G studios

Written by Nick Ackerman, and co-produced by Stanford Chemist.

Is your multi-asset closed-end fund under attack from a group of “activist hedge funds”? Thornburgh Income Building Opportunities Fund (Nasdaq:TBLD) is another option on the market In this space it is also worth taking a look.

TBLD is trading at an attractive discount to its net asset value, making it a potential opportunity today. The fund invests in a broad portfolio that includes equities and fixed income, and includes flexibility for derivatives.

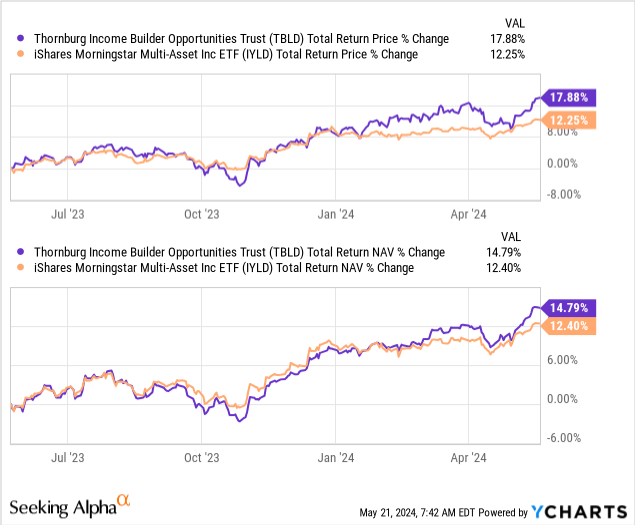

It’s been a little over a year since we last took a look at TBLD. Thanks to strong overall performance in equities and broader fixed income, this fund has performed fairly well. The discount ratio has narrowed slightly over this time, but has managed to outperform the iShares Morningstar Multi-Asset Income ETF (IYLD). IYLD is a 60/40 split between Fixed income and equity.

YCharts

TBLD Basics

- One-year Z-score: 0.75.

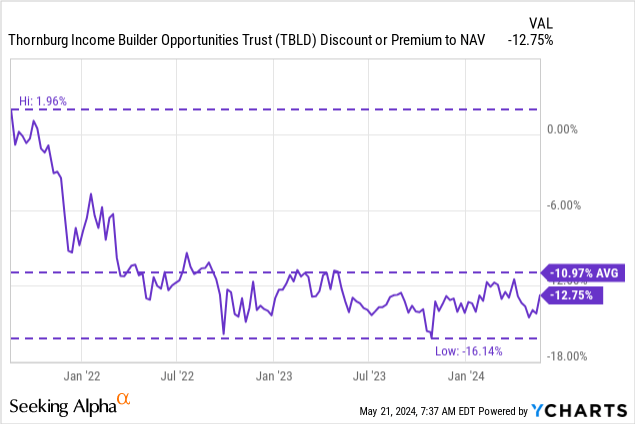

- Discount: 12.75%.

- Distribution yield: 7.71%.

- Expense ratio: 1.62%.

- Leverage: Not available.

- Assets under management: $574 million.

- Structure: Duration (expected liquidation date August 2, 2033).

TBLD’s investment objective is “to provide current income and additional total return.” To achieve this, the Fund will invest “in a broad range of income-producing securities to include both stocks and debt securities of companies located in the United States and around the world. The Fund additionally expects to use an options strategy to generate current income from option premiums and improve risk-adjusted returns.”

This leaves the fund completely flexible to invest in anything income related. 80% of the fund will be invested in income-generating securities “directly or indirectly.” It is not limited to a certain market cap of investment in a company, but is strongly skewed towards large capitalization. At this time, they make up 90.5% of the portfolio.

They still do not currently use any leverage through borrowing, but as mentioned earlier, they leave the option of availing themselves of some form of loans in the future. The fund will also write options “about 10% to 40%” to replace the portfolio. When we last looked at the fund, it was trading at 8.9%, and today it is listed at 7%. So, this is not a strategy that they seem to be using heavily. To be fair, in a bull market that still seems to have upward momentum behind it, this is a good thing.

