Sakorn Sukasimsakorn

Investment thesis

I recommend buying Cosan shares (New York Stock Exchange: KXAN) after the release of 1Q24 results on May 29. The market was already expecting a weak result, as the subsidiaries had already released their results.

However, I have identified some subtleties Signs that the company is starting to show a feeling of need to reduce its operations. As I said in my country Coverage initiation report Published April 1 Moving from the investment cycle to the cash generation cycle can unlock value.

Review of COZAN’s results in the first quarter of 2024

Cosan is the controlling holding company of Raízen, Rumo, Moove and Compass. We will talk in detail about the results of each subsidiary below and then comment on the combined results of the holding company.

Ryzen 1Q24 – lower than expected

Raízen, from the Sugar and Ethanol sector, is the subsidiary that contributes to Mostly for Kozan’s operating results of 51%. In the first quarter of 2024, Raízen’s results fell short of expectations, as did its revenue, which slowed 2% in the year-over-year comparison to $10.7 billion.

The company’s EBITDA slowed 43% in the year-over-year comparison to $784 million. The company witnessed an unstable price scenario in this quarter in both renewable energy and sugar companies. This was reflected in lower cost and margin loss.

The prospects are mixed, as Cosan continues to invest heavily in Raízen (77% of total investments), with the company potentially becoming one of the world’s most relevant companies in the energy transition. However, there are still no expectations of a decline in investments or the start of a strong cash generation cycle.

Romo 1Q24 – Better than expected

Rumo, in the rail sector, reported good results in the first quarter of 2024. The company had a good 32% year-over-year expansion in net revenue to $620 million, and 43% growth in EBITDA to $340 million.

Tariff increases of 23% and 11% on the North-South network, respectively, contributed to increased revenues, as well as cost control resulting in the company achieving an EBITDA margin of 53.7% (+420 basis points year-on-year ).

The outlook is good for the company, which offered leverage of 1.7 times (slightly better than in the previous quarter). Finally, net income was $74 million, which multiplied the previous year’s net income by 5. Romo continues to benefit from working in agribusiness, the most durable sector in Brazil.

Compass 1Q24 – Passive but accurate

Compass, the gas distribution sector, released results below expectations, with the company accounting for 12.5% of Kozan’s operating results. Gas distribution volumes during the quarter were stable at 13.2 million cubic meters per day, but unit margin fell by 12% to $148.

As a result, EBITDA was $179 million, but the company reiterated EBITDA guidance of between $880 million and $940 million. Finally, leverage increased from 1.3x to 1.45x.

The company notes that operational deficiencies were specific, such as residential consumption being lower due to higher temperatures. Compass also intends to monitor the developments of the Rio Grande do Sul tragedy in its operations, but does not believe there will be serious damage to the operation.

MOV 1Q24 – stable

The last subsidiary relevant to Cosan’s business is Moove, in the lubricants segment, which contributes 4.6% of Cosan’s operating results. In the first quarter of 2024, Moove’s results were stable.

The company delivered stable sales volume in year-over-year comparison, while gross profit increased by 2% YoY due to good control of SG&A expenses. In my opinion, Moove should continue on a good trajectory of operational expansion and profitability. I still believe the company will remain one of the smallest contributors to Cosan’s operating results.

Consolidated result

After comments on both companies, Kozan generated revenue of $1.96 billion. (-0.5% quarterly and +3.4% yearly/year). EBITDA reached $559 million (-22% QoQ and +0.4% YoY) and finally the company posted a net loss of $38 million, although better than the Q1 2023 loss of $178 million.

I think today’s COZAN results focus more on the path of leverage and efficiency in investments, and in this sense, we have had positive developments on this issue.

Allocate capital efficiently

Net corporate debt (former Vale stock and preferred stock) fell by about $40 million to $4.54 billion at the end of the first quarter of 2024. This measure does not include the value of Kozan’s investment in Vale (which I discuss below). Cozan has a strong cash position of approximately $760 million, well above maturities in the coming years ($116 million in 2024 and 2025).

What attracted the most attention during this period was the investment management of Vale (NYSE:VALE). Kozan has paid 100% of the debt related to the collar (derivatives), in addition to the derivative financing of the collar.

As a result, Kozan’s direct investment in Vale increased to 4.15% (from 1.57% in the first quarter of 2023), and the collar decreased to zero (from 3.35% in the previous year). In brief, Cosan’s exposure to Vale was reduced in May 2024 to a direct share of 4.15% and an additional call spread equivalent to 1.43% (it was 1.60% in Q1 2023).

This simplification of investing is very positive in my view. One of Kozan’s discount points is the complexity of the issue, given that the holding company already has a very diversified business and is still making very aggressive investments.

The company’s sense of urgency in adjusting the investment is positive in my view, which is why I give the benefit of the doubt and reiterate my recommendation to buy the company’s shares. Now let’s revisit the valuation metrics.

Rating – cheap

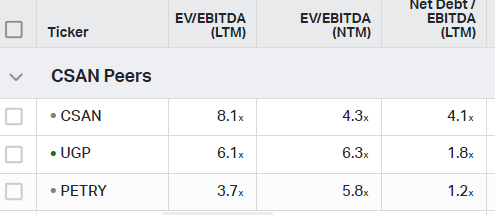

Companies with businesses closest to Cosan are Grupo Ultra (NYSE:UGP) and Vibra (OTCPK:PETRY) in Brazil. I will use the EV/EBITDA multiple again for a comparative evaluation.

evaluation (Quevin)

Well, averaging the pairs, we arrive at an EV/EBITDA multiple of 5.46x. With this, there is 27% upside potential to close the gap between the peer average and Cosan’s EV/EBITDA multiple of 4.3x.

This divergence reinforces my recommendation to buy Cosan shares, but it’s also important to consider that Cosan is the most leveraged among its peers, and reducing its leverage will be key to unlocking value. Now, let’s analyze the risks to the thesis.

Potential threats to the bullish thesis

As I mentioned in my initial coverage report, delays in massive renewable energy adoption and corporate deleveraging are risks relevant to the thesis, and in that context, I’m adding another risk.

Taking too long to realize an investment thesis can be a catalyst for selling pressure on a company’s stock, which already suffers from the added complexity of being a holding company with multiple companies.

Additionally, she mentioned tax reform that could impact dividends. This risk is increasingly evident as the government adopts an aggressive tax hike agenda. The risks facing this thesis are diverse, and investors should analyze them carefully before making their investments.

Bottom line

Although the investment thesis has seen little development operationally. Kozan has shown a sense of urgency to simplify its investment in Vale and reduce its influence, even if only slightly.

In my opinion, the company’s business is very interesting and long-term, and this makes investors more interested in the leverage trajectory and quality of investments than any other operational aspect.

Based on this analysis, I recommend buying Cosan stock. The company has a decent discount on its EV/EBITDA multiple compared to its peers, and should be reduced when the company can reduce its leverage. In my opinion, this will happen, and it will be a great opportunity for investors.