feverish

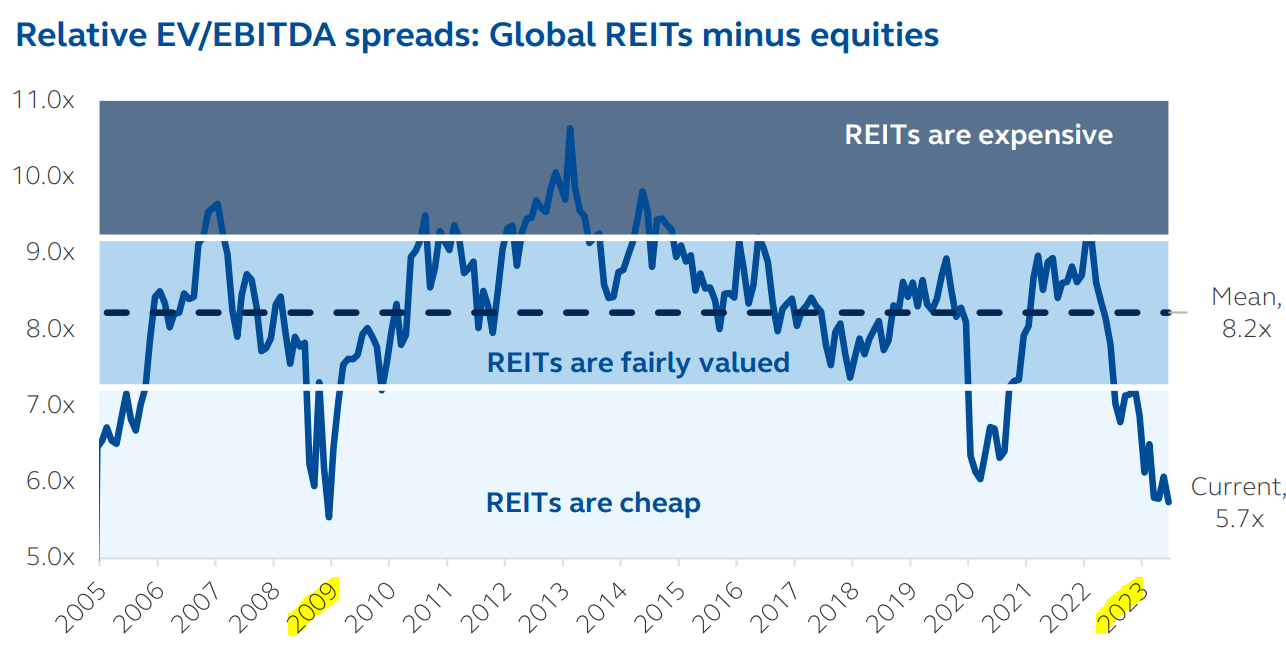

REITs (VNQ) are priced today at their lowest valuations since the Great Financial Crisis:

Key asset management

Historically, it was always a good idea to buy REITs when they were deeply discounted.

I do not think so This time will be different. When you can buy quality real estate for just a few dollars, it’s hard to screw up in the long run.

But just because REITs are opportunistic doesn’t mean they’re all worth buying. This is a broad and versatile sector that includes more than 1,000 companies around the world, and the fact that two companies share the abbreviation “REIT” does not mean that they have anything in common.

I’m very bullish on REITs, but I’m still objective enough to realize that many of them are likely to disappoint over time.

here Here are three REITs I would avoid today:

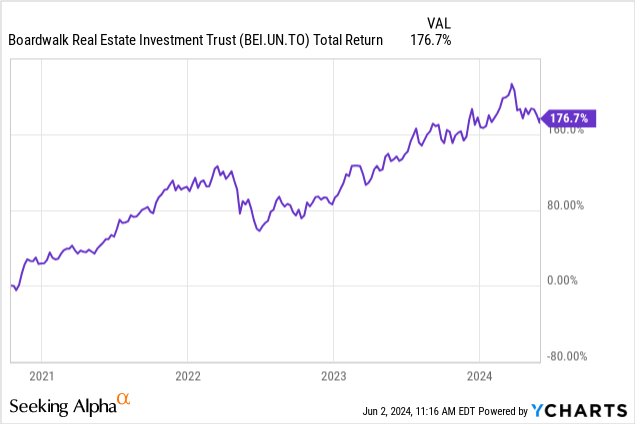

Boardwalk is a Canadian real estate investment trust that owns mostly residential communities.

This was once our largest investment in a Canadian REIT, and we expected it would rise over 100% in October of 2020.

High return owner

Boardwalk REIT

That’s how cheap a REIT is!

But four years later, that upside has now materialized and the REIT is expensive compared to its peers.

Historically, Boardwalk has tended to trade at a discount to most other REITs, because it mostly owns older Series B properties in more energy-sensitive markets.

But right now, its market is performing particularly well, and this has led to it significantly outperforming its peers, closing the valuation gap.

