jewhyte

Chevron stock has outperformed amid recent concerns

Chevron Company (New York Stock Exchange: CFX) Investors have had a challenging few weeks as Crude Oil (CL1:COM) (CO1:COM) futures continue to suffer from bearish market sentiment. OPEC+ extension of its voluntary reductions It also sent mixed signals to the market, with plans to “begin unwinding production cuts as early as October.” As a result, the caution seen by oil investors was justified as WTI futures peaked in early April 2024. Accordingly, oil futures have fallen by more than 15% since then, threatening to enter another bear market.

Despite the clear negative sentiment spread throughout the Energy (XLE) sector, CVX stock has outperformed the S&P 500 (SPX) (SPY) since CVX’s previous bullish update in March 2024. So, it’s safe to say that Chevron investors didn’t particularly care. Not necessary Noticeable weakness in oil futures.

Investors are likely confident of Chevron’s strong first-quarter production performance and confident medium-term production outlook. Furthermore, the recent shareholder approval of Hess Corporation (HES) to acquire Chevron has reduced one of the remaining hurdles to expanding Chevron’s ambitions in Guyana. However, clarity on Chevron’s arbitration with ExxonMobil (XOM) is not expected until at least the fourth quarter. However, Chevron management is confident that “Exxon’s rights of pre-emption do not apply to the Hess deal.”

As a reminder, Chevron’s first-quarter earnings announcement was a mixed report. Chevron recorded a significant 12% year-over-year increase in total average production. However, lower realizations in Chevron’s natural gas segment and downstream refining margins impacted CVX’s adjusted EPS of $2.93. Despite this, Chevron’s ability to beat Wall Street estimates suggests that the market has already reflected sufficiently low expectations.

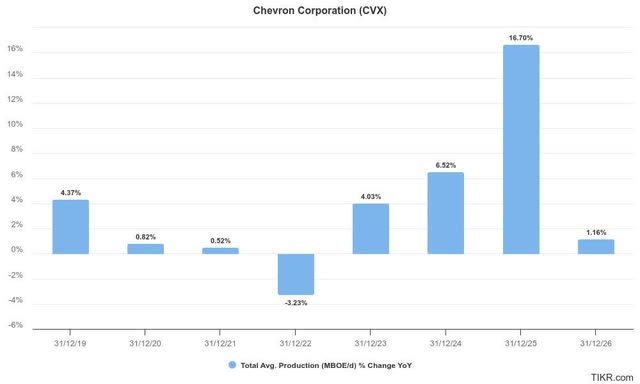

Strong production growth forecast for Chevron

Total Average Chevron Production Estimates (MBOE per day) (TIKR)

As seen above, Chevron’s production is expected to remain in a growth phase, cushioning the downside in commodity price volatility. Despite this, Chevron’s management has pledged to remain disciplined in capital allocation and pursue profitable growth in its portfolio of high-value assets.

Therefore, Chevron is well positioned to leverage its asset base in the Permian Basin and DG Basin. Production remained resilient in the Permian Basin, reaching 859,000 barrels of oil per day in the first quarter. In addition, DJ Basin also contributed to a strong quarter, delivering 400,000 barrels of oil per day last quarter. These are high-quality assets in Chevron’s low-cost portfolio, helping to achieve “high cash margins and low breakeven barrels.”

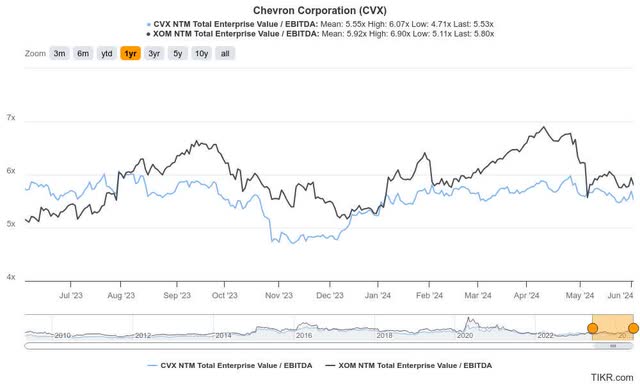

A positive outcome in the Hess case could lead to a rise

CVX vs. XOM (TIKR) Ratings Comparisons

Given the current uncertainty surrounding Chevron’s acquisition of Hess, I estimate that the market may revalue CVX to a higher level if the arbitration outcome favors Chevron. Additionally, the valuation divergence between CVX and XOM has closed significantly over the past month, suggesting that buying sentiment on CVX has remained resilient.

Therefore, CVX’s rating grade of “C-” indicates that it is not expensively valued, with the possibility of a rerating if we obtain a positive outcome in its arbitration with Exxon.

Despite my optimism, I must emphasize that the underlying oil futures have failed to maintain their consolidation area above the $75 support level. Accordingly, WTI futures fell to $73.4, as the market became increasingly concerned about potential increased supply risks as OPEC+ is expected to roll back production cuts. Therefore, if oil futures fall in a subsequent bear market, this could cause downward volatility in CVX. As a result, implementation risks could increase for Chevron to increase production more aggressively to mitigate price declines if Saudi Arabia’s influence on OPEC+ is likely to weaken, leading to a forecast of a potential oversupply situation.

In addition, the long-term investment in Chevron must be balanced against the potential long-term decline in oil demand as the world transitions to renewable energy technologies. Chevron confirmed that it expects to “allocate approximately $10 billion to its new energy business.” However, the return on investment in these endeavors is likely to remain uncertain in light of emerging developments. Despite this, Chevron’s commitment to resume its $17.5 billion annual share buyback cadence following the completion of the Hess acquisition would assure investors of its financial discipline.

Is CVX stock a buy, sell or hold?

Chevron investors have remained resilient, as observed in its relatively outperformance over the past two months. The narrowing of the CVX valuation divergence with XOM indicates that CVX is not being valued expensively, which is confirmed by the ‘C-‘ valuation grade.

A positive outcome from Chevron’s arbitration with Exxon would provide a catalyst for further valuation rerating as Chevron works to bolster its asset portfolio with potentially high-growth, low-cost assets.

Rating: Keep buying.

IMPORTANT NOTE: Investors are reminded to conduct due diligence and not to rely on the information provided as financial advice. Consider this article to complement your required research. Please always apply independent thinking. Note that the classification is not intended to specify a specific entry/exit time at the time of writing unless otherwise stated.

I want to hear from you

Do you have a constructive comment to improve our thesis? Spotted a critical gap in our view? Did you see something important that we didn’t do? agree or disagree? Comment below to help everyone in the community learn better!