Editorial by Sue Thatcher/iStock via Getty Images

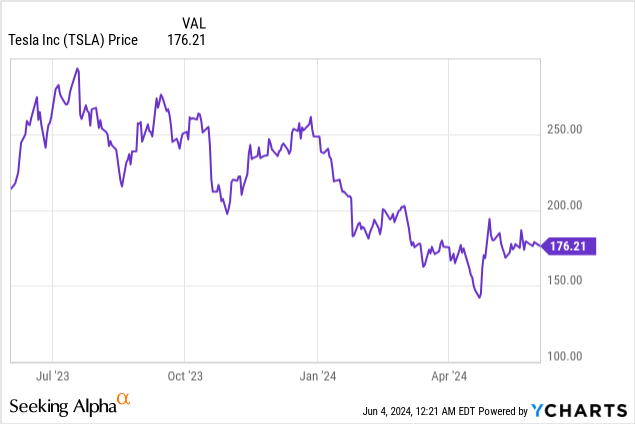

Tesla company (Nasdaq: Tesla) has never been a passive stock. The world’s leading manufacturer of electric vehicles (“EVs”) has long been a lightning rod for the press, and the latest buzz is this June 13 votes in favor of CEO Elon Musk’s proposed $56 billion compensation package – where rejection This package is expected to cause Tesla stock prices to decline.

But when we speculate on near-term engine results, we overlook the real fundamental progress Tesla is making, even in a difficult operating environment. With the stock still down roughly 30% so far, I still see an opportunity for investors to load up here, especially if the vote heads south.

I last wrote a bullish article on Tesla earlier this year, in January, when The stock was still trading near $200 per share. At the time, I argued that Tesla’s lower prices — though certainly a headwind to near-term gross margins and profitability — would make the company more attractive vis-à-vis other resurgent electric and hybrid car makers. this year.

Now, with Tesla shares still lower than they were at the beginning of the year, I’m renewing my contract He buys Call Tesla – In addition, there are a few positive green light catalysts that can be counted in the company’s favor.

In short: Tesla has always been a volatile stock, especially when it comes to key milestones like earnings, production updates, and flashy shareholder votes. But as a long-time believer in electric vehicle adoption and Tesla’s brand and technology advantage in this space, I’m sticking with it.

Gross profit margin stabilizes, with further increase through greater adoption of FSD

Much ado has been made over the past year about Tesla’s price cuts. The company has cut prices, sometimes multiple times in the same quarter, which has always led to investor backlash (particularly to price cuts made in China, where the company competes with much cheaper domestic alternatives).

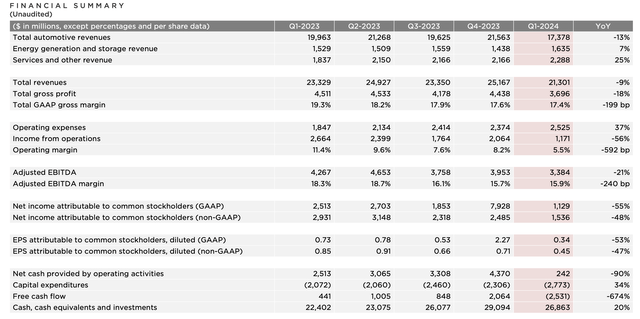

But amid this round of price cuts, we saw in Tesla’s first-quarter results that the company achieved sequential gross margin stability.

Tesla directional gauges (Tesla Q1 Shareholder Group)

Q1 gross margins of 17.4% were down two points year-over-year, compared to an eight-point year-over-year decline in Q4, and were down just 20 basis points sequentially from Q4 as well.

We note that there are a number of positive drivers for the recovery in gross margin, in addition to vehicle production efficiencies, which will naturally gain over time. It’s worth noting that Tesla recently began free Full Self-Driving (FSD) trials for buyers of new Teslas as well as existing Tesla owners starting in March, to encourage further adoption of the $8,000 feature.

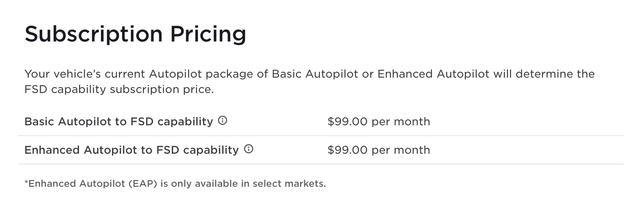

Likewise, it is worth noting the fact that FSD is now available in a number of markets for a subscription of $99 per month, which is Much lower barrier to entry than the $8,000 sticker price. We as consumers have now been trained to a subscription model, and many expensive purchases (including smartphones in particular) have moved to a monthly payment model.

