adventtr/iStock via Getty Images

Clover Health Investments Company (NASDAQ:CLOV) recently announced that it will make its technology platform available to all Medicare Advantage payers and providers. This endeavor will effectively change the company’s business model from just… Traditional Medicare Advantage plan provider of a hybrid SaaS model and shared savings model, with full-individual options. In doing so, Clover Health is finally embracing the AI aspect of its business model that could help boost its valuation thanks to the potential of this endeavor to capitalize on the growth of its peers. In light of this, as well as the company’s improving profitability prospects, I rate Clover Health a Buy with a price target of $2.45, which would imply an upside of 120% from current levels.

Business overview

Clover Health is a Medicare Advantage plan provider that combines technology, data analytics, and preventive care to reduce and increase costs Quality of health and life of Medicare beneficiaries. The company’s technology platform, Clover Assistant, uses artificial intelligence and machine learning to deliver data and insights to clinicians that help with early diagnosis and management of chronic diseases.

While Clover Health is still not profitable, the company has made great strides in this regard as it reported impressive results for the first quarter of 2024. The company’s insurance revenue rose 8% year over year to $341.7 million and its medical cost ratio (MCR) improved ) during the same period from 86.6% to 77.9%. As a result, the company recorded positive first-quarter adjusted EBITDA of $7 million and its net loss significantly improved year over year from $72.6 million to $19.1 million. For the full year, Clover Health is guiding for insurance revenue between $1.3 billion to $1.35 billion, an MCR ratio between 79% to 81%, and positive adjusted EBITDA between $10 million and $30 million.

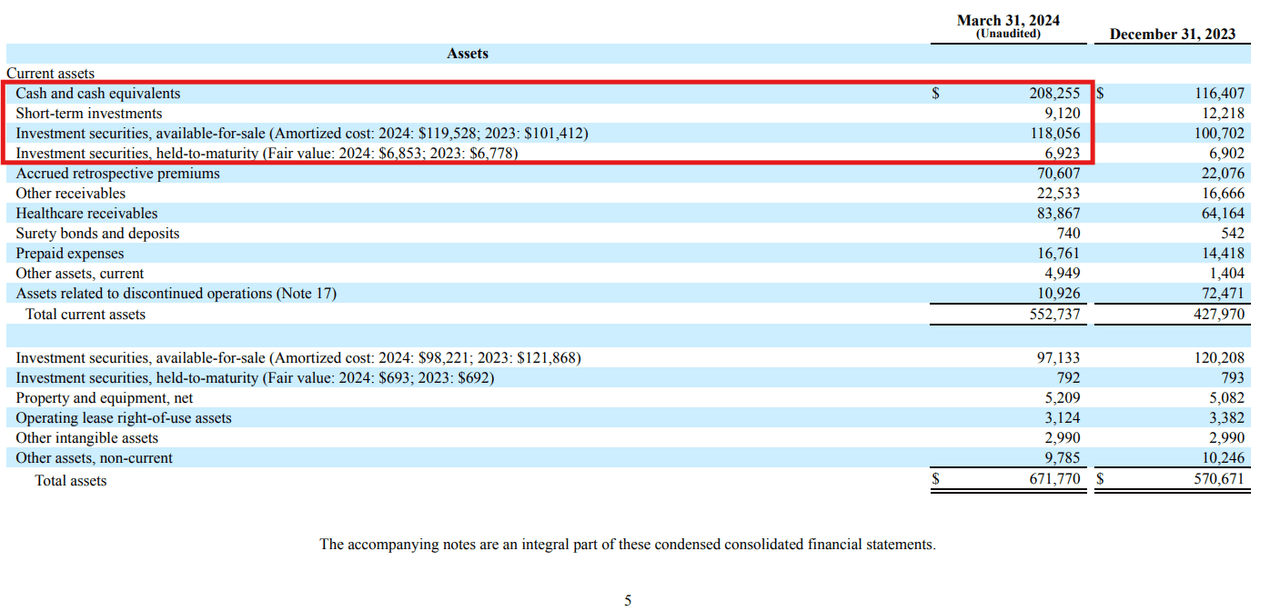

Clover Health also has a strong balance sheet containing cash, cash equivalents and short-term investments, as well as available-for-sale and held-to-maturity investments of $342.4 million, along with approximately $98 million of long-term available-for-sale and held-to-maturity investment securities Its history. Maturity, zero debt. This strong liquidity position has allowed the company to announce a $20 million stock buyback program over the next two years.

