Lilia Litvin/iStock via Getty Images

R (New York Stock Exchange: R) Retails furniture under the RH Galleries and RH brands. In addition, the company operates showrooms under the Waterworks name. The company has international operations, operating in the United States, the Middle East, Australia, the United Kingdom and others Parts of Europe, among other places. RH focuses on the luxury segment of the furnishings industry, selling high-priced items.

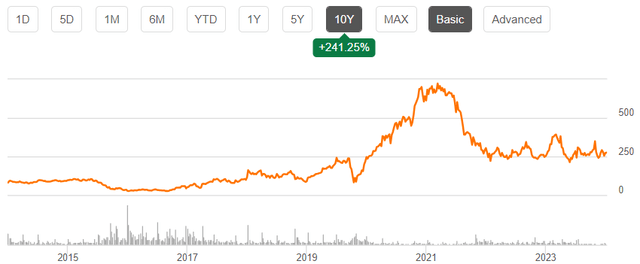

The stock has delivered a good return in the past decade, doubling at a CAGR of 13.1% fueled by aggressive share buybacks that significantly reduced outstanding shares. However, the stock’s recent returns have been negative, as Covid-boosted financials turned into earnings under pressure from a tougher economic climate.

Ten year stock chart (Searching for Alpha)

Financial profile: long-term growth, short-term stress

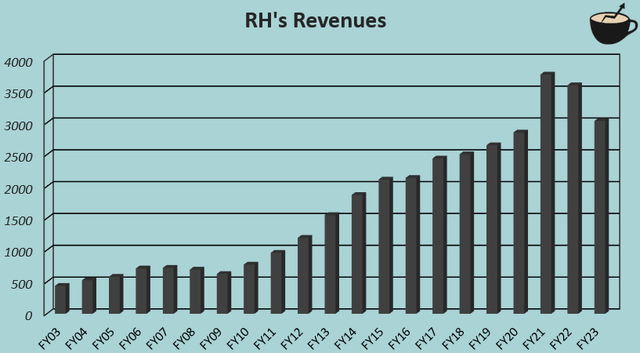

Over the long term, RH has achieved impressive growth. Company revenues It multiplied at a CAGR of 10.1% from FY03 to FY2023, with mostly organic growth.

Author’s calculation using TIKR data

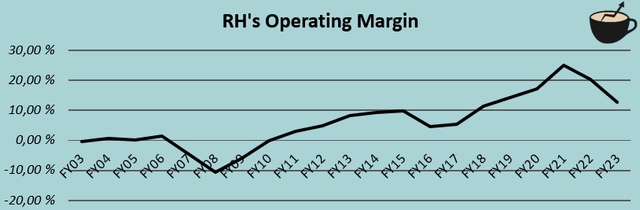

Along with the expansion of RH’s operations, the company saw significant margin expansion, driven by significant gross margin growth and some operating leverage. The company’s operating margin is currently below the level of previous years, but remains at a healthy number of 12.7% in fiscal 2023.

Author’s calculation using TIKR data

As can be seen in revenue and operating margin in the past two years, RH has seen a significant amount of financial turmoil after a mostly stable earnings history. The Covid-first pandemic quickly boosted RH’s sales, boosting revenue growth to 32.0% in fiscal 2021 as the housing market was buoyant and customers spent more time indoors. Due to higher sales, significant operating leverage also boosted operating margin from 14.4% in FY19 before the pandemic to 24.9% in FY2021.

Since then, the increase has eased, and revenues in FY2023 are 19.4% lower than revenues in FY2021. Revenues have now grown at a CAGR of just 3.4% from FY19 despite the higher inflation rate in this period, which is lower of RH’s long-term growth rate, making current revenues weak as the real estate market slows. Slowing sales pressured operating margin to the current FY2023 figure of just 12.7%, even lower than the margins achieved before the pandemic.

When and how will profits rebound?

An eventual recovery in RH sales seems inevitable. The weak fiscal year 2023 is clearly related to the incredibly sluggish housing market, as noted in our Q4 shareholder letter. The company already expects gradual improvements throughout fiscal year 2024 as the housing market recovers and interest rates decline – with the real estate market strongly linked to interest rates, the Fed’s decisions have a clear impact on the timing of the recovery in the US furniture industry. . In Europe, 12-month Euribor interest rates remain very close to the peak at the moment, but interest rates are expected to fall in the back half of 2024.

RH’s financial projections for 8% to 10% growth in FY2024 appear to anticipate a significant rebound in the coming quarters as Q1 sales are still geared slightly downward – I think there is a high chance the financial projections will not be met, and investors should not expect such This recovery is timely. Competitors’ revenues are expected to remain weak, with revenue growth expected at 1.1% for Wayfair (W), 5.4% for aggressively expanding Arhaus (ARHS), and negative -9.2% for Haverty Furniture (HVT).