For once, it’s the opposite. It is a boardwalk that is priced at an excellent rating. It currently trades at an implied cap rate of approximately 5%, even as blue-chip REITs such as Camden Property Trust (CPT) trade at an implied cap rate of 6.5% in the US. This is despite Camden enjoying:

- Much larger scope

- Obtaining an investment grade rating of A-

- Better long-term track record

- Superior development capabilities

- Market exposure is safer

Costar

I have limited capital and for this reason, I sold my position in Boardwalk and reinvested the proceeds in some of its cheaper peers.

I wouldn’t mind owning it again someday in the future. I have met their management and really like their approach. Its valuation is not attractive compared to other REITs in the market today.

Universal Health Income Trust Fund (UHT)

Many investors buy Universal Health Realty for one main reason:

Today it is priced at a dividend yield of 7.7%, despite its ability to increase its dividend for 35 years in a row.

This is one of the longest periods of dividend growth for any REIT, and it rarely trades at such a high yield, so why not buy it now?

Seeking alpha

Here are two main reasons:

1) I expect it will reduce its dividend. Currently, its payout ratio is roughly 90%, leaving little room for error as it faces declining cash flow from tenant issues, rising vacancy, growing capital expenditure needs, and rising interest expenses. I know the REIT raised its dividend in December 2023 and some people like to think that “the safest dividend is the one that was just collected” but note that the dividend increase was only 0.7%. Its purpose was only to keep the line going. WP Carey (WPC) did the same shortly before cutting its dividend, alienating its shareholders, who viewed the cut as a betrayal by management. I fear the same thing will happen here in the near future.

2) The biggest problem is that the company’s valuation is meaningless to me. It is actually priced at a premium compared to its close peer, Healthcare Realty (HR), despite: (1) having weaker assets, (2) having a worse balance sheet, (3) being managed externally, which leads to interesting conflicts, (4) ) and has worse growth prospects.

We used to own UHT, but it exited in late 2022 at $47.76.

I’m glad we did, as it is trading $10 lower today.

Getty Realty (GTY)

Getty Realty is one of the most popular net lease REITs and I believe this is largely due to two reasons:

1) It mostly owns rental properties for gas stations/convenience stores, which are viewed as recession-proof. Investors also seem to like these specific properties because they have a sense of familiarity with them, as they visit these properties regularly themselves.

2) It offers a dividend yield roughly 100 basis points higher than its net lease peers, such as Realty Income (O), Agree Realty (ADC), and NNN REIT (NNN), despite their ability to grow at roughly the same pace over the course of the year. The long-term:

| Profit return | |

| GT | 6.5% |

| Hey | 5.9% |

| Adc | 5% |

| Nnn | 5.4% |

Why don’t I buy it?

There are three main reasons.

The first is that I fear that many of their properties will suffer permanent destruction of their long-term value due to the rapid transition to electric vehicles. Before you comment “yeah, but EVs also need to charge and these are convenience stores…” note that I get that. But there are better places to charge electric vehicles than these convenience stores. Most people charge them at home in most cases, and if they’re out and about, they’ll prefer to charge their electric vehicle while at a grocery store, restaurant, or entertainment venue rather than waiting at a convenience store. Therefore, I think we will not need this number of gas stations anymore.

I also realize that switching to electric vehicles will take a long time, but real estate investors are focused on the long term, and if there is a risk that your property will be vacant in 20 years, the current value should reflect that.

Finally, I am also afraid that redeveloping these properties into other uses will be very expensive. I used to work at a private equity firm, and we used to avoid gas stations for this exact reason. If there are or have been leaks in the past, mitigating any environmental damage can be very costly.

Getty Real Estate

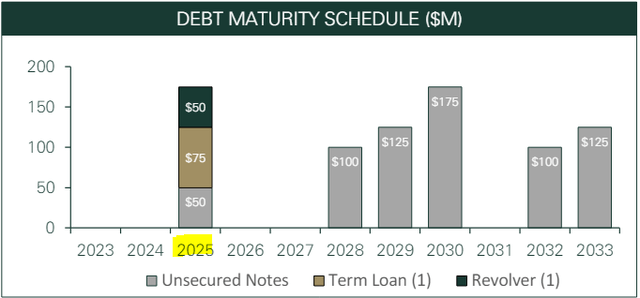

The second reason is that the company has a large wall of debt due next year, and this will likely result in a significant increase in interest expense:

Getty Real Estate

Some of its close peers have done much better with their balance sheets. For example, NNN REIT has an average debt maturity that is twice as long as Getty Realty.

The final reason is that you do not get a lower rating for accepting such high risks. Getty today is priced at similar valuation multiples to its close peers even though it has a weaker balance sheet, is more exposed to rising interest rates, has a much less diversified portfolio and is more at risk of declining property values and rents throughout the year. The long-term:

| Multiple FFO | |

| GT | 12.6x |

| Hey | 12.5x |

| Nnn | 12.5x |

So, even if you disagree with my opinion on EVs, it still doesn’t make sense to buy Getty. You should be getting a lower valuation reward for taking this risk, but you’re not.

Concluding note

You can dramatically improve your portfolio’s risk-reward ratio by being selective, and these three REITs are great examples of that. In all three cases, you’ll likely earn better returns with less risk if you simply invest in some close peers instead.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.