10-Q filing

Taking advantage of artificial intelligence

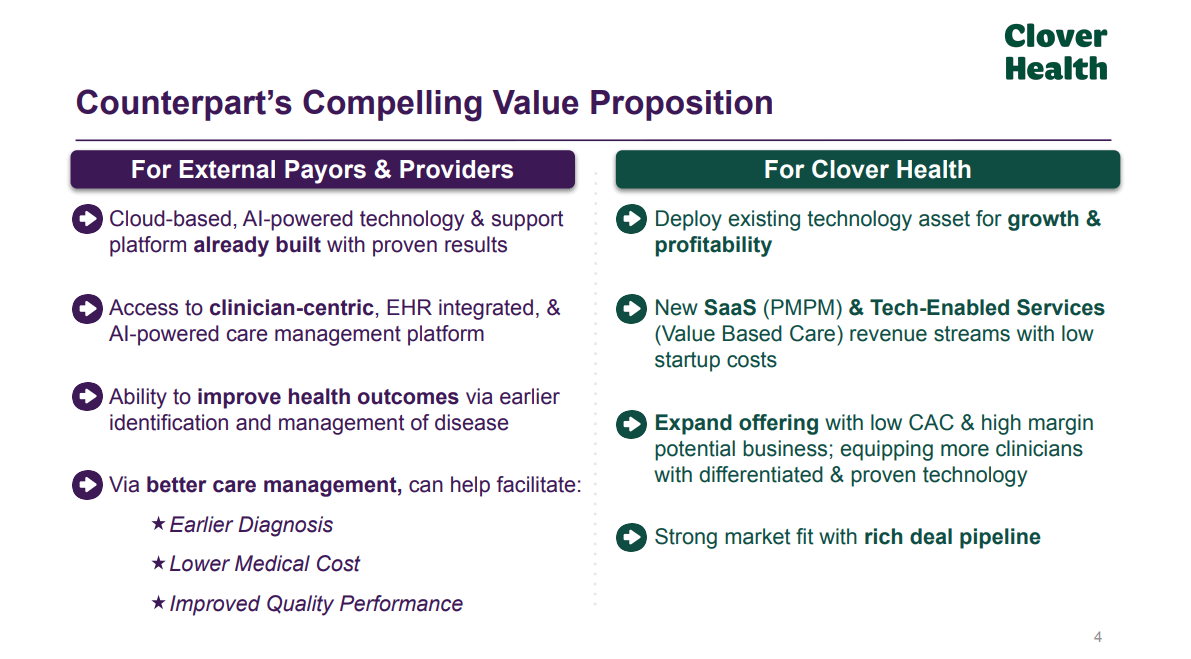

While the core of Clover Health’s value proposition is its technology platform, Clover Assistant, the company never marketed itself as an AI company during a time when the term “AI” became a buzzword for many companies. That’s why I find the company’s decision to make its AI-powered technology platform available to all Medicare Advantage payers and providers under the Counterpart Assistant brand promising for its long-term prospects.