Structured exposure to multi-asset closed-end fund

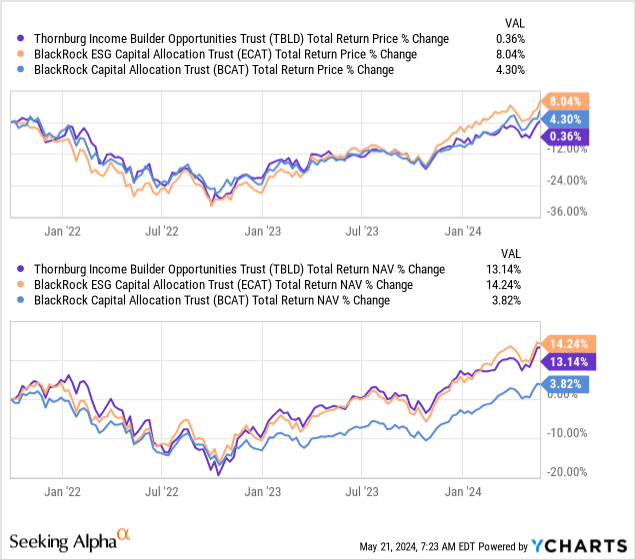

When looking at BlackRock funds, both BlackRock ESG Capital Allocation Term Trust (ECAT) and BlackRock Capital Allocation Term Trust (BCAT) are also two funds that have similar flexibility in their investment strategies. TBLD was launched just before ECAT, with TBLD coming to market on 27 July 2021, and ECAT trading commencing on 27 September. Since then, TBLD and ECAT have provided incredibly similar overall NAV return performance results and have shown a high correlation. The BCAT was lagging behind in this period, for what it’s worth, but I’ve included it for more context.

YCharts

However, with ECAT under significant pressure from Saba Capital Management, an investor may look elsewhere to put his capital to work. That’s why I believe TBLD offers this alternative option for investors who may want to remain in a multi-asset space in a closed-end fund structure.

If Saba beats BlackRock and takes over ECAT, there’s a good chance the future will be very different for ECAT. They have already put enough pressure on BlackRock to increase the fund’s distribution to a 20% managed policy. So, changes really only happen with pressure.

What makes TBLD a fairly solid option today is that the fund continues to trade at a significant, attractive discount on an absolute and relative basis.

YCharts

I think the main caveat or “danger” with this is that with such a large opponent, it could become a future target of an activist group. At the moment, the most active company, Saba, appears to be busy with an all-out campaign against BlackRock.

TBLD Distribution delivers

TBLD currently pays a monthly distribution of $0.1042, which it has done since the fund’s launch. That works out to 7.71% based on today’s stock price. This may not be as flashy as the new 20%+ rates that ECAT and BCAT are now paying, but with an NAV rate of 6.72%, it looks more sustainable in the long term.

In fact, it wouldn’t be too surprising if they raised their yields from this level at some point. They may be hoping to get their net assets back above the initial launch price of $20. The fund was launched in 2021, as mentioned earlier, so seeing NAV decline almost immediately as we head into the bear market in 2022 is not a huge negative for me. It was a bad time for most investments, and this fund happened to be launched at an unfortunate time.

The fund will need capital gains to support the distribution. This is not unusual for a CEF fund, especially one that has about 60% of its portfolio in stocks.

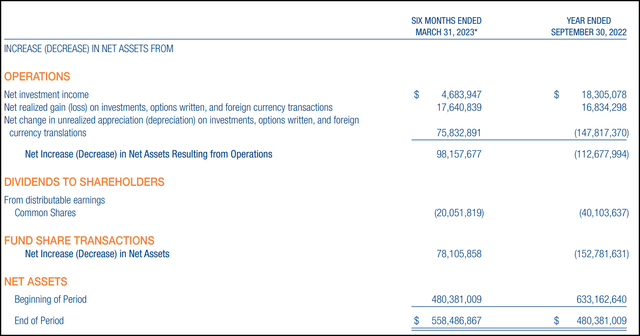

TBLD Semi-Annual Report (Thornberg)

This is one area where writing options can help as well, as they have contributed to some capital gains as of the last semi-annual report. With the receipt of National Insurance and options premium, the distribution coverage was approximately 43.5%. The remaining deficit will have to be “covered” by an appreciation in the value of the underlying portfolio.

TBLD Realized/Unrealized Gains/Losses (Thornberg)

For tax purposes, the Fund’s distribution is primarily described as ordinary income.

Tax Classification of Distribution TBLD (Thornberg)

Approximately 41% of 2023 ordinary income was considered qualifying dividends. This is more tax-friendly, but this fund seems like a good candidate for a tax-sheltered account rather than a taxable account based on the data we’ve seen so far. It is important to remember that these rankings change every year.

TBLD Wallet

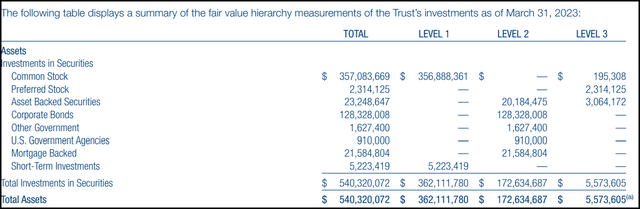

The Fund invests primarily in liquid securities, or those with a Tier 1 securities rating. The fixed income wrapper is primarily Tier II securities, which is normal because bonds are not traded on an exchange at quoted prices. After that, the fund has a small portion of Tier 3 securities, which is not very material at this point.

