Designer491

Every investment has potential risk and potential reward. We must ask ourselves whether the rewards on offer justify the risk. With the SPDR Bloomberg High Yield Bond ETF (NYSEARCA: JNK), the rewards on offer are clear – and they are higher The return and capital gains are modest. However, the yield premium does not appear to justify the additional risk of holding junk bonds, especially given the deteriorating macroeconomic picture.

Presented by JNK

JNK was launched in 2007 and has US$8.19 billion in assets under management. It is a passively managed fund that seeks to track the performance of the very liquid Bloomberg High Yield Index. According to the prospectus, the index “includes publicly issued U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bonds with maturity of at least one year, but not more than fifteen years, regardless of optionality.”

Additional rules apply in Selection process. Bonds must:

- You have $500 million or more of outstanding par value.

- Released within the past five years.

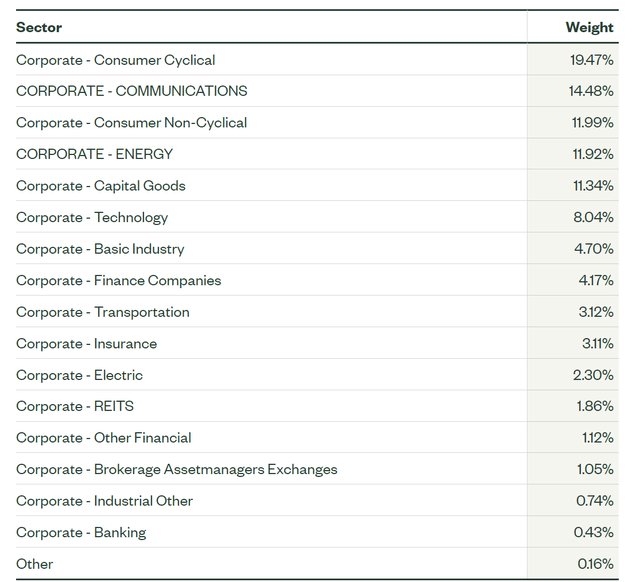

The fund holds approximately 1,192 bonds, with none currently weighted more than 0.5%. Furthermore, “exposure from each eligible source will be capped at 2% of the index.” This gives the portfolio good diversification, although sector exposure is highly concentrated.

Sector exposure (SSGA)

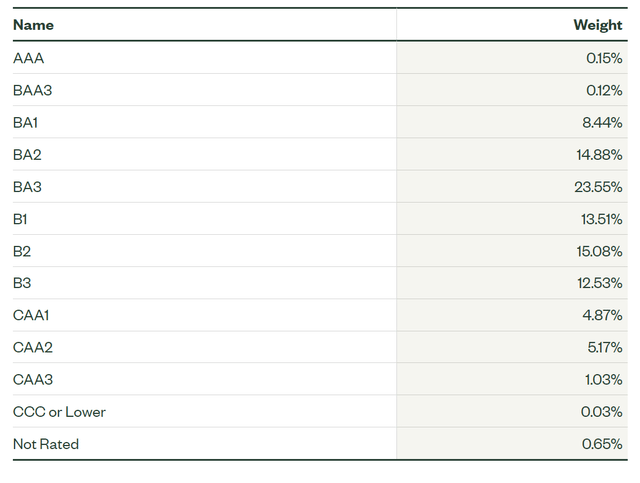

Below is a breakdown of the collectibles’ credit ratings.

Credit ratings (SSGA)

Over 99% of the holdings are rated below investment grade (BAA3) and are therefore “junk bonds”. Credit risk is therefore high, and as the fact sheet warns, “these lower-quality debt securities carry a greater risk of default or price changes due to potential changes in the credit quality of the issuer.”

Default risk is difficult to quantify for an individual issuer, but the portfolio as a whole is sensitive to macro factors such as whether the U.S. economy is contracting or expanding. More on this later.

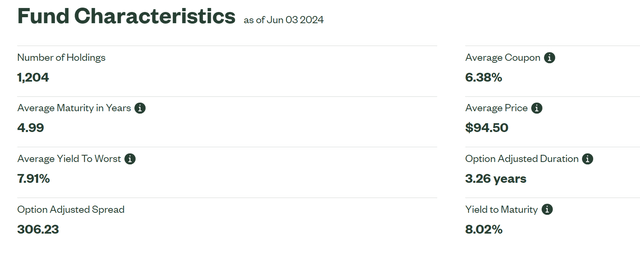

Other important portfolio metrics are displayed on the fund page.

Key metrics (SSGA)

The option’s adjusted duration of 3.26 years is low and means that JNK is not very sensitive to changes in interest rates. It is currently trading at around $94, 20% below its pre-Covid price. Compare that to the higher duration of the iShares 20+ Year Treasuries ETF (TLT) fund, which fell by about -50% in the same period. JNK may be high risk, but volatility is fairly low during calm periods in the market. However, when default risk rises, JNK becomes dangerous; Decreased by approximately -25% in March 2020.

Profits

Due to the short duration, the potential for capital gains is relatively low. The Bank of Japan rose nearly 10% from the October 2022 low to the 2024 high, but this was partly driven by market pricing in a recession and the risk of default.