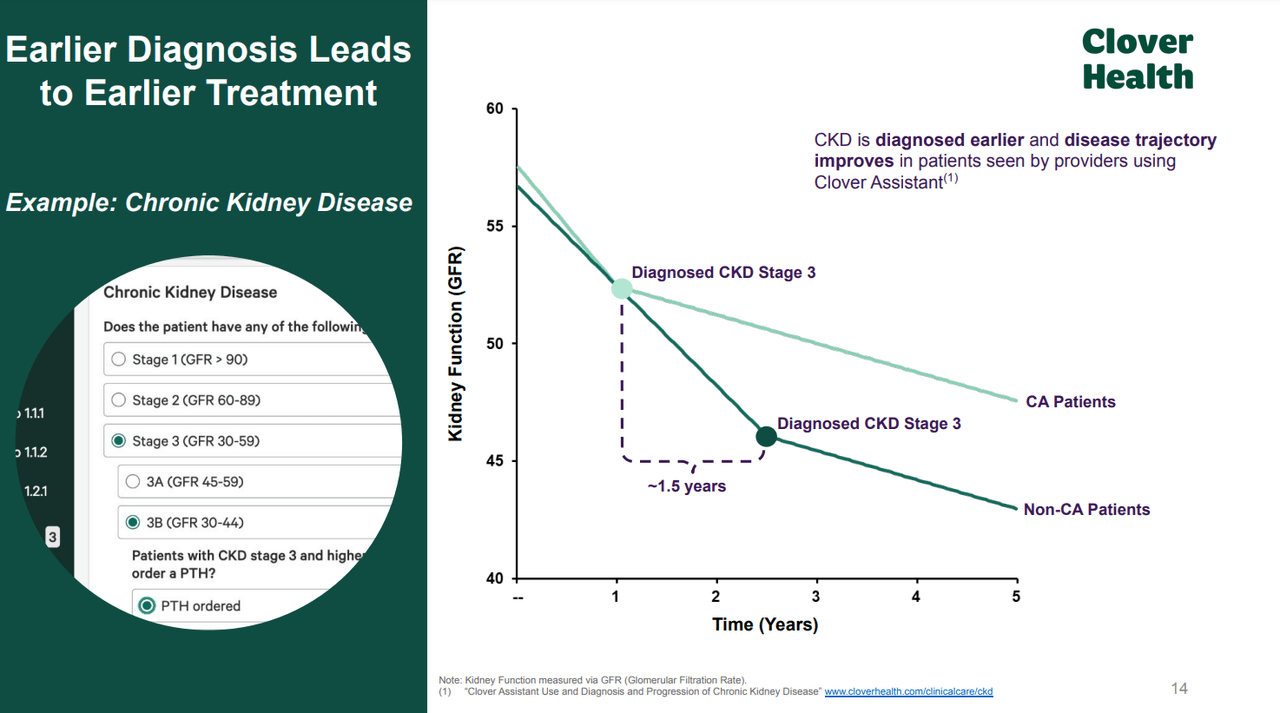

In my opinion, Counterpart Assistant could be highly desirable by Medicare Advantage payers and providers with its ability to diagnose chronic diseases, specifically chronic kidney disease (CDK) and diabetes. According to Clover Health’s most recent investor presentation, Clover Assistant patients with stage 3 chronic kidney disease were diagnosed 1.5 years earlier than non-Clover Assistant patients.