The size of the financial recovery also remains a matter of debate. Investors should not only think back to the profits made during the increased demand due to the Covid pandemic, but in my opinion they should extrapolate to pre-pandemic trends. RH has continued to invest in growth over recent years with a record $269.4 million in capital expenditures in FY2023, and operations have grown nicely since FY19 despite very similar revenues – at a revenue CAGR of 7.2% year over year Fiscal 2014 to Fiscal 2019 revenues would have ended at $3,496 million in fiscal 2023 instead of the $3,029 million achieved, which represents a better estimate of current sustainable sales under normal circumstances.

Margins should also see a significant increase from the operating margin achieved in FY 2023. FY 2019 operating margin of 14.4% appears to be lower than what should currently be expected given RH’s historically large operating leverage, but much higher margins should not be expected in my opinion.

First quarter results coming

Although a specific Q1/FY2024 results date has not been announced at the time of writing, RH is expected to report earnings soon. Analysts expect revenue of $725.2 million and common stock earnings of -$0.10 in the typically seasonally low sales quarter. The estimates represent a year-over-year revenue decline of -1.9% and a significant EPS decline of -$2.31, and follow the Q1 guidance provided by RH for a low-single-digit revenue decline and an adjusted operating margin between 6% and 7%. This quarter follows a -4.4% decline in Q4/FY2023 revenue.

Peak profits are priced in

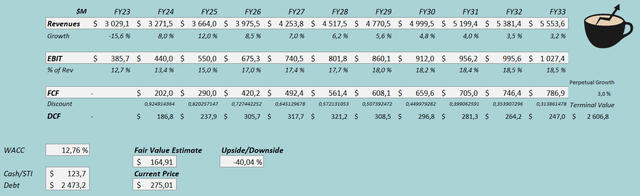

You have created a discounted cash flow model (Discounted Cash Flow Model) to estimate the fair value of the stock. In the model, I estimate RH revenues to grow 8% in FY 2024, followed by an improving housing market leading to 12% growth in FY 2025. After that, I estimate a gradual slowdown in growth in steps toward permanent 3% growth. , which represents a compound annual growth rate of 6.2% from fiscal year 2023 to fiscal year 2033.

For EBIT margin, I estimate incremental improvements from 12.7% in FY2023 to 17.0% in FY2026, raised further thereafter to a final level of 18.5% through operating leverage and slight expansion in gross margin. The company’s capital expenditures and increased working capital are reducing cash flow, making the conversion rate very modest, but I estimate there will be a gradual improvement as growth slows.

With the estimates mentioned, the DCF model estimates the fair value of RH at $164.91, about 40% below the share price at the time of writing – although the share price is down significantly from its 2021 highs, The stock still appears to be pricing earnings expectations too high. . A more aggressive growth trajectory could make the stock worth the current price, but with a five-year RH return on capital of 14.0%, more aggressive growth would require more intensive investments than I currently expect as well.

Discounted cash flow model (author’s account)

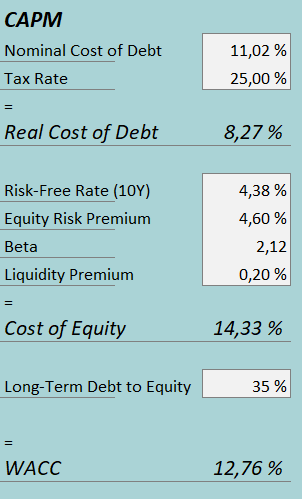

A weighted average cost of capital of 12.76% was used in the DCF model. The weighted average cost of capital (WACC) used is derived from the capital asset pricing model:

CAPM (author’s account)

In the fourth quarter, RH had $68.1 million in interest expense. With the company’s current amount of interest-bearing debt, RH’s annual interest rate is 11.02%. The interest rate appears to be very high and reflects RH’s high debt and volatile operating profits. Despite the turbulent earnings, RH benefits from a significant amount of debt, and I estimate its long-term debt-to-equity ratio to be 40%.

For the risk-free rate on the cost side of stocks, I use the ten-year US bond yield of 4.38%. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the US, updated on 5y January. Seeking Alpha estimates RH’s beta at 2.12. Finally, I add a small liquidity premium of 0.2%, creating a cost of equity of 14.33% and an average cost of capital of 12.76%.

He stays away

RH’s earnings have fallen from pandemic highs to currently low earnings due to a sluggish housing market. The company expects a gradual recovery in demand during fiscal 2024, but I think caution on the timing of the recovery is necessary as competitors are estimated to be very weak in 2024. The current stock price seems to be anticipating a strong recovery in earnings to pandemic highs, which I don’t see The possibility of this happening in the medium term. While RH should be able to continue the growth story over the long term and restore earnings to a better, more natural level, the current valuation appears to be pricing in too much. As such, I have a Sell rating at present.