TBLD Security Level Breakdown (Thornberg)

I mention this because ECAT and BCAT, along with TBLD, allow investments without restrictions or restrictions in private investments. As of recent annual reports, BCAT was the highest for Tier 3 securities at 12.4%, with ECAT at approximately 4.4%. If one looks at TBLD as a potential alternative to ECAT or BCAT, if these funds change hands in the future, it appears they will get less in terms of private corporate exposure.

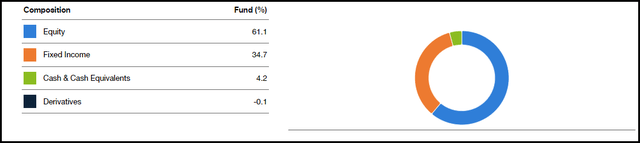

Looking at TBLD more broadly, the fund prefers equity investments over fixed income. Over a year ago, when we took a look at this fund, it had a similar weighting, so we haven’t seen much change on that front. This isn’t too surprising given that the fund’s turnover was 16.19% in its last semi-annual report. This has not been calculated on an annual basis but is still lower than the turnover of over 58% reported in the previous financial year.

TBLD Asset Allocation (Thornberg)

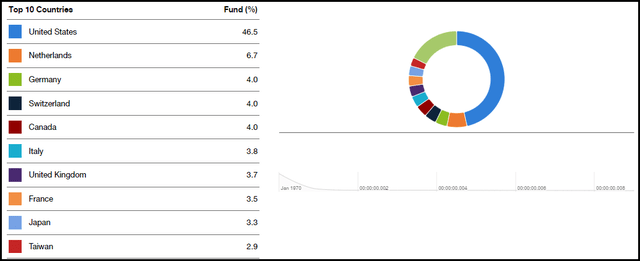

Regarding the geographic segmentation of the portfolio, we also see a similar weighting to our previous update. The United States remains the fund’s largest weighting, previously at 46.3%, and the allocation is almost identical now as then. However, taken together, international exposure still constitutes a significant weighting in the fund.

Geographical assignment TBLD (Thornberg)

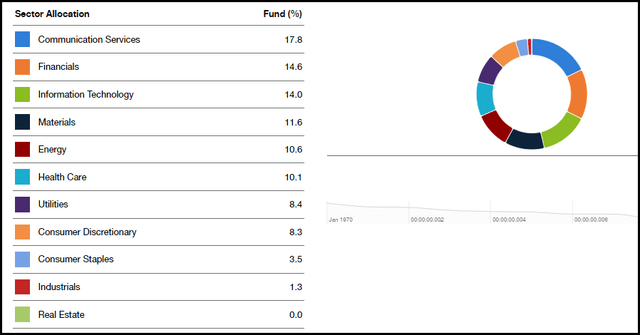

Taking a look at the fund’s sector allocation, we see little change here. The fund previously preferred the financial sector, with 22.5% allocated to the fund. This has since been replaced by telecommunications services, which now represents the largest sector weighting the size of the fund. Previously, telecommunications services represented 9.8% of the fund’s invested capital.

TBLD sector allocation (Thornberg)

The fund’s exposure away from generally high-tech funds that compete directly with the broader market as measured by the S&P 500, I think is one of the positives about the fund. It can be a complement to a person’s portfolio if they are strongly leaning towards technology and want to see more diversification.

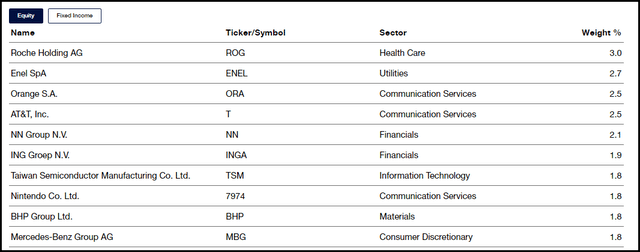

Seeing this shift in the sector to the upside, it was the result of the emergence of Orange SA (ORAN), and AT&T Inc. (T), and Nintendo Co., Ltd. (OTCPK:NTDOY) is now in the top ten. It is worth noting that ORAN and NTDOY are examples of the company’s international reach with ORAN, a French company and NTDOY based out of Japan.

TBLD Top Stock Holdings (Thornberg)

Interestingly, Meta Platforms, Inc. (META), a giant company also listed in the telecom services sector, was in the top 10 but is no longer listed. However, META remains in position, but the weighting has decreased to around 1.25%.

Overall, it’s quite clear to see that TBLD offers a lot of diversification and exposure to various companies up and down the capital spectrum, as well as domestic and international exposure. This can make it a type of umbrella fund, where an investor can own just that fund, if they so choose, and still be appropriately diversified.

Conclusion

TBLD is a multi-asset closed-end fund that has great flexibility about when, where and how to invest. This provides great diversification, and pays a decent distribution rate for income-oriented investors. Given the attractive discount on an absolute and relative basis, the fund appears to present an attractive opportunity to consider. Investors in ECAT could consider TBLD as a potential alternative as well, should ECAT change radically in the future.