May investor presentation

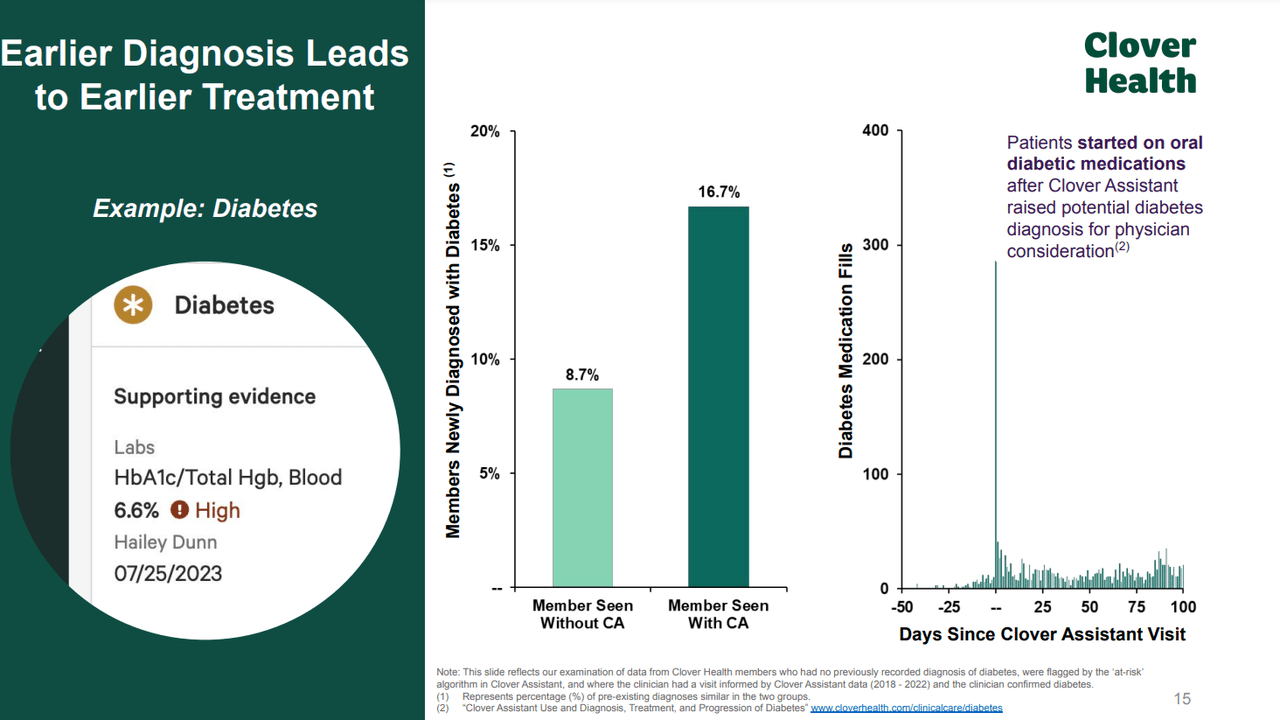

Meanwhile, 16.7% of patients treated with Clover Assistant were diagnosed with diabetes compared to 8.7% in patients treated without Clover Assistant, resulting in earlier treatment.

May investor presentation

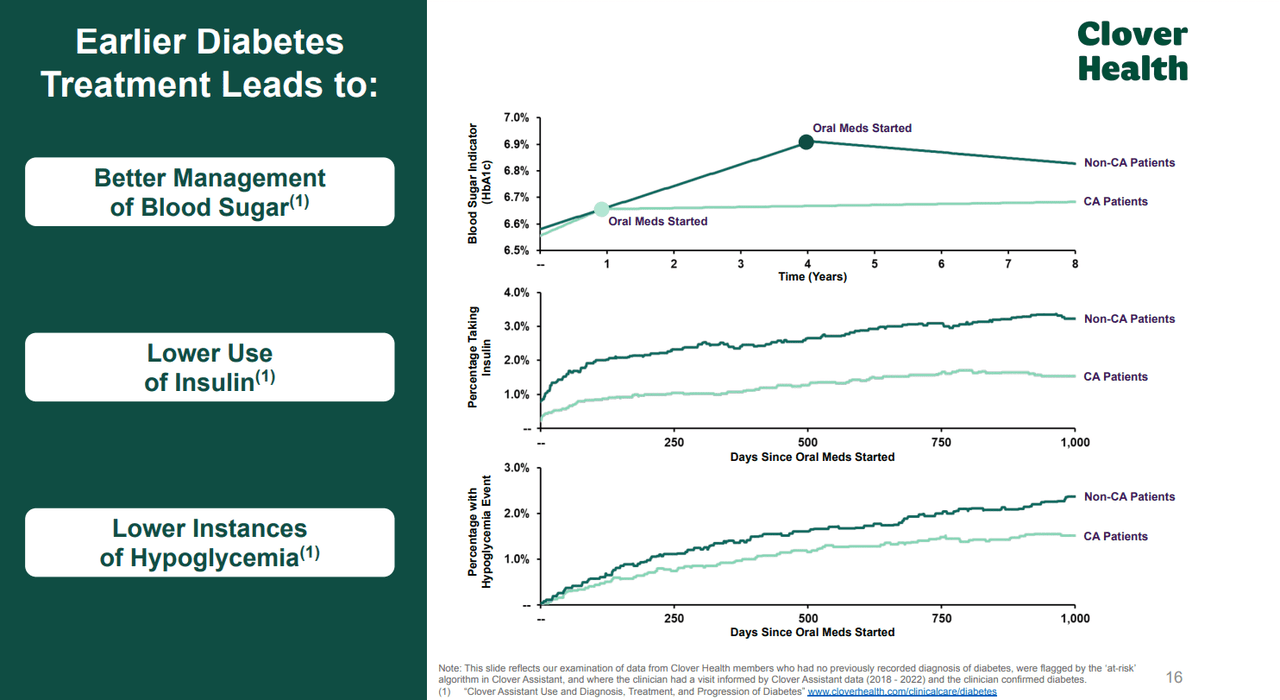

Results from early treatment of diabetes have shown better blood sugar management, decreased insulin use, and decreased incidences of hypoglycemia.

