johnnyscriv/E+ via Getty Images

Investment overview

I give Cricut, Inc. a Sell rating. (NASDAQ:CRCT), as I expect demand to remain weak in the near term as the macro environment remains weak. I expect consumer discretionary spending to remain under pressure Decrease in demand for CRCT’s main product (machine), which will have a direct impact on demand for platform services, accessories and materials.

Job description

CRCT is in the business of providing computer controlled cutting machines to home craftsmen so that they can better design and create products to their liking. I have attached a picture below so you can get a better idea of the product CRCT is selling:

Convention on the Rights of the Child

The core business units (segments) are: Product (60% of FY23 revenues) and Platform (40% of FY23 revenues). For reference, previously, the business had three main segments: Connected Devices (26% of FY23 revenue), Platforms (40% of FY23 revenue), and Accessories and Materials (34% of FY23 revenue).

In its most recent quarter (1Q24), reported on May 7, CRCT saw total revenue of $167.4 million, representing a 7.6% decline versus 1Q23; Gross margin of 54.7%, a significant improvement from 42.3% in Q1 2023; EBITDA margin of 20%, which is also a significant rise from 10.9% in Q1 2023; and a net margin of 11.7%, up 670 basis points compared to 1Q23. On an EPS level, CRCT reported $0.09 EPS versus $0.04 in 1Q23.

Negative outlook on business

May investment ideas

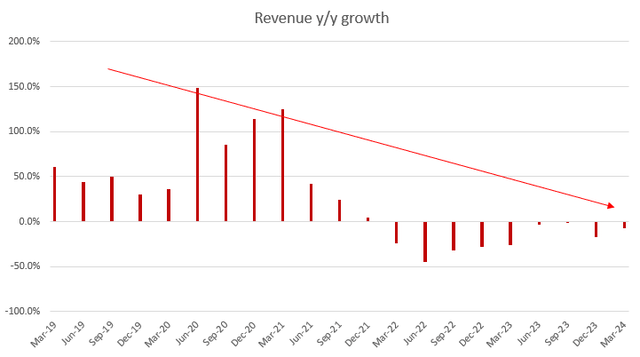

I have a very negative view on the near-term (6-12 months) business outlook. Although profitability has been a very positive point in recent performance, the fact of the matter is that the business is still seeing negative growth, and I don’t see any catalysts that can drive positive growth in the near term.

Starting with the poor macro conditions, my view is that CRCT will continue to feel pressure as consumers’ purchasing power continues to be squeezed, with no near-term view on when this will end. The latest US inflation data shows that inflation remains very steady, and on a 3-month rolling average basis, the economy is back to where it was in the third quarter of 2023. This is really negative for consumer spending because it involves two things:

- The impact of higher interest rates does not appear as much as it should, which means…

- Interest rates will stay high for longer, and the scary part is that the Fed has not ruled out the possibility of raising interest rates further.

May investment ideas

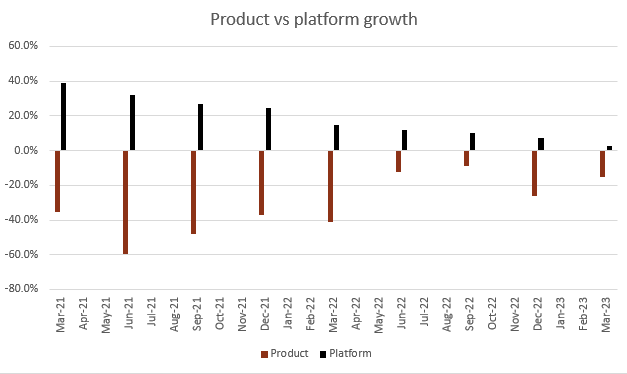

The nature of CRCT’s business is that it is highly exposed to how much consumers are willing to spend on discretionary items. The entire sales model revolves around CRCT selling the main product (the machine). Consumers then subscribe to CRCT to obtain design patterns and purchase tools and accessories to facilitate their cutting operations. In my opinion, weak macro conditions will cause a significant decline in demand for the key product. Note that these machines are not cheap items that cost less than $50. According to the CRCT website, these machines cost from $100 to more than $1,000. The decline in demand has a direct impact on the platform’s revenue as there are fewer customers (fewer product owners) added to CRCT’s customer base, and CRCT’s financials already show this weakness.

