josefkubes

Companies undergoing change through corporate restructuring and spin-offs often provide good opportunities to crystallize value. (I think 3M)New York Stock Exchange: mmm) saw a similar dynamic with the recent rally, giving some relief to investors three years later From pain. Greater clarity on settlement costs also helped provide some clarity around significant risk factors.

However, the benefits from these elements are now likely to be priced out, and what is left is a patchwork of distressed companies that together cannot lift the group’s revenues, and the potential for large cash outflows further impairs the company’s ability to invest in the next four or five years.

Spinoff and change structure

Startups can create opportunities to crystallize value as well as confuse investors. 3M’s spin-off of its healthcare division as Solventum changed the company’s structure and may have created some opportunities for value creation The shares demonstrated strong performance over the past two months after several difficult years. This was accompanied by greater clarity on the costs of litigation in the two major cases relating to PFAS PWS and Combat Arms.

The company still holds a 19.9% stake in Solventum, which will be monetized within five years after the spin-off, for a potential outflow of $2 billion at the current valuation. Management will adjust reported earnings by the change in the value of the Solventum share.

As of Q1 2024, the Healthcare division reported some organic growth in volume (1% y/y) but is the lowest margin division in the group (17.5% adjusted operating margin vs. 21.9% for the group), and is experiencing margin pressure (-40 basis points on an annual basis in the first quarter of 2024).

What will be left is a group with relatively streamlined consolidated operations comprising three core divisions rather than four, with the group recording a higher margin due to the changing mix.

A look at recent trends

Results have been poor for years and the stock has suffered as a result, reaching a depressed valuation at 8x earnings at the bottom. Recent trends have improved slightly, with 3M reporting some slight organic sales growth (1%) and double-digit EPS growth as of Q1 2024, supported by 400 basis points of operating margin expansion.

At group level, the company achieved organic growth of 2.4% if rationalization measures, such as the closure of small countries, portfolio optimization and disposable ventilator businesses, are excluded. I’m very cautious about adjusting organic sales growth for companies that are divesting things. There is generally a risk that struggling companies will emerge from declining/unprofitable divisions to show better trends or better profitability on an adjusted basis, while structural issues increasingly impact more divisions in a pattern of permanent gap between adjusted and consolidated organic metrics. results. 3M has been divesting businesses for a while, such as exiting less attractive geographies (such as Russia in 2022). Although it does not adjust revenue metrics for this line item, I think investors should be careful not to jump to bullish conclusions and look confidently at the underlying revenue trends excluding the impact of the divested sectors. 3M has been weeding out less attractive companies for a while.

It’s certainly useful to look at organic sales trends, including and excluding the impact of these behaviors. As shown in the figure below, the trend is improving slightly in both cases, with annual growth in 1Q24 (although relatively easier to compound in 1Q23). However, we are still talking about less than 1% growth.

Company Files, Author

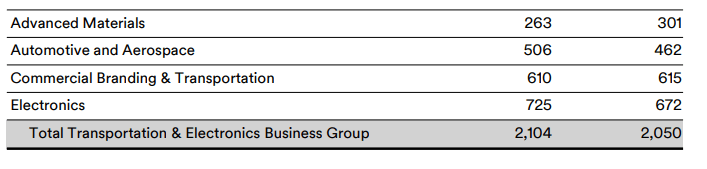

Revenue trends have improved in the areas of safety, industry and above all in transportation and electronics.

Company Files, Author

The Transportation & Electronics segment saw strong organic volume growth in Q1 2024 and is the highest margin segment in the group with an adjusted operating margin of approximately 24.3% compared to 21.9% group-wide. Automotive and aerospace, as well as electronics, were the main growth drivers for the division in the first quarter of 2024. Despite the strong start, it is expected to post low-single-digit adjusted organic sales growth during the full year.

Results for the first quarter of 2024

The Safety and Industrial Index is expected to be flat to the low single digits, while the Consumer Index is expected to contract in the low single digits. Overall, the company expects flat growth of +2% adjusted organic sales growth at the group level, showing that the company is still struggling to get close to GDP growth.

