Kokosan

After our update on Diageo’Low beta and economic moat mean long uptrend“, Today we return to comment on Davide Campari-Milano NV (OTCPK:DVDCF). Since our last update (commentary on FY2023 results and installation of Courvoisier acquisition), Campari’s stock price fell approximately 4.67%. As a reminder, the company has undergone major changes with the appointment of a new CEO after 18 years of Bob Kunze-Konsiewicz assuming his position.

Marie Eve. Update laboratory classification

Meanwhile, the company released its first-quarter report, completed the acquisition of Courvoisier with convertible bonds converted into stock, and provided insight into the second half. Campari is a major global player for our new reader, with a product portfolio of over 50 premium and premium brands. Priority brands include Aperol, Campari, SKYY Vodka and Wild Turkey, which account for more than 50% of total sales. Campari focuses on organic and external growth through add-on acquisitions, having completed more than 26 acquisitions since 1995. More details They are in our Initiate coverage (June 2023).

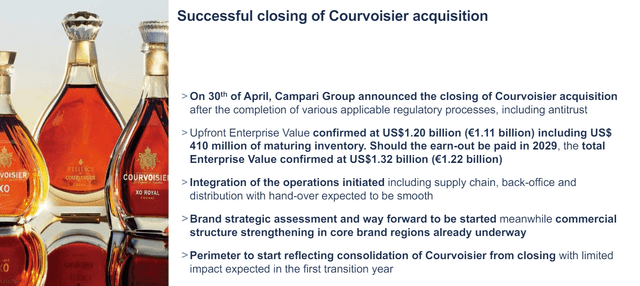

Acquisition of Courvoisier

Source: Campari first quarter results presentation

First quarter results

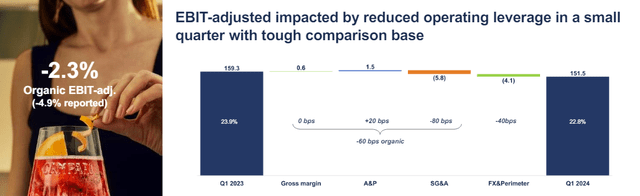

The company ended the first quarter, a traditionally low seasonal period, with net sales of €663.5 million. This is down 0.7% compared to the €668 million recorded in Q1 2023. However, looking at the details, Q1 2023 sales were up 19.6%, in one of the toughest competitions of the year. In addition, there were some temporary carryover effects of pre-purchasing before price increases and changes in China’s price market adjustment. In addition, the company was negatively impacted by the weak US dollar, playing negative at -1.4% versus -1.2% expected. Even if Campari’s Q1 2024 results look a little weaker at the top line, the decline in underlying operating profit margin was limited to 60 basis points, compared to expectations of 80 basis points. Favorable A&P milestones supported this. The appetizers division signed a plus 20 basis point of EBIT accretion, and we should report the appropriate mix and ends of last year’s price movements. This partially offsets cost of goods sold inflation. In terms of numbers, Campari’s adjusted EBIT amounted to €151.5 million and declined by -2.3% organically by a margin of 22.8%. On a reported basis, the company’s EBIT decreased by -4.9%.

Campari Bridge EBIT

Why are we still neutral?

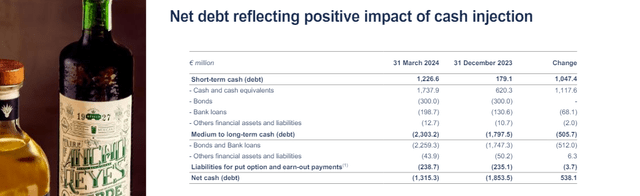

Starting with the positive news, we quote the CEO’s words: “Campari once again entered the year with momentum and a resilient performance in a down-season quarter. Going forward, our expectations remain unchanged.” In addition, following the acquisition of Courvoisier, Campari’s pro forma net debt to EBITDA was 3.5 times. Looking at the convertible notes and the company’s first-quarter results, that ratio is now 1.8 times.

Evolution of Campari’s net debt

On the downside, the current poor European weather conditions (there were +40% rainy days in April and May) may affect the development of second-quarter sales, although we still see strong demand for aperitifs. In the first quarter, Espolon (tequila), Aperol and Campari led the company’s organic sales growth.

Q1 sales from the Asia-Pacific region were very weak, recording a 20.2% decline year-on-year. This was due to high competition, particularly in Australia. The company’s competitors are still corporate, in Europe, and are very aggressive with pricing. We understand that Campari is adopting a wait-and-see strategy; However, the company may resist through promotional activity. In detail, the company sees some potential impacts from aggressive promotion in the gin category. In our estimates, we are now reducing our underlying operating profit margin slightly. In contrast, given Campari’s comprehensive product portfolio, we believe the company is not exposed to high competition in the United States. The company offers different price points and product categories. The company is also satisfied with the current inventory level in the region.

SKYY is seeing some softness in the product category; However, the CEO is confident that it will outperform the US market.

Looking at the recent acquisition, on the negative side, we confirmed an underlying operating profit impact of €10 million due to one-off costs. However, what we lack is investment vision. Here at the lab, according to NABCA, we are cautious about acquiring Courvoisier given that its Cognac sales have been underperforming the market. Our team has positive medium-term views on the long-term acquisition, but we believe the real market and cost benefits will contribute to the group’s margin in FY2025.

Campari forecast

Earnings and Valuation Changes

Combining our new financial estimate for Courvoisier and higher net sales in the first quarter (we previously estimated EUR 638 million), we have decided to reduce our fiscal 2024 sales from EUR 3.21 billion to EUR 3.15 billion. This is mainly due to the lower performance of the Asia-Pacific region and its impact on weather. In our estimates, we now expect a decline in currency exchange rates of 1.6%. This is in line with the current foreign exchange rate in EUR/USD terms. On margin, there is no change in D&A of €130 million; However, including one off-cost, we reached an underlying operating profit of $675 million. Considering convertible bonds, we reduced net interest rate payments to €76 million, reaching net income of €418 million from €428 million. For this reason, our EPS forecast is now €0.34. This also includes a larger number of shares.

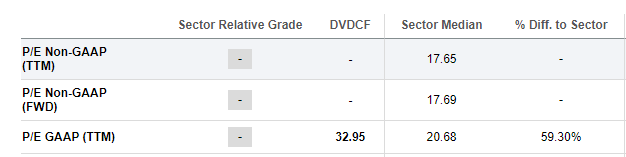

According to our 2024 estimates, Campari currently trades at 27.6x. Looking at Campari, the company’s valuation still looks complete. As a reminder, Campari has in the past traded at a roughly 50% premium valuation against the CPI. So, even applying a 30x P/E multiple, we arrive at a valuation of €10.2 per share. For this reason, given the current challenging trading environment, we maintain our Hold rating recommendation.

SA Campari Rating Data

Source: SA evaluation data

Risks

Our latest analysis has covered the downside risks well. In addition, we must mention that the company relies on competition in the beverage market. Consumer spending levels are also subject to weather conditions. Moreover, given its low debt-to-EBITDA ratio, Campari may once again be active in mergers and acquisitions. Therefore, there is some execution risk related to Courvoisier’s recent acquisition and potential value-destroying M&A for new brands.

Conclusion

There were no major surprises in the first quarter, but we lack visibility on Courvoisier stock and have to hope for a sunny summer. As mentioned earlier, the company is a show story with a positive catalyst in H2. However, the company’s valuation is expensive, and given some of the challenges ahead on a twelve-month basis, we affirm our Neutral rating status.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.