May investment ideas

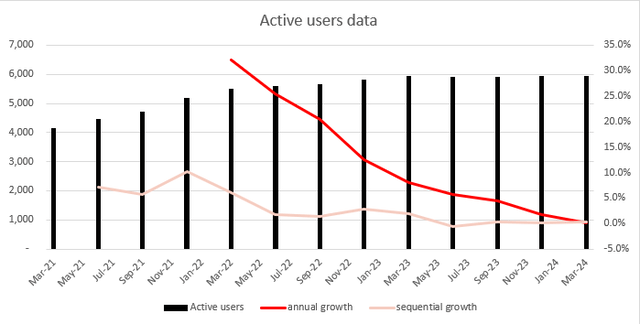

There are also many other signs of weak demand. For example:

- The number of active users continues to slow on a sequential and year-over-year basis

- User engagement over the next 90 days decreased by 5% to 3.5 million

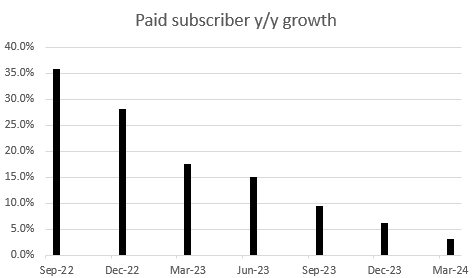

- More importantly, annual growth in paid subscribers slowed for the seventh consecutive quarter, from 35% in 3Q22 to just 3% in 1Q24.

May investment ideas

With all these data points, I think they are enough to prove my point that demand is slowing and is at an inflection point where it could turn negative if macro conditions continue to remain weak. Management’s comments on Q2 2024 performance showed no positive signs of recovery or stabilization, noting that retailers remain cautious about restocking and that they expect weak consumer spending trends to continue.

May investment ideas

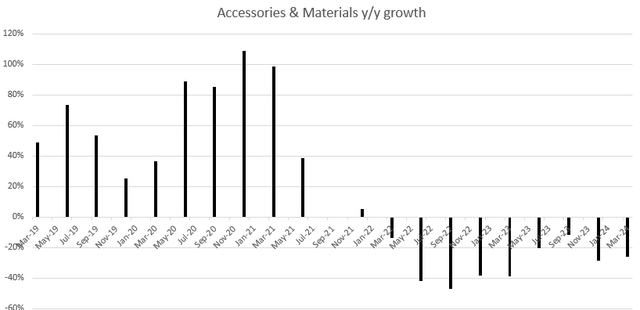

Aside from the overall weakness, management has also described competition as a major constraint for the accessories and materials sector, and this is particularly worrying. This sector represents about 33% of businesses, and is the sector with the lowest barriers to entry (there are thousands of arts and crafts stores from which consumers can purchase). I expect this sector to continue to reduce overall growth as it faces not only the impact of a weak macro backdrop (lower product sales impact demand for accessories and materials) but also from competition.

Puzzled by the new capital return program

I’m also very puzzled by the new capital return program, which includes a $50 million stock buyback authorization, a special dividend of $0.40 per share, and a new recurring semi-annual dividend of $0.10 per share. This may sound good to shareholders, but my takeaway from this action is that management did not have better alternatives to distribute this amount of cash. I would expect them to reinvest in the business to find a way to revive growth (my concern is that there is no way for CRCT to restore growth even if they deploy capital).

Therefore, even with this capital return program, until I see signs of demand stabilizing or rebounding and fundamental user metrics improving, I will not pivot to the positive.

evaluation

May investment ideas

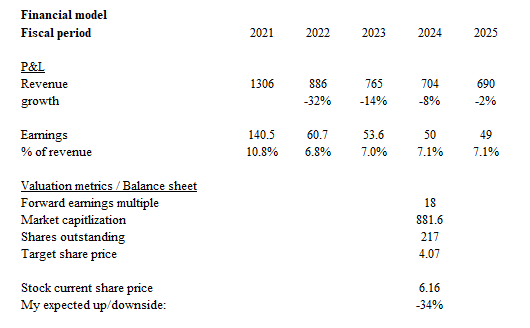

Based on my research and analysis, the expected target price for CRCT is $4.

- I expect revenue to continue to decline for the rest of the year (FY24) at the same rate as Q1 2024, as I see no catalyst to drive growth in the near term. However, I believe the macro backdrop for FY25 should be better than FY24, and CRCT should see some form of recovery. For FY2025, I assumed a decline of 2%, following the same 600bps rise in year-on-year growth (FY24 growth was -8%, 600bps higher than FY23).

- Regarding earnings margin expectations, I give management the benefit of the doubt that it can achieve and maintain FY24 guidance in FY25, given that it demonstrated strong margin performance in 1Q2024.

- CRCT is trading near its historical average multiple of 24x today, which I believe does not accurately reflect the ongoing slowdown in business. Just a few months ago, the stock was trading at 18x forward PE, and I think this is a potential downside that CRCT could face. Assuming CRCT trades at 18x, this means the stock price is around $4.

risk

Since subscription, accessories and materials revenue growth follows connected device sales, higher-than-expected connected device sales would prove my headline estimates too conservative. In particular, Cricut recently launched in several new markets internationally which could lead to faster-than-expected growth.

Conclusion

I give CRCT a Sell rating due to weak demand and outlook. I believe the negative macro environment will continue to pressure consumer discretionary spending, directly impacting the sale of CRCT’s flagship devices. This weakness is expected to translate into fewer platform subscriptions, materials, and demand for accessories. In addition, user metrics show a clear downward trend, which is very worrying. Finally, the new capital return program looks more like a desperate attempt to appease shareholders and does not address the fact that growth is slowing or potentially becoming negative.