J. Michael Jones

Cenovus Financial (New York Stock Exchange:SNV) is a bank founded in 1888 and headquartered in Columbus, Georgia.

As is the case with most banks, the higher cost of deposits results in lower net interest margin and net interest income; In addition to large unrealized losses The securities available with AFS adversely affect the tangible book value.

Over the past few months, management has been undertaking a series of maneuvers to unleash Synovus’ full potential, and in this article I’ll show you what it’s all about.

Difficulties that worry investors

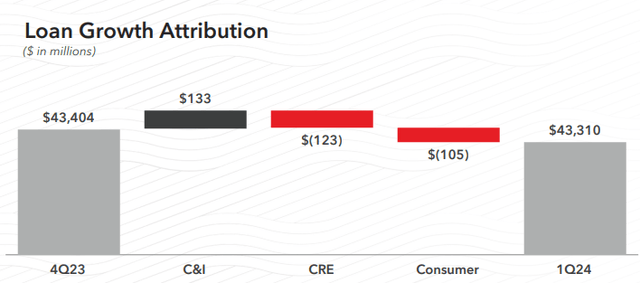

Cenovus financials for the first quarter of 2024

The first problem that SNV faces relates to the stalling of growth in total loans. The sector the bank is most focused on, C&I loans, had healthy growth of $133 million over the previous quarter, but CRE loans and consumer loans declined by $123 million and $105 million, respectively.

Guidance for the full year of 2024 shows an expected growth in total loans of between 0% and 3%, so it is far from exciting. C&I loans will once again likely be the most active segment, while the other two segments may disappoint due to declines in institutional CRE and senior housing as a result of continued disbursements. Interest rates are very high, and I think investors would prefer to pay part of the principal up front to reduce the total interest they would pay.

Cenovus financials for the first quarter of 2024

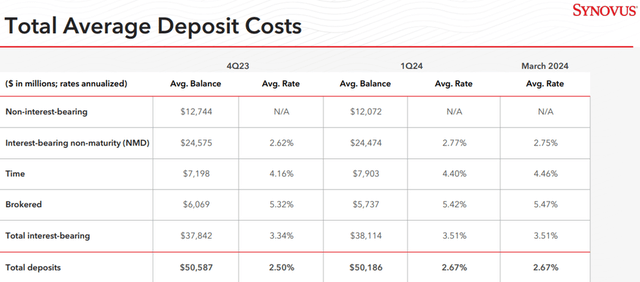

The situation is slightly better regarding total deposits. They are also decreasing, but guidance for 2024 sees core deposit growth of between 2% and 6%.

The decline seen in the first quarter of 2024 is mainly due to a seasonal element. In addition, the loan-to-deposit ratio is 85%, so the bank has some flexibility and does not necessarily need to increase its deposits.

In this aspect, perhaps the most important news is that in March, non-interest bearing deposits returned to growth (+$299 million) after several quarters of decline. If this trend continues, the cost of deposits will see a significant slowdown that could lead to the net interest margin rising again.

Cenovus financials for the first quarter of 2024

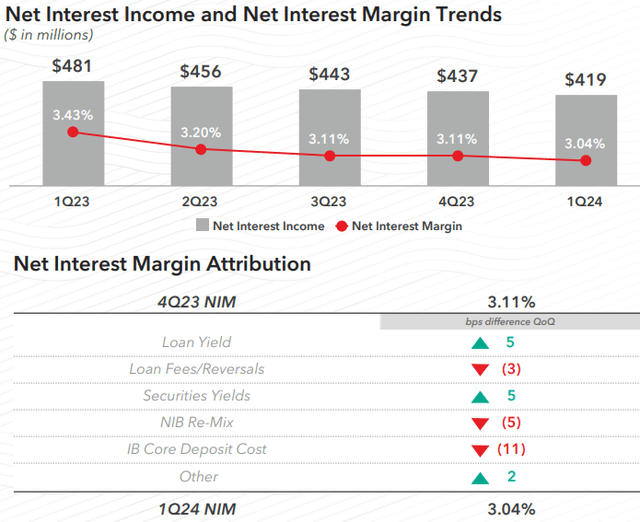

The latter fell by an additional 7 basis points from the previous quarter and reached 3.04%. This in itself is not a bad result, but after months of decline, there is a need to reverse the trend, otherwise SNV’s profitability risks a major setback. Management is working to develop the appropriate strategy to solve the problem, and there are several factors that can be taken advantage of.

Return to growth strategy

The demand for credit is no longer what it was in previous years due to high interest rates. Therefore, SNV cannot fully rely on it to improve its net interest income/margin. In any case, it could benefit from reorganizing its stock portfolio.

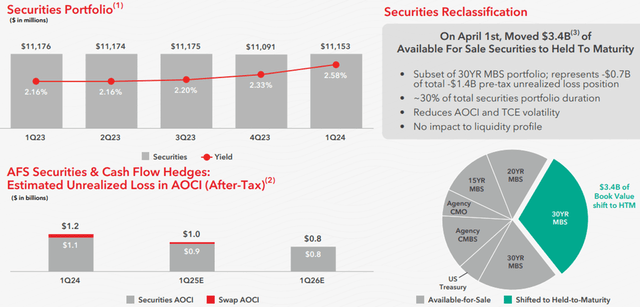

One of the major mistakes SNV made was to buy too many long-term, fixed-rate securities when the federal funds rate was still very low. As interest rates rose, these securities were exposed to large unrealized losses that affected the growth of tangible book value. Additionally, earning a yield of just over 2.50% from these securities when money market yields are currently more than double that is negative and unhelpful to your net interest margin.