May investor presentation

Counterpart Assistant’s ability to diagnose chronic diseases early is a major selling point in my opinion. This is mainly due to lower treatment costs associated with early intervention, which may lead to less expensive treatments, less invasive surgeries, and shorter hospital stays compared to diseases diagnosed at a later stage.

At the same time, early treatment can prevent complications, leading insurance providers to avoid covering the costs associated with treating these complications, which can be significant in some cases. Early diagnosis can also allow for preventive measures and lifestyle changes that can keep patients healthier, which often translates into fewer claims for insurance providers in the long run.

With that in mind, I think Clover Health may announce a deal with a major Medicare Advantage provider like UnitedHealth (UNH), Humana (HUM), or Cigna (CI) soon, since it shared in a recent presentation that it has “ Rich Deal Pipeline.”

2024 Leerink Partners Healthcare Crossroads Conference

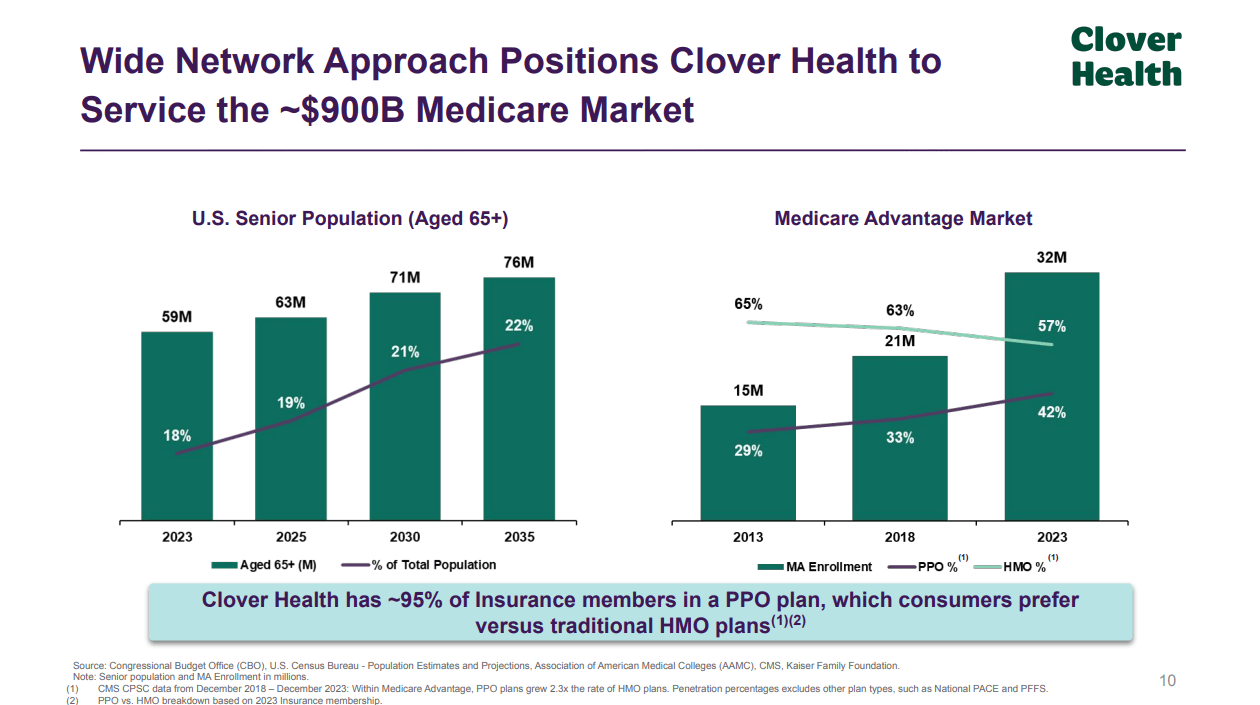

If this is indeed the case, Clover Health will benefit from the growing $900 billion medical care market due to the current aging population, with 76 million Americans expected to be over 65 years of age in 2035, representing 22% of the total population .