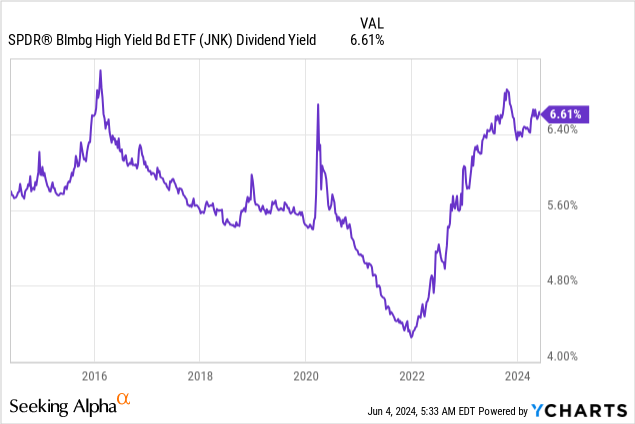

JNK is primarily about yield, and this is where it gets disappointing. Distributions are monthly and the current yield is 6.61%. The 0.40% expense ratio is high for bond ETFs, and brings the current yield from 6.61% to just 6.21%.

In the context of historical returns, 6.61% is considered a good percentage.

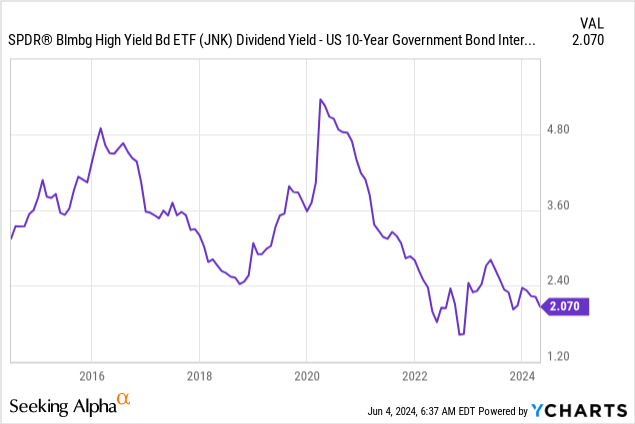

However, the spread with the risk-free rate, which is the yield on 10-year US Treasury bonds, is not attractive at all. There is only a 2.07% premium for much higher risks.

This spread remains the same if you replace the 10-year bonds with 5-year bonds to match the average maturity of JNK’s holdings. This is a big turn off. JNK was attractive during the ZIRP days when Treasury yields were close to nothing, and it was one of the only ways to get a return above 5%. Maybe the higher risk was worth it. Taking the expense ratio into account, the premium is now just 1.67%. The higher risk is not worth the extra 1.67% return.

Macro image

As mentioned earlier, JNK has benefited from an improving macro backdrop since late 2022. It is worth noting that JNK bottomed on October 13, 2022, the same day as the S&P 500 (SP500). Other bond funds like the iShares Core US Aggregate Bond ETF (AGG) and TLT hit bottom just one year later in October 2023.

The US economy surprised most recession-claimers in 2022 and 2023, and they have all but disappeared this year, as the economy was particularly strong in the first quarter. However, cracks are starting to appear again, from weak consumer data, a contraction in the ISM manufacturing PMI, and a cooling labor market. None of this is overly concerning yet, but the backdrop is becoming more uncertain for the economy and this could impact JNK.

This week Société Générale’s Albert Edwards warned that “investors may be wrong to trade off their recession expectations for a ‘no-land’ outcome.” He also noted that signs of distress are spreading.

“This distress is now playing out in the junk CCC (HYG) (JNK) world where spreads are widening sharply, even though higher grade bonds have the narrowest spreads versus US Treasuries,” Edwards said.

I think this plight can be ignored for a while, as the prospect of interest rate cuts will keep the markets in an uptrend. However, a cold economy is not an ideal backdrop for holding JNK and problems may arise later this year. Interest rate cuts probably won’t be the silver bullet that many think they will be.

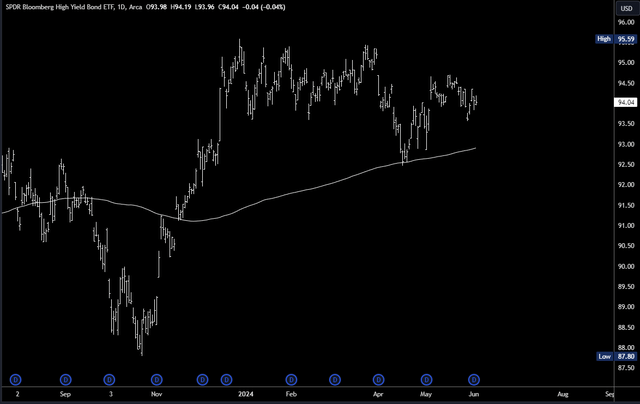

Bullish chart

JNK formed a “bullish flag” on the chart and rebounded strongly from testing the 200dma. The outlook should be positive for the coming weeks and months, with the flag likely to rise above $95.59. However, if this breakout fails and the price falls back below $95.59, JNK could be in danger of a major decline. Depending on the big picture, a pullback to $87.80 is not impossible.

JNK Chart (TradingView)

In short, the BOJ looks bullish in the short term, but is at risk of a major reversal later this year. This fits my view of the big picture.

Conclusions

JNK has a yield of 6.21% when taking its expense ratio of 0.40% into account. This premium is only 1.67% over ten-year US Treasury bonds, which is simply too low to bear the additional risk. Given the economic slowdown, and the potential for distress later this year, JNK is an avoidance.