weakness in growth. Historical ART cycles in the US suggest a strong long-term growth trend, and any decline is usually met by a strong rebound afterwards, which gives me confidence that we will eventually see a recovery. There are also leading indicators that usage is already back on track.

review

Regarding a recap of the latest results, PGNY reported earnings in early May, which saw revenue grow 7.6% to $278 million, beating Street expectations of $290 million. Collapse Growth and fertility benefits services saw growth of 8.1% to $169.8 million and pharmacy saw growth of 6.9% to $108.3 million. Gross margin decreased 18 basis points to 25.7%, while EBITDA margin expanded 14 basis points to 18.1%, which amounted to $50.3 million on an absolute basis. Overall, 1Q24 results were disappointing, with revenue performance underperforming due to weak usage, which sent the stock down significantly, from ~$32 to ~$26 today. I talk below about why I think this loss is just a one-time issue and why I still think the stock is trading at very attractive levels.

Regarding the error, my point is that it was not due to anything structural. The year started well, with usage rates in January and February being in line with 2023. However, usage saw a sharp decline in mid-March, resulting in lost revenue. I think what’s happened is that a lot of patients are adjusting their expectations about access to maternal health care after the Alabama Supreme Court ruling, especially in states that have more restrictive laws on women’s reproductive rights. In other words, I think usage rates are delayed and not permanently decreased. Once there is more clarity (the recent Senate bill should help clear up any confusion), in fact, the administration has already noted that utilization rates in April were stable and improving from low levels. It is also important to note that although usage has declined in states with more restrictive laws on women’s reproductive rights, there has been no decline in demand for PGNY fertility benefits among employers in those affected areas. This is crucial because it means that employees can continue to access affordable IVF (more potential demand and future use).

My prediction is that PGNY will see growth accelerate in the coming quarters, as there are many indicators that demand remains strong. First, the year-to-date pipeline remains very strong based on early indicators. It was specifically noted that the pipeline has become more active compared to last year. It is worth noting that the pace of industry adoption appears to have picked up as follows: (1) PGNY is seeing more early commitments from a strong group of people not mentioned last November; (2) PGNY saw strong commitments in healthcare, automotive, manufacturing, etc. My view of the increasing adoption rate is supported by the fact that 45% of large employers offered IVF coverage to their employees, up from 23% in 2019. On an aggregate basis, the statistics show a 10-point improvement in IVF treatment coverage in 2023 versus 2020.

Conditionally, What’s Not Now represents the majority of the early commitments we have received, and 2024 is proving to be no different with strong early commitments from leading brands in healthcare, automotive manufacturing, travel and leisure, media, as well as many government and private organisations. Local government residents. Q1 24 earnings call

One other indicator that also suggests that demand is still good is that engagement has continued at higher levels than in 2022. This suggests that the current increase in adoption and growth in the pipeline is not a freak one-off event.

What gives me comfort in focusing on the long term is that demand for IVF has been historically resilient, and I don’t see major catalysts that will change this trend in the future. The Centers for Disease Control and Prevention has historical data on ART cycles, and based on that data, ART cycles have continued to rise over the past 20 years, and the only periods when growth turned negative were during the coronavirus and subprime mortgages. But growth I immediately revived After every crisis ends. During subprime, ARV cycle growth turned negative in 2009 and 2010, but rebounded back to 3.2% growth immediately in 2010, a similar growth rate seen before the crisis (the average growth in the period was 2005-2008 3.7%). The same is true for the Covid period, which saw negative growth of -1% in 2010 but rebounded to ~27% growth in 2021.

evaluation

Author’s work

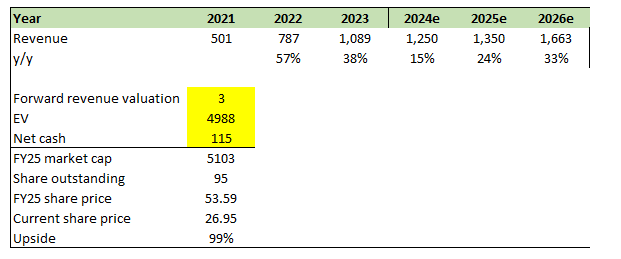

My view on PGNY has not changed. I still believe growth can be accelerated back to above 30% eventually as all short-term problems disappear and the economy rebounds. The problem is when growth will accelerate again. Previously, I had expected growth to reach more than 30% in FY2025, but to be more conservative today, given the governing issue and persistently weak economic outlook, I have postponed my estimates by one year. Using revised FY24 revenue guidance of $1.25 billion at the midpoint (implying 15% year-over-year revenue growth), I projected a linear expansion of year-over-year growth rates to 33% in FY26, meaning PGNY would generate $1.66 billion in revenue in FY26. I don’t think this is a huge hurdle, as this business has grown 38% in just the last year.

The market should react favorably to growth accelerating over the years, and I believe PGNY should trade at least 3 times forward revenue, which is where it traded in FY23 when growth was over 30%.

Based on these assumptions, I have a price target of around $54 in FY25.

risk

With the volatility in usage, I think investors will be more conservative in their estimates, especially with guidance that includes a recovery in the second half of 2024. Until PGNY shows that usage is improving on a reported basis, the stock may be range-bound in the near term. Also, depending on historical cycles, if the economy continues to slow or turns into a recession, PGNY will be directly affected.

Final thoughts

My recommendation is a Buy rating despite the revenue loss in 1Q24. I believe demand has been delayed simply by recent legal uncertainties, not by structural factors. I remain a believer in the long-term outlook for the business as historical trends show that demand for IVF is resilient, with strong rebounds following the economic downturn. There are also leading indicators that a rebound in usage has already begun.