May investor presentation

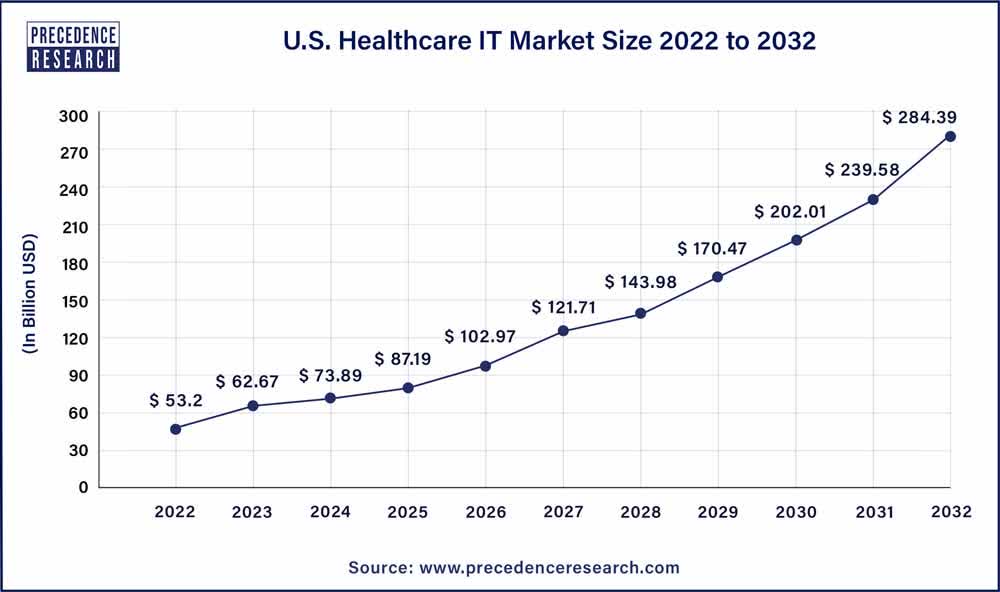

Even if that’s not the case, Clover Health’s endeavor will allow it to capitalize on growing technology spending in the healthcare sector. According to Precedence Research, the US healthcare IT market was valued at $53.2 billion in 2022 and is expected to reach $284.4 billion by 2032, at a compound annual growth rate of 18.3%. Therefore, I believe Clover Health’s growth prospects are strong for the foreseeable future.

primacy research

Benefits of the new business model

Aside from the growth opportunity this endeavor provides, this new business model will help Clover Health’s profitability thanks to the higher margins expected for this new business. Clover Health said the new offering will use a hybrid SaaS and shared savings revenue model, with options for full participation.

In the per capita system model, Clover Health is paid a fixed amount for each patient the Counterpart Assistant visits providing financial certainty. Meanwhile, the shared savings model gives Clover Health a percentage of any savings Counterpart Assistant users make through the platform when their total costs of care (TCOC) are below the agreed-upon TCOC benchmark. As for the SaaS revenue model, Clover Health will receive periodic recurring fees for access to Counterpart Assistant.

Through a combination of these revenue models, Clover Health will benefit from long-term growth in the Medicare Advantage segment while maintaining higher margins than other insurers. The reason for this is that insurers’ medical loss ratio is capped at 80% under the Affordable Care Act, which requires insurers to spend at least 80% of their premium revenue on medical care and quality improvement activities. If the insurance company spends less than 80% on medical care, the difference must be returned to policyholders.

evaluation

Given Clover Health’s expected growth prospects from its decision to begin selling its technology platform to other Medicare Advantage payers and providers as well as the benefits of its new business model, I believe the stock is undervalued at its current valuation. At its current stock price of $1.11, Clover Health is worth just $208.7 million. This means that its shares are trading at a forward sales/value multiple of 0.16.