Lawsuits and cash flow pressures

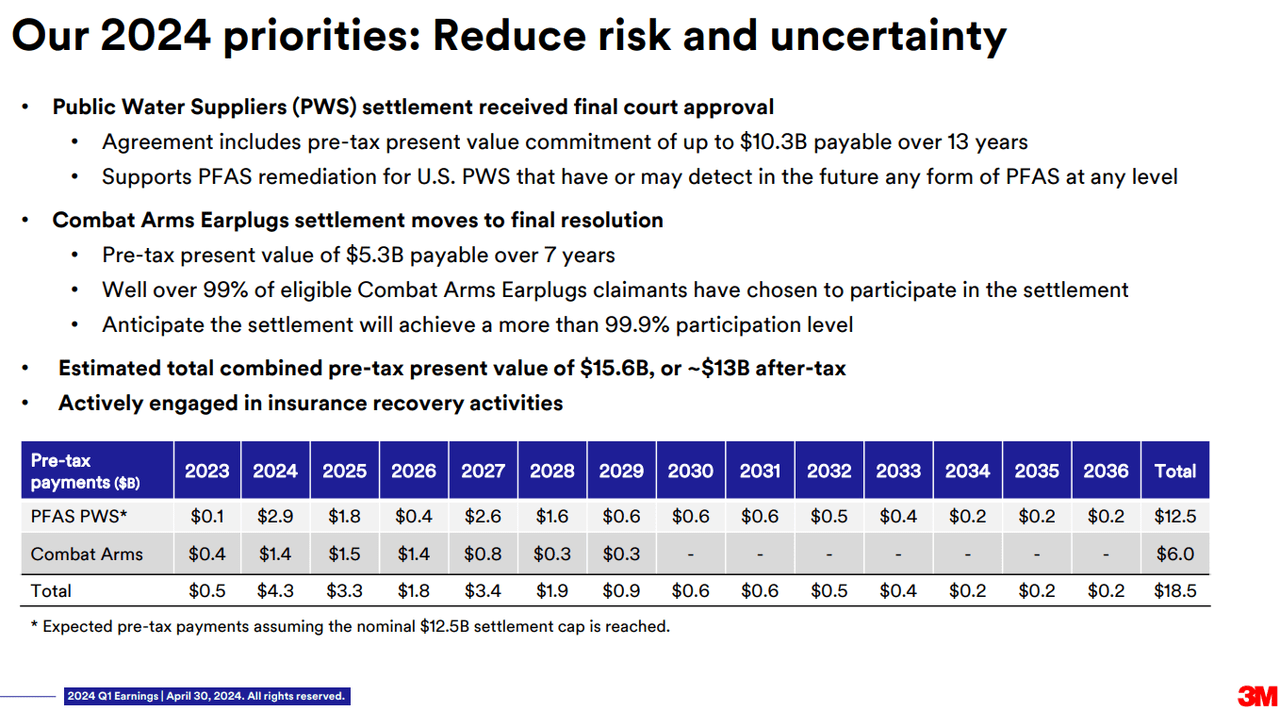

The big problem I see with 3M is the cash flow pressure from litigation payments. The total pre-tax cost of the Combat Arm Earplug settlement is estimated at $5.3 billion over 7 years, and more than 99% of eligible Combat Arm earplug claimants have elected to participate in the settlement.

The larger PFAS settlement is expected to cost PWS $10.3 billion before taxes over the next 13 years, which could increase to $12.5 billion based on additional PFAS contamination.

Results for the first quarter of 2024

The current status of the two issues suggests a total pre-tax cash flow drain of $15.6 billion in 13 years, with at least $1.8 billion annually (and a peak of $4.3 billion in 2024) for each year through 2028. Quantified by The court’s approval gave some investors more clarity and a chance to get involved in 3M’s potential value story. However, even assuming the matter is finally closed (3M will still be producing PFAS until the end of 2025), there is a structural cash burn issue that could severely limit the company’s ability to invest.

3M was generating an average of $4.9 billion in annual foreign cash flows in 2021-2023. Excluding an estimated $1.4 billion from Solventum (Q1 2024, $340 million per year), the current business could generate about $3.5 per year assuming no further deterioration. According to the expected repayment schedule shown in the table above, an average of $2.9 billion will be paid annually in the next four years. Further pressure could come from rising interest rate costs, as bond yields are rising, and the company faces about $6 billion in debt maturities through 2028 that need to be refinanced. Therefore, there is a significant risk that the company will generate minimal cash flow, if any, in this period.

It is also worth noting that with capital expenditures for 2021-2023, the company has faced declining revenues and flat overall revenues in the last six years. This may indicate that the company will need to invest more to achieve some growth (assuming there is growth for its products in its markets), but free cash flow trends indicate that there will not be a lot of investable cash flow available even with a full dividend cut (which has already been cut from $1.51 USD per quarter to USD 0.70). The fact that the company intends to continue paying a dividend equal to ~40% of adjusted free cash flow (which excludes litigation payments) may indicate a higher dividend than FCF generation, a choice I generally consider a red flag for almost any business (let alone one that doesn’t appears to have capital growth) which is a factor likely to contribute to further fundamental deterioration. Even assuming adjusted free cash flow of $4-4.5 billion, a ~40% dividend payout with $2.9 billion in annual litigation payments still suggests a higher dividend than free cash flow generation of $200-$500 million per year.

The valuation is not that attractive

Adjusted P/E ratios using the midpoint of the company’s EPS guidance ($7.05) still reflect a valuation at 14x EPS, which I don’t consider a bargain. At an 11% discount rate, this multiple still assumes perpetual growth prospects of 4%, and the company hasn’t come close to that level in the past five years. Furthermore, I think it’s important to acknowledge that the company is facing real cash flow pressure over the next five years, so adjusted EPS won’t translate into distributable cash flow anyway.

Conclusion

The Solventum spin-off and more clarity on litigation costs may have helped 3M stock in the short term, but structural challenges remain. The company is struggling to grow with revenue back six years ago and organic sales growing in the low single digits even with recent improvements. The company now faces further free cash flow pressure from litigation payments, and the valuation implies structural improvements that are not justified in my view. I believe the dividend remains at risk even after the recent cut, and if not, distributing more than FCF generation could further fundamentally deteriorate the business. I always look for good value among established companies, but I think this is a name to avoid in the current situation and at the current valuation.

I plan to continue following 3M and updating my thinking about it.