Tesla FSD subscription (Tesla.com)

In my view, offering both free trials and subscription pricing will boost Tesla’s FSD attach rates on new vehicles, which is essentially a “free” lever for overall margin leverage.

Accelerating timeline for next generation vehicles

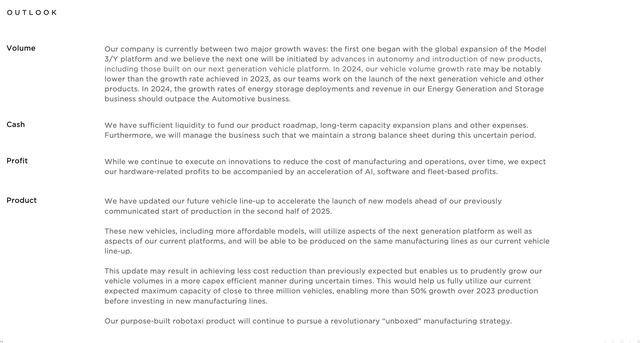

In my view, Tesla also doesn’t get enough credit for the anticipation building around the launch timing of its lower-priced next-gen vehicles. We now know that Tesla believes it is between two major growth phases, the second of which will be unleashed when cheaper cars become available on the market.

Comment on Tesla’s anecdotal forecasts (Tesla Q1 Shareholder Group)

As seen in the company’s future commentary above, the company indicates that it expects to begin production of these new vehicles by early 2025. It’s also important to note that Tesla currently has a proven ability to increase vehicle volumes by at least 50% above 2023 levels when these new vehicles are brought online before investing in any new manufacturing lines. So, right now, the gross margins we’re seeing include built-in idle costs that are booked for these new vehicles.

Per Elon Musk’s Roadmap Comment on Q1 Earnings Call:

We also continue to expand our AI training capacity in the first quarter, sequentially more than doubling our training compute. In terms of the new product roadmap, there has been a lot of talk about our upcoming vehicle line in the past few weeks. We’ve updated our future vehicle lineup to accelerate the launch of upcoming new models, which we previously mentioned would go into production in the second half of 2025, so we expect it to be more like early 2025, if not late this year. These new vehicles, including more affordable models, will use aspects of our next-generation platform as well as aspects of our existing platforms, and will be able to be produced on the same manufacturing lines as our current vehicle lineup. So it doesn’t depend on any new factory or huge new production line. It will be manufactured on our existing production lines more efficiently. We believe this should allow us to reach over 3 million vehicles when fully achieved.”

Valuation metrics still look reasonable, especially when there are still a number of upside margin catalysts on the horizon

If we judge Tesla based on near-term earnings metrics, many would consider the stock to be expensive versus the broader market, but in a longer-term context, I believe Tesla is actually trading at reasonable levels even versus later metrics.

With current stock prices hovering around $175, Tesla is trading at a market cap of $552.4 billion, and when we strip out the significant net cash of $24.0 billion in Tesla’s most recent balance sheet ($26.9 billion in cash, offset by a relatively modest of $2.9 billion in outstanding debt), resulting from it Enterprise value: $528.4 billion.

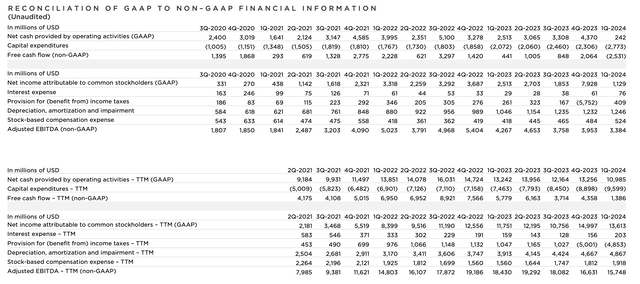

As shown in the chart below, Tesla’s TTM adjusted hours EBITDA of $15.7 billion. In contrast, Tesla stock is trading at 33.6x EV/TTM Adjusted EBITDA.

Tesla trailing profitability metrics (Tesla Q1 Shareholder Group)

We can say that Tesla has reached a low point in terms of profitability, having just gone through a round of price cuts. We have already discussed the potential for increased adoption of FSD (from free trials and subscriptions) to boost gross margins. Besides the rebound in sales, another key factor to expanding profitability is the company’s recent decision to lay off 10% of its headcount. These moves are expected to generate at least $1 billion in annual savings.

Main sockets

Amid the short-term volatility, I continue to see a number of positive catalysts for Tesla, including in particular an accelerating roadmap for next-generation vehicles. Take advantage of the decline in stocks this year to build a long-term position here.