|

Market value |

$551,045,584 |

|

Liquidity |

$342,354,000 |

|

religion |

$0 |

|

Eve |

$208,691,584 |

|

Revenue guidance (midpoint) |

$1,325,000,000 |

|

EV/Sales |

0.16 |

Meanwhile, other Medicare Advantage plan providers like UnitedHealth, Humana, Elevance (ELV), Centene (CNC), Cigna, and Alignment Healthcare (ALHC) are trading at the following EV/sales multiples.

|

a company |

EV/Sales |

|

United nations |

1.29 |

|

Hmm |

0.45 |

|

ELV |

0.85 |

|

CNC |

0.26 |

|

CI |

0.52 |

|

ALHC |

0.58 |

|

middle |

0.66 |

One reason for Clover’s lower Health multiple compared to its peers may be its much lower size. As it stands, the company reported 79,527 insurance members in Q1 2024, a number that pales in comparison to its aforementioned peers, as the following table shows.

|

a company |

Members |

market share |

|

United nations |

9,439,000 |

28.6% |

|

Hmm |

5,974,000 |

18.1% |

|

ELV |

1,988,000 |

6.0% |

|

CNC |

1,123,000 |

3.4% |

|

CI |

587000 |

1.8% |

|

ALHC |

144000 |

0.4% |

*Data was collected from a report by healthcare analytics company The Chartis Group.

However, Clover Health now has the ability to benefit from the growth of its peers due to its technology platform being available to all Medicare Advantage plan providers. That’s why I expect the company’s valuation to rise in line with, or even exceed, its peers if Counterpart Assistant is adopted by several major Medicare Advantage plan providers.

As such, applying a 0.66 EV/sales multiple to Clover Health, which is the average multiple for Medicare Advantage plan providers, would imply an enterprise value of about $872.3 million. When adding the company’s net cash position of $342.4 million, this would result in an equity value of $1.2 billion, resulting in a price target of $2.45 per share, which represents an upside of 120% from current levels.

|

he won |

$1,325,000,000 |

|

Eve |

$208,691,584 |

|

EV/Sales |

0.16 |

|

The goal is multiple |

0.66 |

|

Implicit EV |

$872,291,667 |

|

Net cash |

$342,354,000 |

|

Share value |

$1,214,645,667 |

|

OS |

496,437,463 |

|

Price target |

$2.45 |

|

Share the price |

$1.11 |

|

Upside down |

120% |

I used Clover Health’s EV/Sales ratio to arrive at the target price, since the company has not yet posted its full year of EBITDA profitability, and the expected full-year EBITDA is not representative of its future cost structure, in My opinion.

Risks

Although I’m bullish on Clover Health, there are risks to my thesis worth considering. The first risk is government regulations, as Medicare Advantage is subject to regulations that may affect reimbursement rates and program requirements, which could negatively impact the company’s growth prospects.

Another risk is a decline in the number of insurance members at Clover Health. The company reported 79,527 members in the first quarter of 2024, down from 81,205 in 2023 and 88,627 in 2022. Although increased net PMPM premiums offset the decline in membership, Clover Health should show a path to growing its member base Otherwise, its insurance revenues may be harmed. At risk of decline in the future.

|

a period |

Members |

Net Premium PMPM |

|

2022 |

88,627 |

$1,041 |

|

2023 |

81,205 |

$1,250 |

|

First quarter 2024 |

79,527 |

$1,437 |

* Data collected from earnings reports.

Conclusion

With the company now offering its AI-powered technology platform to the broader Medicare Advantage market, I am optimistic about Clover Health’s future prospects thanks to its ability to capitalize on industry growth and expected margin expansion resulting from its new business model. Counterpart Assistant has proven successful in diagnosing chronic diseases, specifically chronic kidney disease and diabetes, early, which I expect will be the main selling point of the offering for Medicare Advantage payers and providers thanks to the cost benefits of early diagnosis.

Meanwhile, the new offering will use a hybrid SaaS and shared savings revenue model, with options for full participation. This new model will add more financial certainty as well as boost the company’s margins, which will be crucial to its profitability prospects. Based on this, I rate Clover Health a Buy with a target price of $2.45, implying 120% from current levels.