Cenovus financials for the first quarter of 2024

The portfolio is currently valued at $11.15 billion, and its composition will change in the coming months. As mentioned, the goals are to reduce the AOCI weight on stocks and improve the average return.

In relation to the first objective, SNV reclassified US$3.40 billion of 30-year MBS from the AFS category to the HTM category. This way, AOCI would record $700 million less in unrealized losses. Obviously, these new origination mortgages have a new amortized cost basis of approximately $2.70 billion and no more than $3.40 billion. This maneuver will help tangible book value, which is a key component of any bank’s stock price in the long term.

As for the second objective, the bank will sell some securities available for sale at a loss and use the proceeds to buy new securities at current rates: we are talking about a margin of 300 basis points. These losses will certainly have a negative impact in the near term, but management expects a recovery period of about 5 years. In other words, the present is sacrificed for the sake of a better future.

Last month, $1.60 billion worth of AFS securities were already sold, resulting in a pre-tax loss of about $250 million. In my opinion, these sales can be continued in order to give a clear boost to profitability growth.

Here the question arises: Wouldn’t selling all these securities at a loss cause capital ratios to deteriorate? Probably not, and now I’ll explain why.

Cenovus financials for the first quarter of 2024

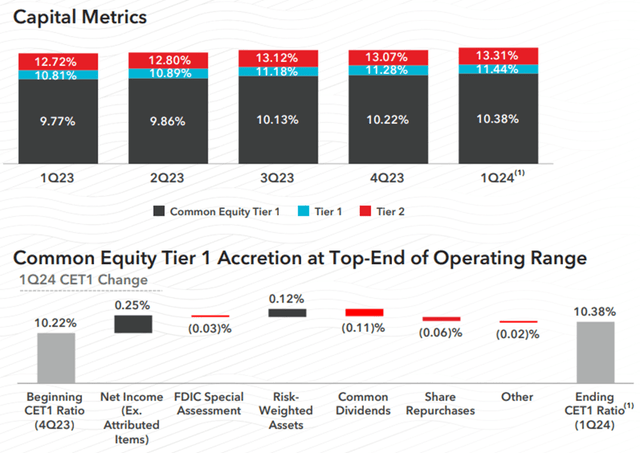

Currently, the CET1 rate is 10.38%, which is a significant improvement over last year and falls within the 10%-10.50% range expected by management. With unrealized losses on available-for-sale securities, there will certainly be a decrease in net income, but it will be offset by improved risk-weighted assets.

The effort we’re talking about today revolves around certain categories of loans that could qualify for reduced risk weighting, including mortgages, government lending, securitization exposure, and multifamily loans. The largest impact of this effort comes from loans that qualify for reduced potential risk treatment within our lenders’ financing portfolio. But in order to achieve this risk weight, the risk ratio must be reduced to 20% in many cases from the 100% we have today. We need to conduct appropriate documentation analysis in light of regulatory capital requirements under the simplified supervisory formula approach.

Unfortunately, we did not complete this effort. Therefore we cannot give specific details on the impact of capital ratios. But as we said in the prepared remarks, and as we show in the presentation, we think it can make sense.

CFO Jamie Gregory, Q1 2024 conference call.

Simply put, SNV could be allowed to use a lower weighting factor on some of its loans, and this would reduce the denominator of the CET1 ratio. As a result, the bank will be better capitalized and will be able to cover realized losses.

We don’t know the exact impact on capital ratios, but management is assuming a reduction in risk-weighted assets (RWA) between $2 billion and $2.40 billion, which increases the common equity ratio (CET1) by up to 50 basis points.

In addition, new capital will be released, ready to be used to purchase short-term, high-yield bonds, as well as to continue buybacks. In the first quarter of 2024, $30 million worth of treasury stock was purchased, and the company may continue to do so throughout the year if economic conditions are favorable. A bank that is afraid of deteriorating capital ratios will certainly not even think about doing a buyback, so the management is very confident in the portfolio reorganization plan.

Finally, let’s not forget that SNV has a dividend yield of 4.04% and a payout ratio of 52%. Therefore, in addition to the buyback, investors can expect good profits.

Conclusion

For Synovus Financial, the rapid rise in interest rates has generated many difficulties in terms of profitability and equity. In the former case, NII and NIM are constantly declining, and in the latter case, tangible book value must bear the brunt of AOCI.

Management is working to improve both, and the main lever now appears to be the stock portfolio. By reclassifying securities as HTM and selling less profitable available-for-sale securities, there will be a gradual improvement in the medium term. In the short term, net income will suffer a significant setback due to realizing losses.

Taker

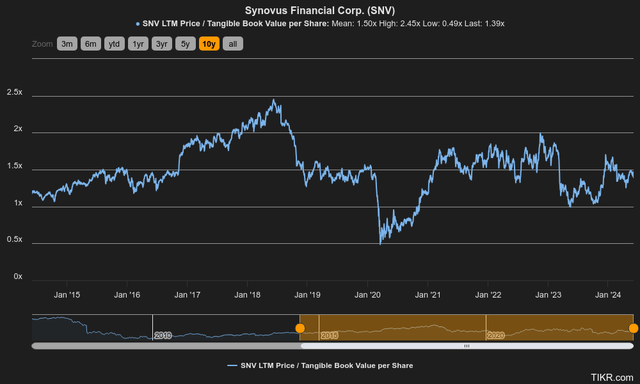

Currently, the stock’s price per share volume is 1.39 times, which is roughly in line with the 10-year average of 1.50 times. As far as I’m concerned, I would need a greater margin of safety before considering a purchase, which is why my rating remains pending as in my previous article. If the ratio drops to 1x, there is likely a basis to buy.